U.S. President Joe Biden and his predecessor Donald Trump, the presumptive Republican nominee in November’s presidential election, are competing to portray themselves as tough on trade and China. Biden has already imposed a 100% tariff on Chinese-made electric vehicles, and Trump has vowed to impose a 200% tariff on Chinese cars manufactured in Mexico, along with a range of other protectionist measures affecting steel, solar panels, semiconductors, and batteries. The European Union is likely to follow suit, albeit more cautiously.

Under President Xi Jinping, China is widely expected to respond with tit-for-tat tariffs rather than turn the other cheek, thus increasing the likelihood of a trade war that could significantly impede the green-energy transition and potentially lead to a broader geopolitical conflict.

What is often missing from the debate about the escalating rivalry between the United States and China is the perspective of other countries, especially larger developing economies. After all, these tariffs are not just protectionist but also discriminatory. If there is any truth to the joke that China is the only country in history with a comparative advantage in every industry, then targeting the world’s most efficient exporter and supplier with protectionist measures could create lucrative opportunities for its competitors.

In analyzing these developments, it is instructive to consider the free-trade agreements of the postwar period. These FTAs were a mirror image of today’s discriminatory measures: while they reduced tariffs on imports from partner countries, effectively diverting trade away from third-country suppliers, today’s tariffs are being imposed on imports from perceived adversaries like China, redirecting economic activity toward third-country suppliers considered allies.

The Biden administration’s China trade policy, which U.S. National Security Adviser Jake Sullivan likened to “a small yard and a high fence” in 2023, could further weaken Chinese manufacturing. In fact, the higher the tariffs, the greater the competitive advantage third-country suppliers will gain over Chinese firms, particularly in large markets like the U.S. and Europe.

To be sure, these gains will depend on the extent of U.S. protectionism. If Sullivan’s “small yard” grows larger, with U.S. tariffs imposed not only on imported goods from China but also on goods from third countries that either use components produced in China or by Chinese firms located in these countries — the benefits to these third-country suppliers will be reduced. In the language of FTAs, rules of origin can be so restrictive on Chinese inputs that third countries gain less than they would otherwise.

In the first wave of discriminatory protectionism unleashed by Trump, the scope of protectionism was limited to direct imports from China. As a result, as documented by Aaditya Mattoo and others at the World Bank, third countries like Vietnam benefited significantly. This time, given bipartisan support in Washington for anti-China legislation, the scenario of a growing yard cannot be ruled out.

Should today’s trade war escalate into a full-scale geopolitical conflict, any potential advantages would be negated by a broader economic downturn and increased uncertainty…

Broadly speaking, the countries affected by Western protectionism can be divided into two groups: those integrated into the Chinese supply chain, such as Vietnam, Thailand, Indonesia, Malaysia, and South Korea, and those less dependent on it, like Mexico, India, Turkey, Brazil, Poland, and Hungary. The second group stands to gain more from U.S. trade policies.

India offers a prime example. It has successfully attracted several Western firms exiting China since launching its “China Plus One” strategy in 2014. Notably, Apple has significantly expanded its iPhone manufacturing operations in India, and Tesla reportedly may follow suit. This shift presents India with an opportunity to revitalize its consistently underperforming manufacturing sector. To this end, the government is offering subsidies to attract foreign investment and offset disadvantages such as relatively poor infrastructure.

By increasing the returns on investing in India, current U.S. trade policy could complement its own industrial policy. If India can establish a supply chain that is largely independent of China — a trend that is slowly underway in the electronics sector — it could gain a competitive advantage over China and countries linked to it.

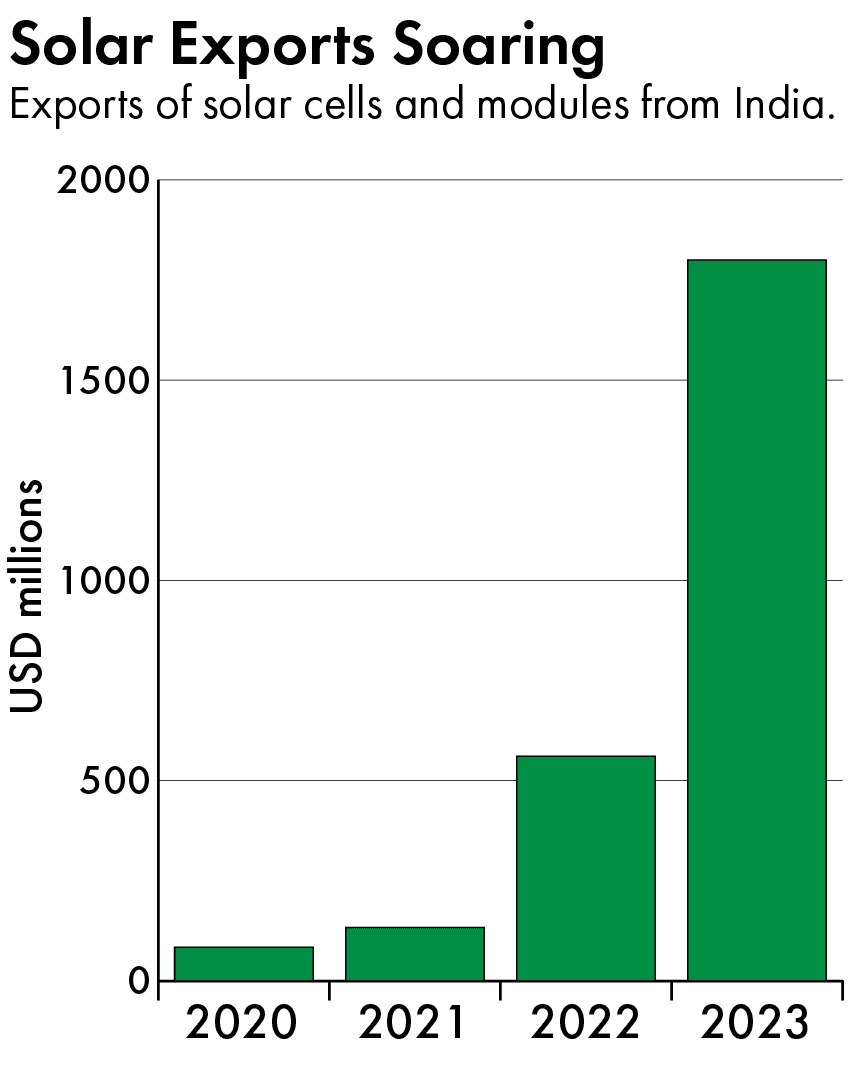

Solar panels are a case in point. I recently visited an American-owned factory just outside of Chennai that produces solar panels for export to the U.S.. This operation owes its success to Trump’s tariffs on imported solar panels from China, which the Biden administration has maintained. Without these measures, Chinese manufacturers’ efficiency and scale — helped by massive government subsidies — would have rendered India an unattractive investment destination. But India was able to seize the opportunity and increase its solar-panel exports.

More broadly, the greater the overlap between America’s strategic interests and third countries’ capabilities and comparative advantages, the more likely that discriminatory protectionism will be long-lasting and provide certainty to investors seeking to diversify away from a ruthlessly efficient China. In pharmaceuticals, for example, India has the capability to step in if the U.S. decides to impose tariffs on Chinese drug manufacturers, which dominate the global production and export of active pharmaceutical ingredients.

But China’s competitors should curb their enthusiasm. Discriminatory protectionism is currently confined to relatively sophisticated industries and is unlikely to extend to labor-intensive sectors like apparel and footwear, where poorer countries have a stronger comparative advantage.

More importantly, U.S. and EU discriminatory protectionism is beneficial only in moderation. Should today’s trade war escalate into a full-scale geopolitical conflict, any potential advantages would be negated by a broader economic downturn and increased uncertainty, which could have a chilling effect on global trade and investment. In this scenario, everyone would lose.

Copyright: Project Syndicate, 2024.

Arvind Subramanian, a senior fellow at the Peterson Institute for International Economics and former chief economic adviser to the Indian government, is the author of Of Counsel: The Challenges of the Modi-Jaitley Economy (India Viking, 2018).