It’s not often that trade policy and sports culture collide, but this June, as European soccer fans gather for the UEFA European Football Championship, the current trade predicament facing the E.U. will — quite literally — be center stage.

|

|

| Illustration by Nate Kitch | |

| More in this series: | |

| The Japan Model |  |

| Rare Earth Reshore |  |

| Out of Bounds |  |

| Tomorrowland |  |

| The Chip Comeback |  |

The tournament, which takes place every four years, is one of Europe’s most coveted sporting events, and a marquee sponsor this year is BYD, China’s largest electric car maker. Given the context — that European automakers are struggling to fend off rising Chinese competition — it is insult enough that BYD secured this unprecedented marketing opportunity to showcase its diverse range of vehicles to climate-conscious European consumers.

The added injury is that the tournament is being held in Germany, Europe’s largest economy and automotive center, and one of its main sponsors used to be Volkswagen, Germany’s homegrown auto giant, which bowed out after Euro 2020 for “cost discipline” reasons.

For those concerned about the future of Europe’s automotive industry in face of stretching Chinese competition, the symbolism smacks.

“BYD is essentially a battery maker that learned how to make cars, and since batteries can account for 40 percent of the value of an electric vehicle, its rise is going to be very disruptive to German automakers,” says Ilaria Mazzocco, a senior fellow at the Center for Strategic and International Studies.

Short for “Build Your Dreams,” BYD Auto was ridiculed by Tesla’s Elon Musk after entering the EV game. But last year, it silenced critics when it surpassed Volkswagen to become the largest selling car brand in China. Now, BYD is making its move on Europe and unloading thousands of new EVs at European ports.

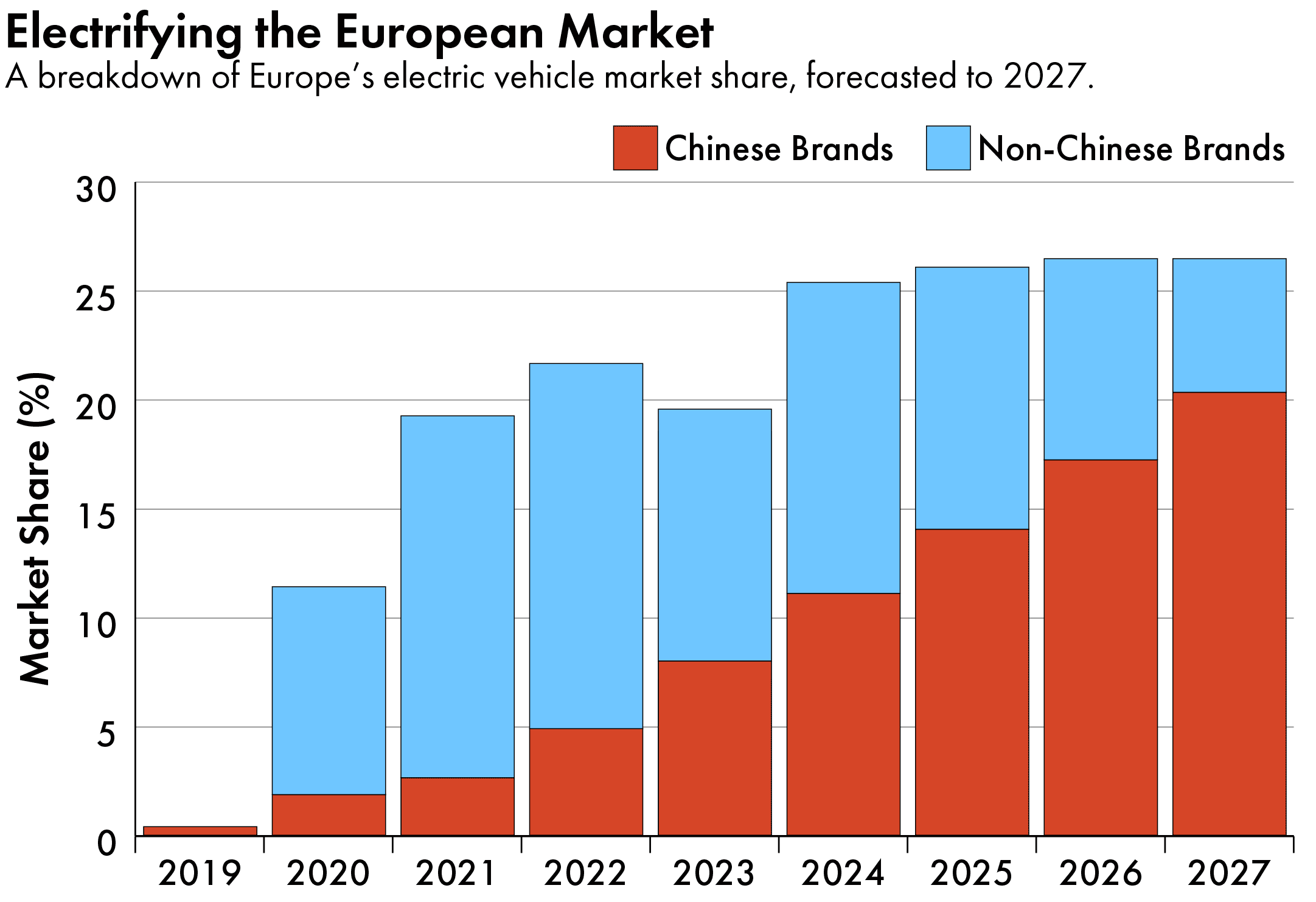

And it’s not the only one: Close to 40 percent of China’s EV exports last year landed in the E.U. — causing collective panic among European leaders. Ursula von der Leyen, president of the European Commission, has warned that Chinese electric vehicles were “flooding the European market” due to “China’s market distortions.” Christiane Benner, head of Europe’s largest industrial union IG Metall, cautioned that the E.U. is facing “creeping deindustrialization.”

According to Transport and Environment (T&E), a clean transport campaign group, 20 percent of EVs sold in the EU last year were made in China. Close to half of those exports were western brands, particularly Tesla’s Shanghai-made Model Y and Renault’s Hubei-made Dacia Spring. But by 2027, T&E predicts that Chinese brands will account for one in every five EVs sold in the E.U.

“Chinese electric vehicle producers are very good at reducing costs and very competitive when it comes to performance and innovation,” says Yanmei Xie, geopolitics analyst at Gavekal Research. “Some level of sinicization of the European car industry is inevitable.”

European leaders have long argued that climate cooperation with China is necessary to fulfill a higher purpose — namely, achieving the green transition to address global warming. But as the Chinese export drive of green technologies has intensified — Chinese automakers now make up a quarter of all global orders for car-carrying vessels — so too have European doubts. The deluge, experts warn, could seriously undermine the European economy.

The automotive sector provides direct and indirect jobs to 13.8 million Europeans, over 6 percent of the E.U.’s workforce, and represents 7 percent of the regional bloc’s economic output. But the E.U.’s once vaulting automotive trade surplus is falling fast — and the near 200 percent increase in Chinese automobile imports from 2019 to 2023 is the main reason why. The transition to EVs may very well accelerate this decline.

“This is a call of alarm,” warns François Godement, a senior advisor for Asia at the Institut Montaigne in Paris. “Whether Chinese competitiveness comes from subsidies, or scale, or actual manufacturing savvy, the challenge for European industry is unprecedented.”

A failure to respond could, in turn, upend the European climate agenda. Not only are made-in-China EVs more carbon-intensive than made-in-Europe EVs, but the potential hit to Europe’s economy could undermine Western political support for decarbonization policies.

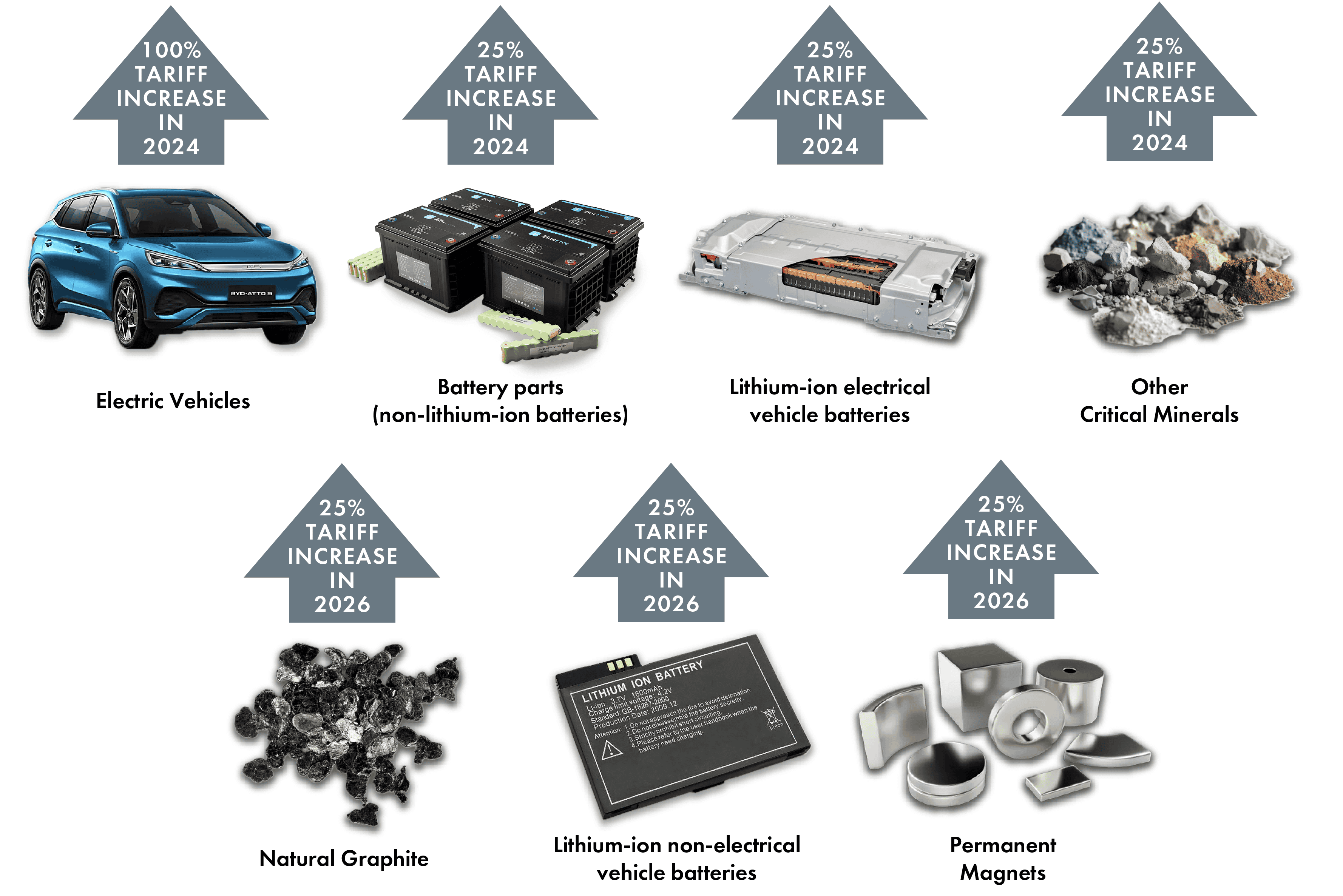

The EV challenge from China is hardly as imminent in the United States; the 25 percent tariff hike imposed in 2017 by the Trump administration has ensured Chinese EVs have hardly made a dent in the U.S. market. And yet, just this week in the U.S., the Biden administration took extraordinary preventive measures — quadrupling those tariffs to 100 percent — to protect “American workers and businesses” from Chinese imports.

The U.S. move may slow the country’s green transition in the coming years, but experts argue the E.U. needs to take similar steps — and fast.

The flood of Chinese EVs “is going to hurt Europe,” explains Camille Boullenois, an associate director at the Rhodium Group. “There are very valid reasons for the European Commission to act now before it is too late.”

President of the European Commission, Ursula von der Leyen, announces the investigation into electric cars from China, September 13, 2023. Credit: European Commission

The E.U., for its part, launched an anti-subsidy investigation on electric cars from China last October, and analysts expect it to impose tariffs of 15–30 percent in July. Former Italian prime minister Mario Draghi is also working on a new strategy for E.U. competitiveness, which he has said argues for “radical change” to secure the electric vehicle supply chain. And in a recent speech at Princeton University, the E.U. competition commissioner Margrethe Vestager called on G7 countries to “develop a list of trustworthiness criteria for critical clean technologies” with environmental, labor rights, and cybersecurity and data security requirements.

But although the tone from Brussels has hardened considerably, the E.U.’s position remains more nuanced than America’s. German automakers, for instance, are much more ingrained in China than American automakers, and unlike the U.S., the E.U. is not opposed to Chinese EV and battery makers setting up shop in Europe. While there are calls for the E.U. to act as aggressively as the U.S. in blocking the influx of Chinese-made EVs, the more thought-provoking question is how the E.U. might leverage its position to both have its EVs and make them too.

BATTLE LINES

In recent years, the E.U., the U.S. and others have taken a page from China’s playbook by engaging in high-stakes industrial policy. But the size and scope of China’s EV-oriented industrial policy would make even the most-devoted dirigiste policymaker blush.

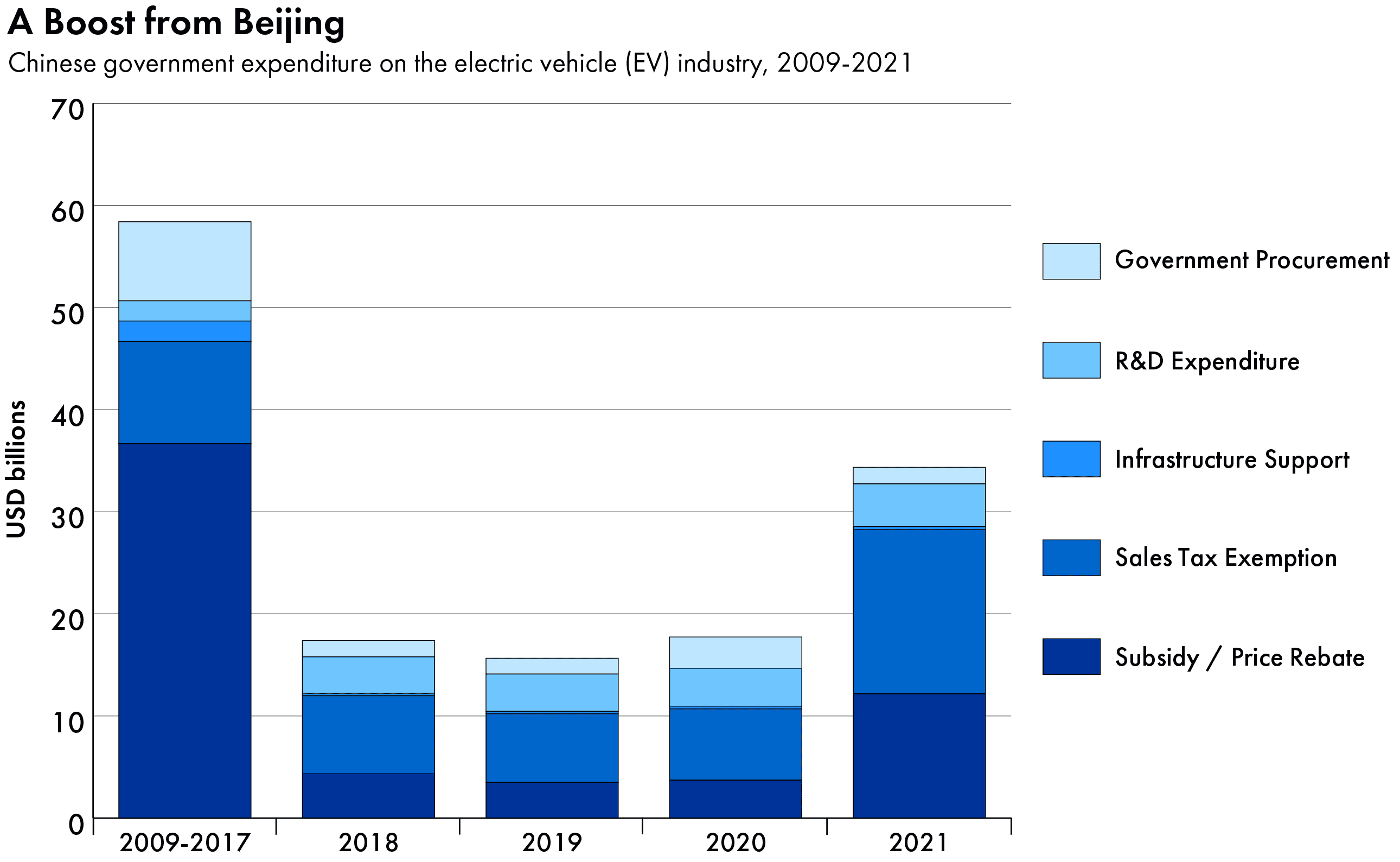

On top of direct subsidies, the Chinese automobile industry benefits from tax deductions, public procurement, land provision, cheap energy and low-interest loans. One study estimates that from 2016 to 2022 China’s central government EV purchase incentives were five times larger than those in the United States. Another study counts Chinese government support for EVs as $58 billion between 2009 and 2017, with such provisions increasing sharply up to 2021.1As China’s EV market matured, purchase subsidies were phased out by the end of 2022.

“Chinese companies are not responding to demand signals from the market, but production incentives from across all levels of the Chinese government,” says Gavekal’s Xie. “Overcapacity is a chronic phenomenon in China’s industry policy.”

Boullenois, from Rhodium, adds that while overcapacity is not spread evenly among China’s EV makers, it is nonetheless a driver for the ruthless price war currently underway in the Chinese market that in turn is pushing BYD and other leading companies to rush out exports in order to boost shrinking margins at home.

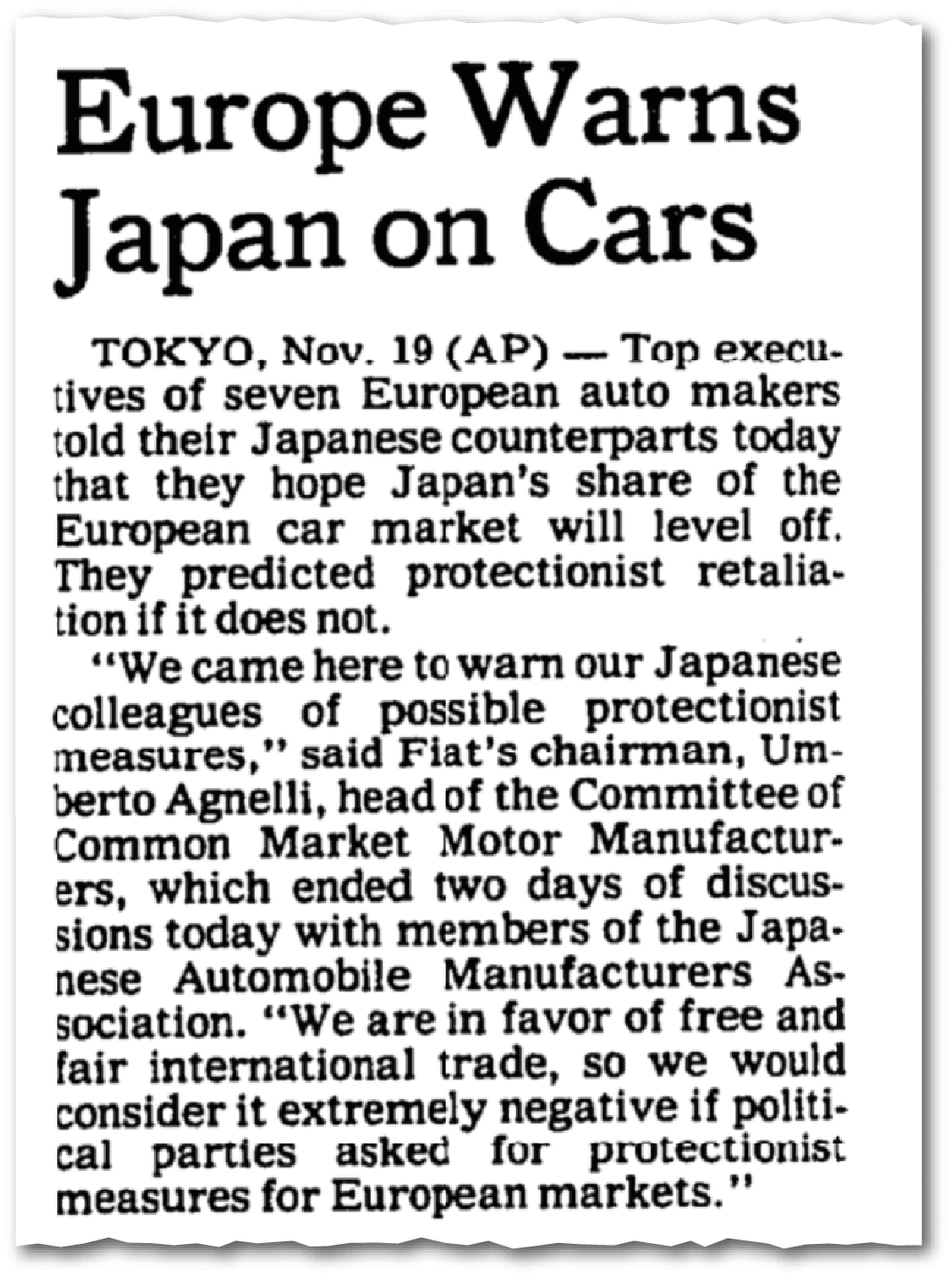

Whatever the causes, the result is a proliferation of extremely low-cost, made-in-China EVs in Europe. And the current predicament is reminiscent of the late 1970s, when European and American markets experienced an influx of more affordable, reliable, and fuel-efficient Japanese automobiles. Led by Toyota, Japan’s exports grew fivefold within a decade. By the early 1980s, Japanese vehicles represented 23 percent of the U.S. car sales and grabbed 10 percent of European markets.

As they are doing now, expert commentators at the time posed the ‘fortress’ question of trade: to block or not to block imports. German executives thumped their corporate chests, saying the Japanese competition would only make them stronger, while their French counterparts derided an undervalued Japanese yen and demanded the same rules of the game for everybody.

Today, not much has changed: The regional bloc is divided between the German position to lay off and the French decision to support the Commission’s ex officio anti-subsidy investigation on Chinese-made EVs.

Luca de Meo, chief executive of the French automaker Renault, has even called for a “European Marshal Fund” to support the automobile industry through investment and cooperation against an “onslaught of Chinese electric vehicles.” In his 19-page open letter, De Meo points to Europe’s Airbus experience as a “tried and tested model.” (Airbus developed into a frontrunner to challenge Boeing only after ample state backing and a collaborative program between government and industry in France, Germany, and Britain took shape in the 1960s. Former French President Charles de Gaulle decried Boeing at the time as an “American colonization of the skies.”)

For a French carmaker like Renault, however, there are few sales in China to defend in a possible trade war. In contrast, German automakers fear their collective 20 percent market share in China (VW alone held 14.5 percent in 2023) may become the main target of Chinese trade retaliation. Mercedes-Benz chief executive, Ola Källenius, has even called for reducing current European tariffs on automobile imports.

German automakers still have significant financial resources and production know-how, but it is looking quite dire. They neither have a price advantage nor a technology advantage in software and batteries.

Gregor Sebastian, a senior analyst at the Rhodium Group

“Part of the German industry has sold itself to China by agreeing to lobby against duties,” says Godement from Institut Montaigne.

The German strategy is not only about protecting its existing market share, however. Many argue that because China is the epicenter for EV innovation, European and other foreign automakers will only fall behind more if they choose to leave. And they’re backing that assessment up with investments.

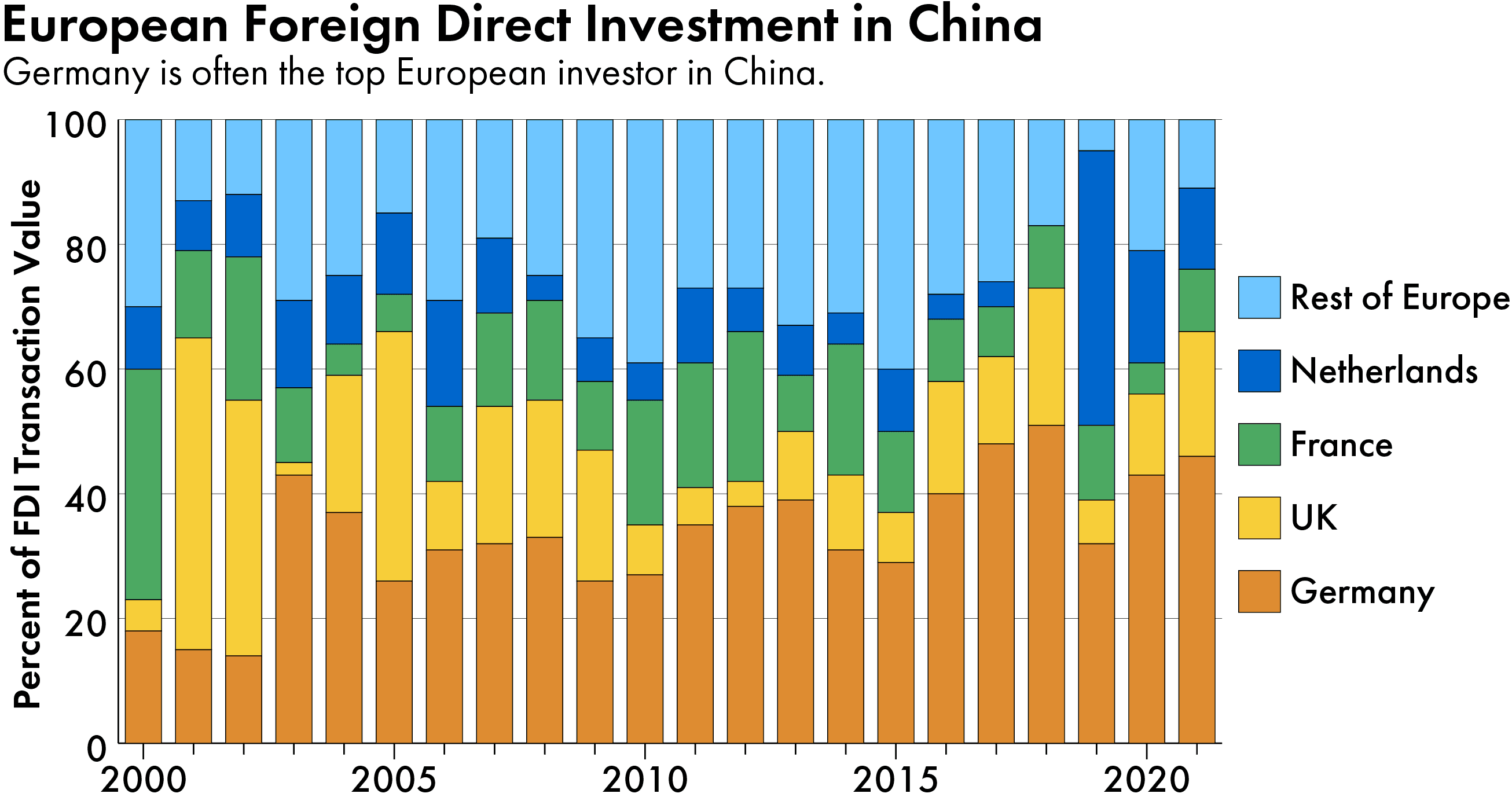

Germany represented close to 60 percent of total E.U. investment in China between 2016 and 2023, compared to an average of under 40 percent the prior decade. In 2021 the German automotive industry made-up 42 percent of total E.U. foreign investment in China. In fact, at a time of staggering lows in overall foreign investment in the Chinese economy, Germany reached an all-time high at close to $13 billion last year.

Some say all that investment could pay off for German automakers.

“South Korean carmakers have been kicked out of the Chinese market, and the Japanese are on their way out,” says Gavekal’s Xie. “Rather than seeing this as a trend that the water is rising, the German automakers may see themselves as the last one standing among foreign brands.”

But as consumers switch to EVs, such optimism could also be misguided, says Gregor Sebastian, a senior analyst at the Rhodium Group.

“German automakers still have significant financial resources and production know-how, but it is looking quite dire,” he says. “They neither have a price advantage nor a technology advantage in software and batteries.”

Indeed, since 2018, the market share of German automakers in China has collectively fallen by 4 percent. VW’s export deliveries to China from its luxury brands, like Porsche, are shrinking, and the company’s joint ventures in the Chinese market have seen annual earnings cut in half since 2015, from over €5.2 billion to €2.6 billion. Overall, VW saw vehicle sales growth of only 2 percent in China last year.

In the E.U., by contrast, VW reported a 20 percent increase; it sold some 400,000 more cars than in China and generated around €180 billion in sales revenues.

When it comes to the EV sector, automakers like VW are still investing in factories in North America and Europe (VW has gigafactories in Germany and Spain, for instance, and BMW is retooling its Munich plant for EV production), but some E.U. policymakers fear that European car makers will increasingly exploit China’s hyper-efficient manufacturing base to export back to Europe.

“Dacia Spring is made in China. The Smart car is made in China. Volkswagen will start to make its Cupra in China,” says Mazzocco. “There is an element here [with the anti-subsidy investigation] of the Commission telling European companies that they better not go and move everything to China because we are going to slap a tariff on you.”

And that tariff would hurt European brands far more than Chinese ones. In fact, Godement from Institut Montaigne, argues that Chinese EV makers are still well-positioned to lower their prices considerably.

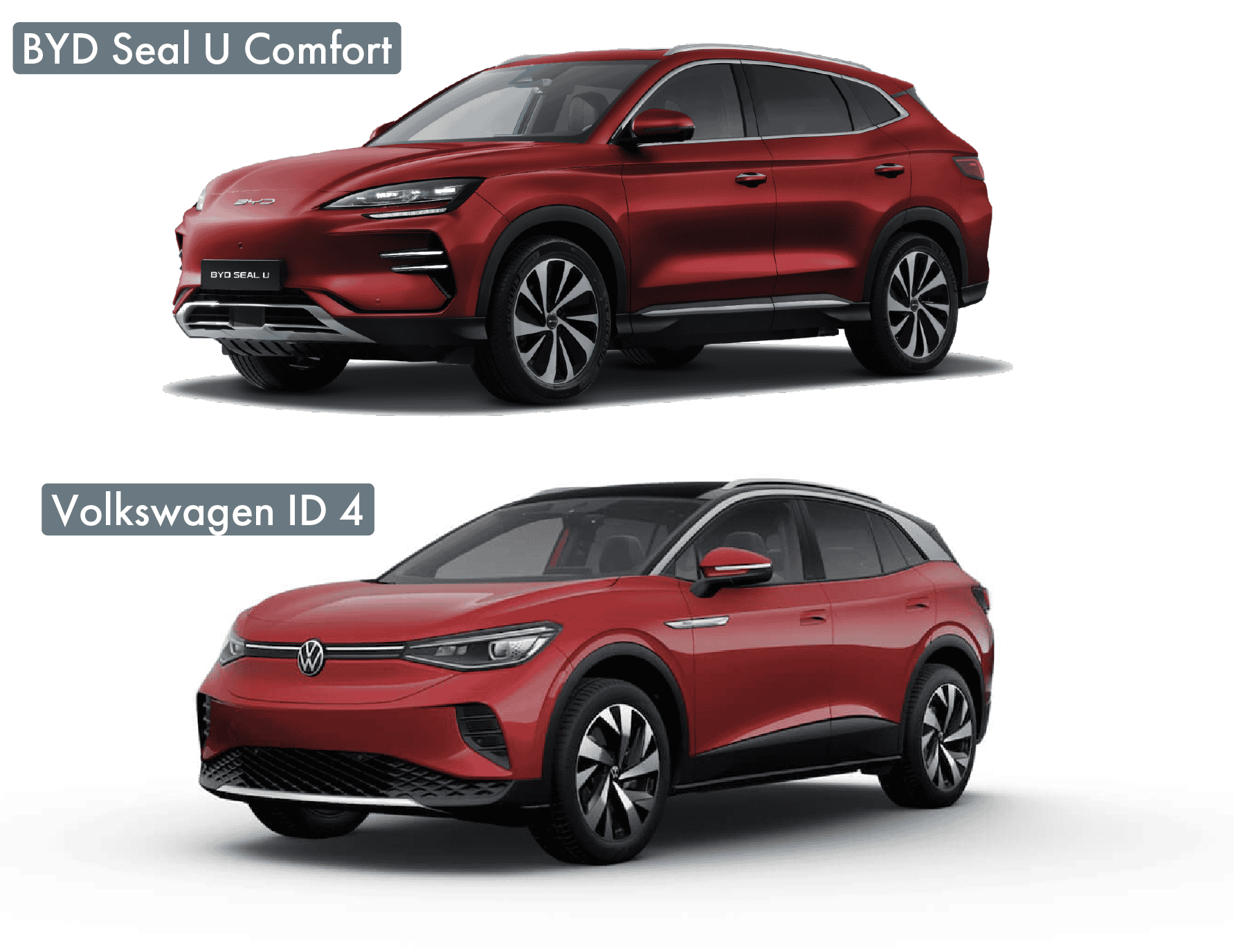

Rhodium Group research (and analysis from JATO Dynamics) shows, for example, that although the BYD Seal U Comfort has a sales price of only 10 percent lower in Germany than its comparable model, the ID 4 from Volkswagen, the Chinese EV maker’s premium is over 43 percent higher than its German counterpart.

As a result, the E.U.’s likely application of provisional duties between 15 to 30 percent will not be enough to overcome the combination of China’s state support and the manufacturing advantages of its EV makers. BYD and other Chinese brands are also positioning themselves to circumvent tariffs through third-country assembly, such as in Mexico and Morocco, and strategic collaboration between western and Chinese brands is well underway.

The U.S. is already preparing to penalize any Chinese EV moves from its southern neighbor, but when put altogether, western bureaucrats will have their work cut out for them when it comes to actually enforcing tariffs and other defensive measures.

Chinese EV makers, in other words, are relatively tariff-resistant. In the E.U., at least, the estimated level of duties will mostly impact EV exports from China by western carmakers, such as Tesla and BMW. This might encourage more ‘re-shoring’ of the EV industrial base in Europe, but it will do little to stop the surge of leading Chinese EV brands.

For that, the E.U. may need to take a new direction in leveraging incoming Chinese investments.

‘BUY EUROPE’

Chinese officials argue that the E.U. has no choice but to buy made-in-China EVs and other clean technologies to meet its net-zero emission targets.

But they tend to neglect the fact that the production of EVs in China is far from green.

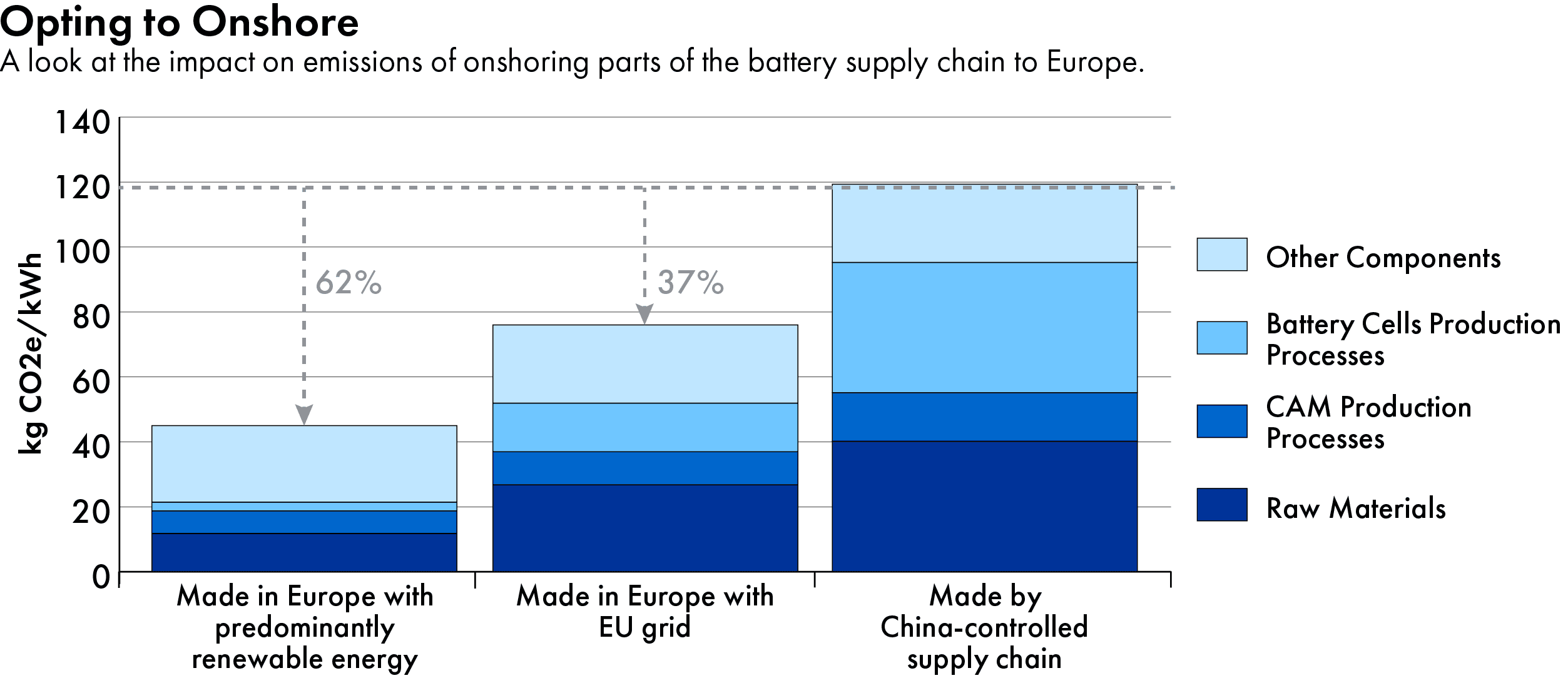

New research from the climate group T&E finds that if the E.U. fully onshores the battery supply chain, the carbon intensity of production would be 37 percent lower on average across member states than emissions produced in China (which still relies heavily on coal) and almost two-thirds lower in European countries where power generation relies primarily on renewable energy, such as in Sweden, a rising battery producer.

“There is a climate benefit for Europe by onshoring EV production,” notes Julia Poliscanova, senior director for vehicles and e-mobility supply chains at the T&E climate group.

France has already incentivized the purchase of EVs produced with relatively lower-emissions, which disqualified many EVs manufactured in China. And the initiative shows promise: Even though total EV purchases in France have risen compared to its European counterparts so far this year, sales of made-in-China brands that are illegible for subsidies have dramatically collapsed — from 22 to 4 percent of EVs sold.

The goal is to localize manufacturing to Europe. It is not about the nationality of the manufacturer. We need Chinese know-how. We just want them to on-shore production here.

Julia Poliscanova, senior director for vehicles and e-mobility supply chains at the T&E climate group

The country agnostic environmental scheme is under consideration in Italy, and might even serve as a lesson for the Americans. The Biden administration’s climate envoy, John Podesta, has established a task force to examine limiting imports from countries with high carbon footprints.

European leaders are also pushing past the American model by attempting to attract Chinese investment, even as they try to dissuade imports of Chinese EVs. Although American automakers Ford and GM are cautiously exploring licensing agreements and joint U.S. factories with Chinese battery giant CATL, the E.U. is actively courting Chinese investment. Alongside European companies, such as Northvolt and Verkor, Chinese EV and battery makers BYD and CATL have benefited from the Commission’s loosening of rules for member states to provide state aid to industry to support its Green Deal Industrial Plan.

“The goal is to localize manufacturing to Europe. It is not about the nationality of the manufacturer,” says Poliscanova. “We need Chinese know-how. We just want them to on-shore production here.”

That is, she stresses, if the Chinese manufacturers meet the E.U.’s social and environmental rules.

The problem for member states seeking to attract foreign investment in EV and battery manufacturing is that Chinese and other companies can pick and choose their destinations while still accessing the trade benefits of setting up shop in the common market.

Rather than cooperating for an “Airbus of the auto industry,” which Renault’s chief executive calls for, Godement says the E.U. is witnessing a “race to the bottom” between member states to attract Chinese investment.

“The Chinese are having a field day extracting the best terms for investment,” he says.

Indeed, BYD courted both Germany and France before ultimately deciding on Hungary for its first EV factory in Europe. Within the E.U., Hungary received over half of new Chinese EV investment in 2022 and 2023 — including a $7.6 billion battery plant in the eastern city of Debrecen to supply Volkswagen and other European automakers.

Hungary has long been an automotive hub in Europe, but it is also viewed as “a geopolitical safe-haven by Chinese EV and battery makers,” according to Rhodium’s Sebastian, because it has opposed the China de-risking agenda advanced by Brussels as well as E.U. sanctions against Russia’s invasion of Ukraine. On his recent visit to Budapest, Xi Jinping celebrated Hungary’s “independent” foreign policy.

Critics also say that Chinese investments in Hungary, Spain and elsewhere aren’t really strengthening the E.U.’s manufacturing capacity because they are essentially assembly-only plants. By contrast, when Japanese automobile makers began investing in Europe to avoid trade controls in the 1980s, European governments demanded that Nissan and others meet high local content requirements for new factories. Sourcing claims were at times disputed, but over the years some Japanese automakers reached 80 percent local content.

Alicia García-Herrero, Chief Economist for Asia Pacific at French investment bank Natixis, says that today, “even if Chinese investments are only assembly,” the E.U. is letting it slide in order to “tick the box” of its reshoring efforts.

“Right now,” adds Gavekal’s Xie, “the E.U. is keen to extract the growth benefits of this new investment, but not equipped to extract the developmental benefits of technological innovation, managerial knowhow, and industrial upgrades that China is very well practiced in extracting from foreign companies.”

But, after all the years spent gaining first-mover advantage, why would Chinese companies agree to offshore considerable manufacturing capacity? European and other foreign automakers long commanded large shares of China’s market — why shouldn’t Chinese EV makers enjoy the same position in western markets?

For starters, Brussels does have leverage over Beijing. At a time when green industries represent critical growth drivers for the Chinese economy, it is worth remembering that the E.U. took in close to 40 percent of China’s EVs last year. There is also the fact that, like their western counterparts long believed, Chinese EV and battery makers think they can stay ahead.

“Chinese companies have built up a certain level of confidence in this space and believe they can create innovation and push the technological frontier faster than anyone else,” says Edward Tse, founder of Shanghai-based Gao Feng Advisory.

If the Chinese refuse to play ball, Godement recommends that the E.U., under the World Trade Organization’s (WTO) “public order” exception, establish investment criteria over the entire industry which, for example, set terms for supplier localization.

“An E.U. ‘buy European’ requirement would be open to a WTO challenge,” says Brad Setser, senior fellow at the Council on Foreign Relations. “But if it was challenged by China, there would be plausible defenses centered around the fact that China itself has not lived up to the letter and spirit of its own WTO commitments.”

Experts argue a large, new E.U. green investment fund could then enable scale for EV-manufacturing and a European battery supply chain.

“I would like to see the E.U. and the German government focus on reining in bureaucracy and develop a positive agenda to industrial policy with specialized investment, tax incentives and efforts to reduce the burden of high energy prices,” says Stefan Gätzner from the German Federation of Industries.

“The European Union must remain attractive as an industrial base,” adds a Mercedes-Benz spokesperson.

Europe’s bout with Japanese automakers going West in the 1980s may offer a final lesson for the E.U. on Beijing’s response to any major industrial policy shifts.

As business historian Grace Ballor notes, the Japan solution was only possible because Tokyo was a negotiating partner with Europe. Jacque Delors, then President of the European Commission, impressed upon his Japanese counterparts that: “European car companies [simply] need a certain amount of time to [be ready to] face international competition.”

In turn, then-Prime Minister Toshiki Kaifu took a political, rather than a purely economic, approach, and Japan’s leaders, who had aspirations of establishing a long-term presence in western markets, accepted “voluntary” export controls, quotas and local content rules in “Fortress Europe.”

Japan still lost sizable exports. Europe’s automobile sector still shed 400,000 jobs, a figure representing a quarter of the industry’s employment at the time. But a full blown trade war was averted.

Given today’s geopolitics, it’s difficult to imagine Chinese leadership offering the E.U. any space to play catch up. But while European consumers may benefit from lower prices of made-in-China EVs in the short run, the ripple effects could force the E.U. down a more American road. As the continent’s finest soccer players prepare to lace up their boots in Germany, BYD must surely be wondering if the European home crowd may soon enough turn hostile.

Luke Patey is a senior researcher at the Danish Institute for International Studies. He is author of How China Loses: The Pushback Against China’s Global Ambitions. His work has been published in The New York Times, Financial Times, The Guardian, The Hindu, Foreign Affairs and Foreign Policy. @LukePatey