The series of fiscal and monetary stimulus policies either announced by the Chinese government or speculated upon by the market in recent days have provided a substantial boost to China’s previously gloomy stock market. Measures such as lowering interest rates, reducing the banks’ reserve requirement ratio — which on paper should allow them to lend more — and targeted support for local governments, the industrial sector, and households with children have lifted investors’ growth expectations. A late September Politburo meeting further strengthened the messaging by decreeing that “we must work hard to complete the economic and social development targets for this year.”

Click here to read a piece by Eliot Chen on state lending to China’s industrial sector.

However, a closer examination of these policies reveals their limited effectiveness in addressing China’s underlying economic challenges. Many of the policies, such as incremental rate cuts and selective fiscal support, are too modest to fully counterbalance the country’s deep-rooted issues such as distressed household and local government balance sheets, and a flailing real estate market. The lack of broader, more transformative reforms means that the immediate market gains will have limits.

First, most of the monetary policy measures announced by the People’s Bank of China, including the reserve requirement ratio (RRR) reduction and lower interest rates, were necessary to enable the financial system to roll over an enormous pile of non-performing or distressed debt, and will likely have limited scope to encourage new, more productive lending. Even before the announced 0.5 percentage point reduction in the RRR, the actual ratio of money banks are required to hold in reserve to their total deposits had fallen from 10 percent at the end of 2023 to 6.9 percent in August. In other words, China’s banks have already had to free up substantial amounts of money to support troubled borrowers over the past year and half.

The central bank’s interest rate cuts, especially the 0.5 percentage point cut for outstanding mortgages, could alleviate payment pressures for some households, especially those who bought homes in recent years when interest rates were higher. However, the economic impact will be modest since overall household leverage ratios were not that high to begin with. Meanwhile most local governments are so indebted that a half-point interest rate reduction will merely alleviate their cash flow pressure by a modest degree. They will still need billions of renminbi in fresh capital each month to roll over both their official and off-balance sheet debt — mostly in the form of debt owed by local government financing vehicles — and to pay interest on it.

Any set of policies aimed at meaningfully restructuring its debt and boosting growth will thus require much more than the 3-4 trillion renminbi impact of the announced/rumored policies.

In terms of fiscal policies, Reuters has reported that the government is considering issuing 2 trillion renminbi’s (nearly $300 billion) worth of special government bonds. But this amount will also provide only a modest and temporary lift to sentiment. Half of the proceeds might have to be allocated to financially strapped local governments. This would be a repeat of the 2020 special bond program, which prevented the bottom from falling out at the local level, but ultimately did not lift medium-term growth. Even 1 trillion renminbi is only equivalent to the amount needed to service a month or less worth of local government bond obligations, meaning it offers limited impact on local fiscal stress.

Moreover, this short-term infusion fails to address structural issues such as the fact that local governments have limited fiscal autonomy and high debt levels. And while it may enable some wage arrears for civil servants to be paid, the long-term impact on household consumption will likely remain muted. Local civil servants, a key element of China’s middle class, are still reeling from months of wage arrears, and will likely be wary of future wage delays. They may choose to save the recouped income rather than spend it, limiting any boost to consumption.

The other half of the special bond issuance might go toward subsidizing equipment renewal for firms and even special subsidies to households with more than one child. Equipment renewal subsidies could result in marginal improvements in demand for industrial output, but without robust demand or broader economic reforms, the benefits may not translate into sustainable growth and may lead to further price reductions in Chinese exports. This, of course, would elicit greater protectionist reactions from the world.

As for the rumored 800 renminbi ($114) monthly subsidies per child after the first born, there are some 226 million children below the age of 14 in China. Even if we assume that only 10 percent of them are younger siblings, this would still require 217 billion renminbi ($31 billion) in subsidies per year. At this rate, either local authorities would have to shoulder much of the cost, which they lack the capacity to do, or this would prove to be a temporary program with minimal effect. To make such a policy more sustainable, the government could set up a special baby fund with an initial fiscal injection, followed by annual contributions from taxes or fees, from which a steady stream of funds could be paid over the long term, albeit likely less than 800 renminbi per child per month. The fertility impact of such a program would likely still be modest, and the growth impact even more so.

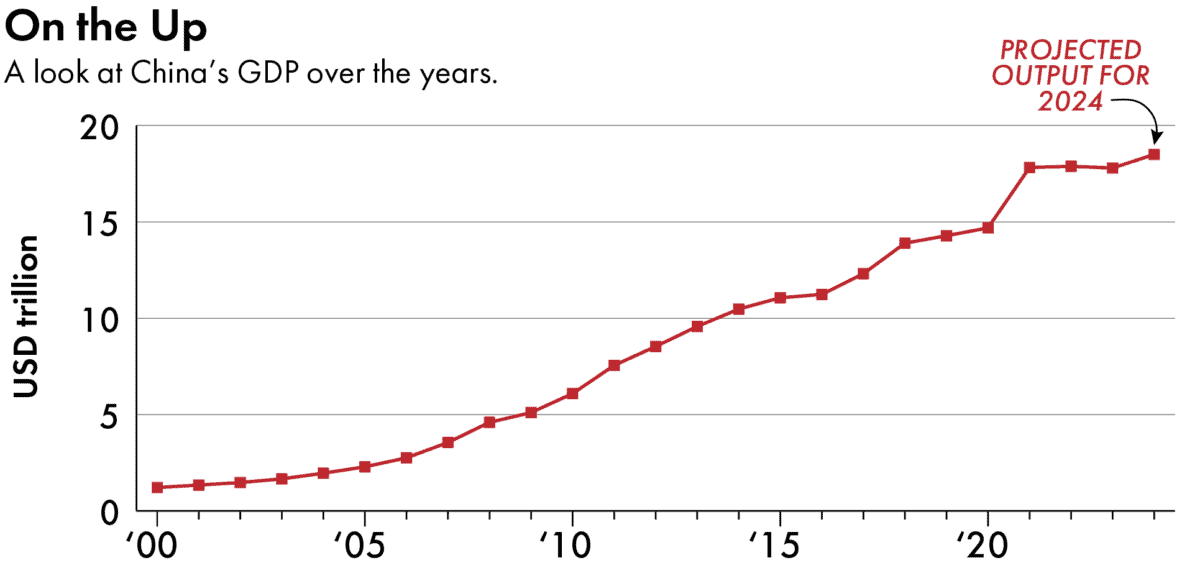

Two economic realities face China today. First, it has the second largest economy in the world at a projected output of 130 trillion renminbi ($18.5 trillion) this year. Second, it has some of the highest governmental debt in the world, at well over 100 percent of its GDP. Any set of policies aimed at meaningfully restructuring its debt and boosting growth will thus require much more than the 3-4 trillion renminbi impact of the announced/rumored policies. A true bazooka for the economy would need to be to the tune of 13-20 trillion renminbi.

In addition, the de facto tax rate in China is fundamentally much too low for a middle income economy struggling with a host of debt and public service challenges. Across all levels of government, China only collected taxes equivalent to 14 percent of its GDP in 2023, which was far below that of any major economy. Gradually increasing tax rates would put both debt sustainability and public goods provision on better footings.

For now, the leadership does not seem to want any fundamental change in its supply-side dominant growth model. It might require greater economic volatility before the leadership gets the message.

Victor Shih is a professor of political economy at UC San Diego and holds the Ho Miu Lam Chair in China and Pacific Relations at the School of Global Policy and Strategy. He is also the director of the 21st Century China Center and the author of Coalitions of the Weak: Elite Politics in China from Mao’s Strategem to the Rise of Xi. @vshih2