Credit: Jiri Rezac, The Climate Group, Creative Commons

China manufactures most of the world’s solar panels, and its state policy banks are among the largest financiers of energy projects in the world, particularly along the Belt and Road, Beijing’s global infrastructure project. But new data that tracks lending for overseas energy projects from China’s two leading policy banks, the China Development Bank (CDB) and Export–Import Bank of China (China Exim Bank), shows that just a tiny proportion is directed towards solar energy, which analysts say could make it difficult for the world to meet the renewable energy targets set by the Paris Climate Accord.

The findings are significant, analysts say, because China’s policy banks have surpassed the World Bank to become the leading financiers of global power generation projects, giving them outsized influence on whether nations choose to build solar, wind or coal projects.

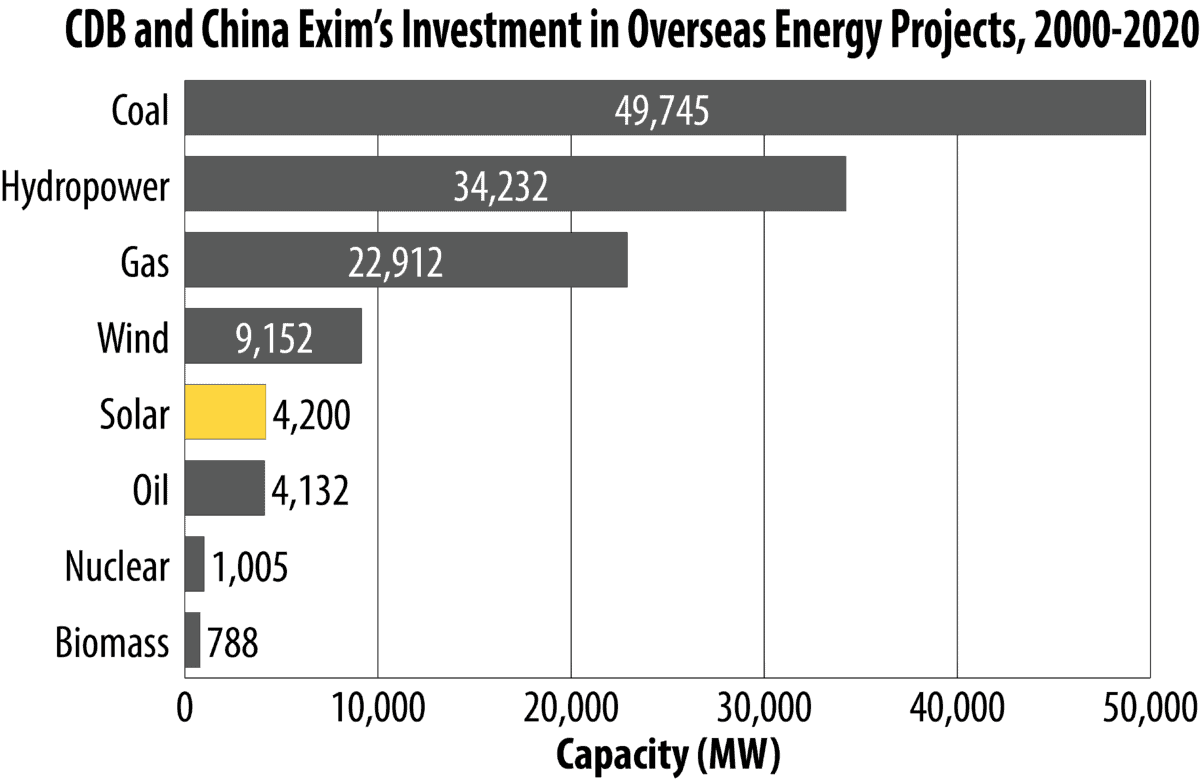

And while solar projects have gained substantially in the past decade, they lag far behind traditional sources of energy, like coal. In fact, between 2000 and 2018, solar projects accounted for just 1 percent of the total energy capacity financed by CDB and China Exim bank, while coal projects produced more than 62 percent of the capacity, according to China’s Global Power Database, a new dataset from Boston University’s Global Development Policy Center.

“There has been quite a bit of rhetoric about wanting to make the Belt and Road green, but in terms of actual investment, the proportion of solar projects has been quite small,” says Jonathan Hillman, author of The Emperor’s New Road: China and the Project of the Century (2020). There has been more solar investment from Chinese companies in the form of foreign direct investment, or FDI, rather than policy bank financing, analysts say, but that investment is also relatively limited compared to other forms of energy.

The World Bank Group, in comparison, dedicates more resources to solar energy. According to the Urgewald World Bank Group Energy Project Finance Database, 8.5 percent of their energy financing went to projects involving solar from 2014 to 2018.

Data: China’s Global Power Database

CDB and China Exim Bank are not turning away from solar because the Chinese firms lack technology or because the projects are expensive, experts say. After all, Chinese solar companies have dominated the global solar market with cheap panels for more than a decade. Rather, solar projects are typically much smaller, both in investment and energy capacity, than the typical coal plant, meaning they are only a blip on the radar for the behemoth banks.

“The projects are just too small to be attractive for CDB or China Exim Bank,” says Cecilia Han Springer, a senior researcher with the Global China Initiative at BU’s Global Development Policy Center.

Not only that, but Chinese solar companies also tend to be smaller and younger than the state-owned enterprises that develop overseas coal and hydropower projects, which means they lack experience and relationships with the policy banks. “The Chinese renewable players are simply not as big and as powerful and as competitive as their counterparts in the coal sector and hydropower sector, which, by the way, have been operating overseas for almost two decades now,” says Bo Kong, an associate professor of Chinese and Asian Studies at the University of Oklahoma and expert on the Chinese energy industry. “The Chinese solar companies are the new kids on the block.”

Chinese policy banks also have a troubled history with the solar industry. In the mid-2000s, the export-driven Chinese solar industry expanded at an extraordinary clip, with the help of government subsidies in the U.S. and Europe and credit from CDB and China Exim Bank. But after the global financial crisis, and the resulting rollback of solar subsidies in the Western world, many Chinese solar companies found themselves indebted, forcing the policy banks to intervene and save companies from the brink of bankruptcy.

“The Chinese solar industry is characterized by the boom and bust cycle,” Kong says. “Both policy banks have had some bad experiences financing solar expansion in China.”

There are other barriers as well. For instance, analysts say, many countries may not want solar development. Some developing countries turn to Chinese policy banks to finance energy projects that will fuel their industrial development, not renewable expansion. “It’s not only about the preference of the Chinese investors, it is also about the host countries,” says Kevin Tu, a senior advisor on the Chinese energy sector at Agora Energiewende, a Berlin-based think tank. “It is two-way traffic.”

Regardless of these solar financing challenges overseas, China continues to push the development of solar technology at home. “The Chinese have taken over the global solar industry in manufacturing and increasingly in innovation,” says Dan Reicher, a senior research scholar at Stanford and former U.S. Assistant Secretary of Energy for Energy Efficiency and Renewable Energy under the Clinton administration. This is particularly notable, he adds, because U.S. solar companies were industry pioneers in the twentieth century. “China used to be a place only for low cost solar manufacturing, but now it is a place for innovation and R&D,” says Reicher.

The Chinese solar industry is characterized by the boom and bust cycle. Both policy banks have had some bad experiences financing solar expansion in China.

Bo Kong, associate professor of Chinese and Asian Studies at the University of Oklahoma

China, in fact, has installed more solar capacity domestically than any other country in the world, and demand is expected to grow after Xi Jinping’s recent pledge to peak emissions before 2030 and reach carbon neutrality by 2060. Achieving that goal will require a 587 percent increase in solar installation within China from 2025 to 2060, according to data from the Tsinghua University’s Institute of Energy, Environment and Economy.

Even with the investment opportunities that will come with the domestic solar surge, experts predict that the large Chinese solar companies, such as JinkoSolar, JA Solar, and LONGi Solar, will still look to expand in global markets. Two other major solar markets — the U.S. and India — have imposed tariffs on Chinese solar panels, pushing these companies to look to regions like Southeast Asia and Latin America, which have been the most popular destinations for Chinese solar projects since 2000, according to China’s Global Power database.

In September, the results of Myanmar’s first large solar tender caught the attention of many analysts attempting to read the tea leaves on China’s future overseas solar investment. Out of the 30 winning bids, which were released by Myanmar’s Ministry of Electricity and Energy, 29 involved Chinese companies.

It’s not yet clear whether the winning companies are receiving support from CDB or China Exim Bank, says Tim Dobermann, an economist at the London School of Economics who has worked extensively with Myanmar’s Ministry of Electricity and Energy. “But how they are getting financing is incredibly relevant, because if they can get very cheap concessional financing from the Chinese government, then potentially they can deliver this at a really low cost, which is not something that a Western company would be able to do,” says Dobermann.

Some analysts interpreted the bids as the beginning of a shift towards more overseas solar project development from Chinese energy companies, but there are still many reasons for skepticism. “Myanmar is a very conclusive data point — 29 out of 30 says: watch the space,” says Tim Buckley, the director of energy finance studies in Australia and South Asia for Institute for Energy Economics and Financial Studies (IEEFA). “But it is only one data point, and one data point is not a trend.”

Katrina Northrop is a journalist based in New York. Her work has been published in The New York Times, The Atlantic, The Providence Journal, and SupChina. @NorthropKatrina