One unseasonably warm weekend in March, executives from some of the largest Western mining firms moped around a convention center in Toronto, Canada. The glum atmosphere was a stark contrast to the much more celebratory feel of mining conferences in recent years. Just three years ago, Robert Friedland, the eccentric founder of Ivanhoe Mines, told mining executives that they were about to “make more money” than ever before: After decades of being shunned as a dirty industry best kept offshore, the clean energy transition and concerns in Western capitals about supply chain security had remade mining in North America into both an environmental and political imperative.

“So many people in the average workforce are now aware of the importance of metals and minerals,” Michael Stanley, mining sector lead at the World Bank Group, told a packed auditorium at the Prospectors & Developers Association of Canada’s convention in March. “But if that’s the case, how do we reconcile this?”

He was gesturing at a slide showing a steady decline in capital expenditure into mining through 2027. The lack of investments, he said, represented a time of “very constrained capital access” that was threatening the renewable energy transition.

It wasn’t supposed to be this way, several mining executives said at the conference.

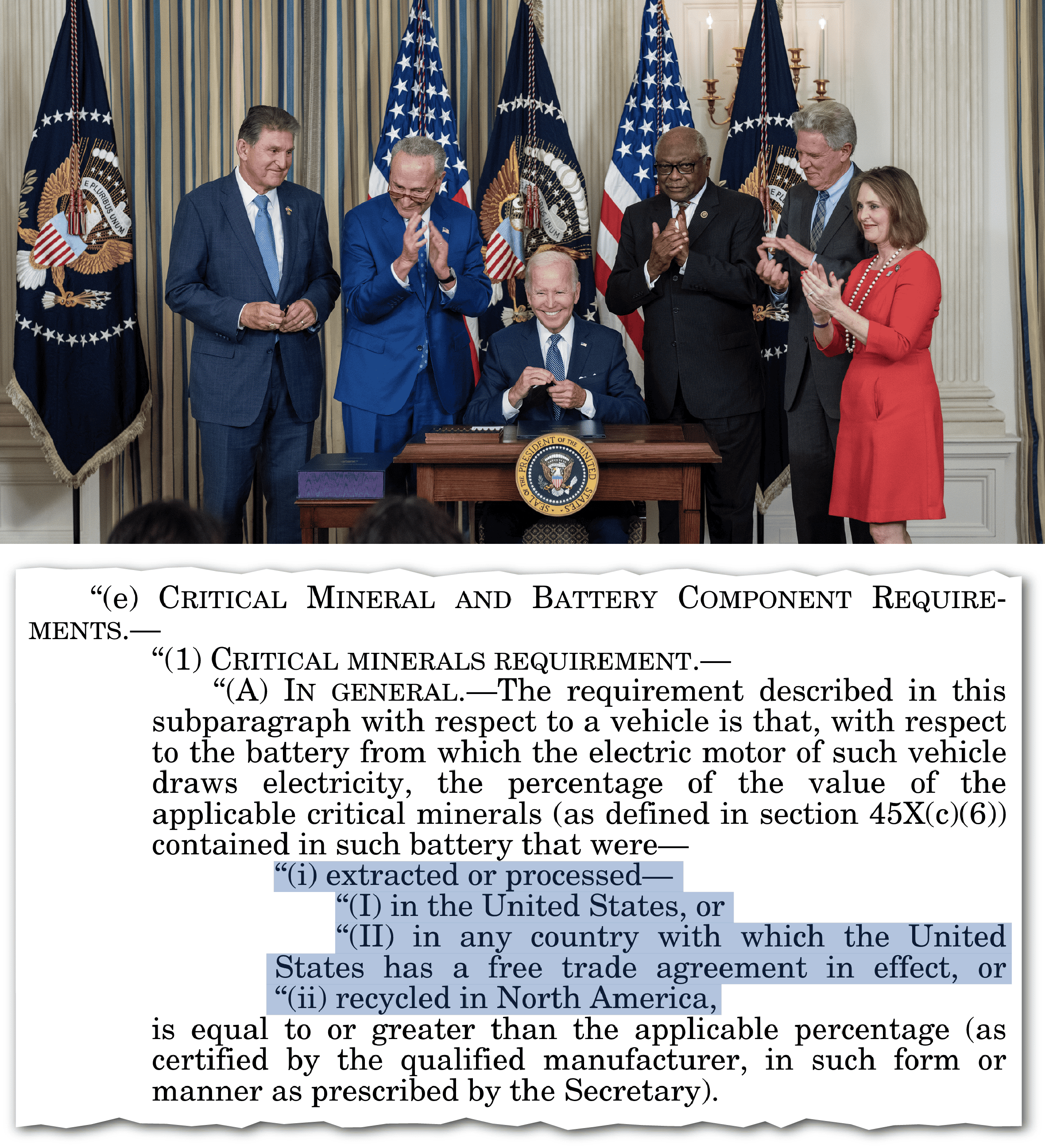

Credit: The White House, Congress.gov

Washington’s $370 billion Inflation Reduction Act (IRA), which was passed in August 2022, was seen as a generational opportunity for miners in the U.S. as well as mineral rich trading partners such as Canada and Australia. The IRA included a $7,500 per car clean vehicle tax credit, but for an electric vehicle to be eligible, the car, its batteries, and the vast majority of the minerals found inside those batteries have to be sourced, processed and manufactured in the U.S. or free trade partner countries.

With such a high bar, just 43 EV models are currently eligible for subsidies, down from 53 last year. But policymakers hoped the incentives would turbocharge investment all the way up the battery supply chain in Western countries — all while slashing America’s reliance on China, which currently dominates the production of batteries and their raw material inputs such as lithium, nickel and cobalt.

Since the passing of the IRA, battery and auto makers have announced some $110 billion in planned investments in North America. And yet, at the PDAC convention, representatives from the mining sector kept lamenting the same problem: Where’s our cut?

“We’ve seen striking numbers since the passing of the IRA,” Michael Torrance, chief sustainability officer at the Bank of Montreal, said. “But almost none of it is in mining.”

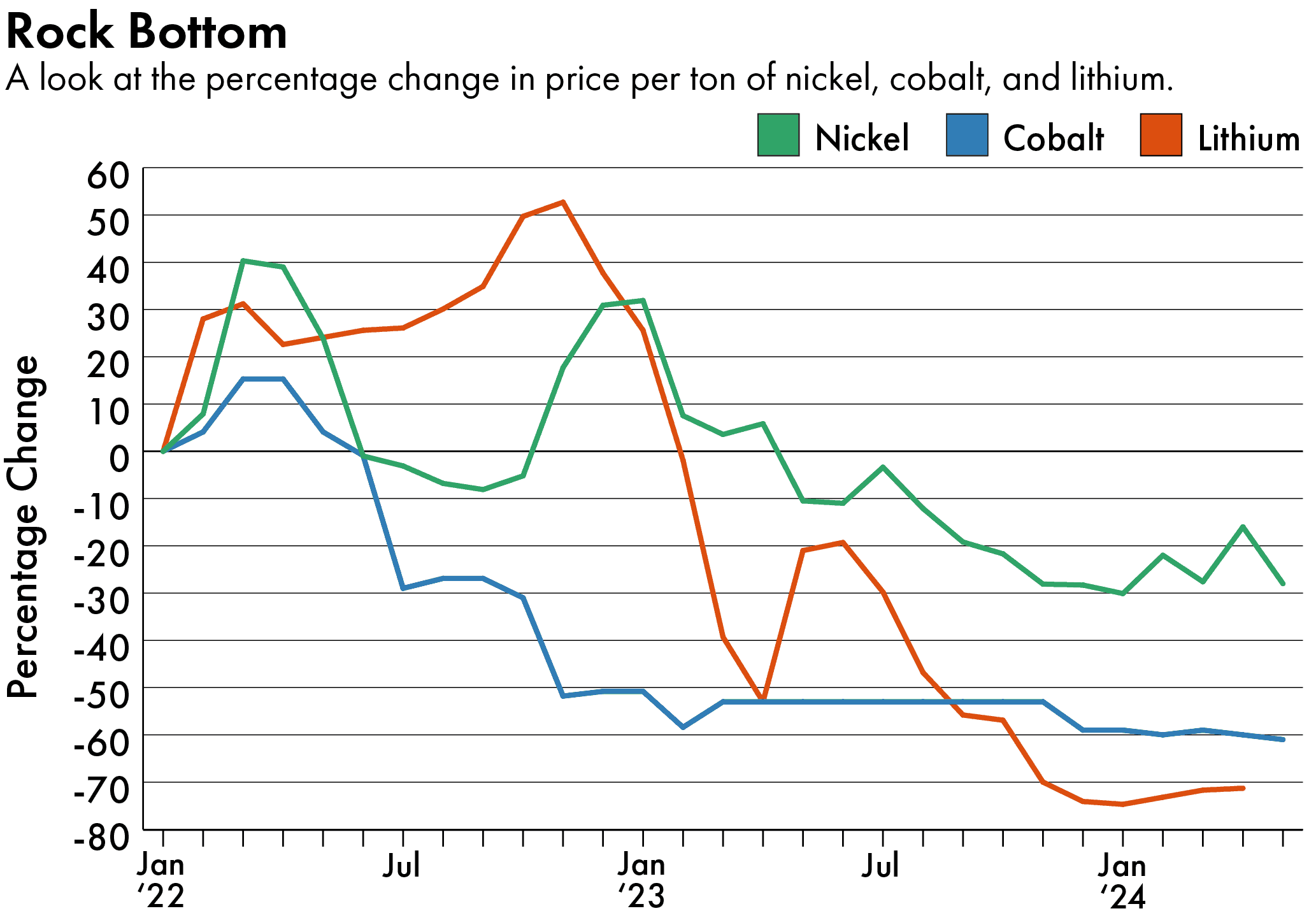

Aggravating the mining industry’s problem is that battery mineral prices have crashed over the last year: Lithium is down almost two-thirds from its 2023 high, while nickel and cobalt prices have fallen by half over the last year.

The mining sector is no stranger to boom and bust cycles, but rarely has the bust coincided with surging longterm demand and strong political support.

“We stand at a mineral price paradox: You see these continually falling prices and negative sentiment around pricing coming at a point where you continue to see massive growth in EV production,” Andrew Miller, chief operating officer at Benchmark Mineral Intelligence, said.

The strategic direction that [the government] wants the industry to move towards does not match up with the level of government support… it’s going to take much more money than what has been given.

Tom Moerenhout, a research scholar at Columbia University’s Center on Global Energy Policy

Battery mineral prices have collapsed due to a confluence of issues. For one, demand for EVs in the west has fallen short of expectations, with consumers deterred by the cost of vehicles and high interest rates. But equally at issue is the near-relentless determination by Chinese producers to ramp up production, even as the price of minerals continues to fall.

In China, producers backed by deep-pocketed battery makers like Contemporary Amperex Technology Co. (CATL) — the world’s largest EV battery manufacturer — have aggressively pursued costly new mines at home. Chinese producers in Indonesia, meanwhile, have helped raise the country’s nickel output from 7 percent of the global supply to 44 percent over the last decade.

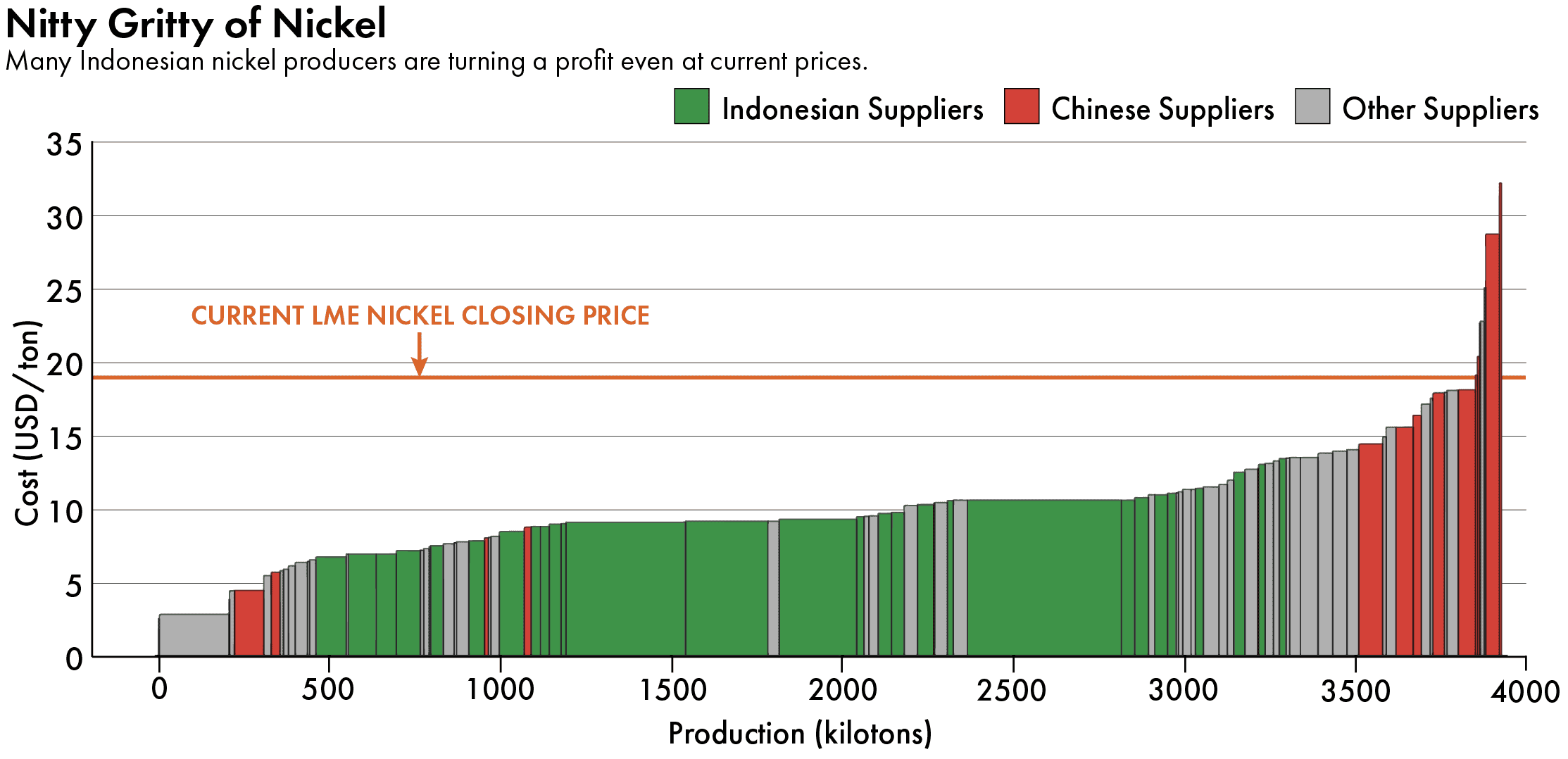

Mining projects in U.S.-allied countries, by contrast, have been thrown into crisis by the sudden price drops, forcing many to lay off workers and idle production. By one estimate in February, about half of the world’s nickel mines are currently unprofitable.

“Are capital markets rewarding low-carbon operations? In a very simple answer: no,” Jakob Strausholm, chief executive of Rio Tinto, the world’s second largest mining company, said at the conference. “The world needs to ascribe it some kind of value … otherwise decarbonization will not work.”

Governments are painfully aware that they need to intervene in the market if the “green transition” has any hope of succeeding. In March, the Australian government took extraordinary steps to rescue the country’s ailing nickel sector, providing tax breaks and low-interest loans to teetering producers. In the U.S., the Department of Energy has formally asked producers to submit solutions on how to support the industry, and it made a significant first step this week, by clarifying for the first time that mining projects are eligible for up to $72 billion in loan guarantees.

“This decision is a potential game changer for responsible mining projects in the United States because it can level the playing field with Chinese developed mines,” says Todd Malan, chief external affairs officer at Talon Metals, an American nickel mining firm. “For projects that can obtain conditional financing from the [Loan Programs Office], it will help get them built and also be a sign of strength to investors.”

But is it too little, too late? From exploration to permitting to production, it takes between eight and fourteen years to get a mine up and running in North America. With countries on the clock to meet their climate goals, every day of inaction will be felt far into the future.

Eagle Mine, an underground, high-grade nickel and copper mine in Michigan. Eagle is currently the only active primary nickel mine in the United States. Credit: Eagle Mine

“The strategic direction that [the government] wants the industry to move towards does not match up with the level of government support,” says Tom Moerenhout, a research scholar at Columbia University’s Center on Global Energy Policy. “What the [Department of Energy] has been doing on the battery supply chain is impressive. But even if they’re extremely hard working and committed, it’s going to take much more money than what has been given.”

Especially as China continues to pump out minerals at an unbeatable rate and Chinese companies continue to find ways to squeeze into U.S. EVs.

DIGGING IN

China’s miners have not only managed to stay afloat amid the price crash — they are also expanding their production and market share. Despite the low prices, for instance, analysts forecast that Indonesia’s nickel industry, which is dominated by Chinese companies, will add capacity this coming year.

Many mining sector observers are mystified by the development, with some competitors and policymakers smelling a conspiracy, believing that China’s producers are colluding to drive rivals out of the market.

There are reasons to be suspicious. In response to U.S. export controls over high performance semiconductors and manufacturing equipment, Beijing has repeatedly leveraged its grip over critical minerals. In December, for instance, China introduced controls over the export of graphite, a key component in battery anodes. The country has also imposed restrictions over the export of gallium and germanium, two minerals with important uses in the defense industry.

Now, some politicians are suggesting that the flood of cheap nickel may be a form of market manipulation. “It is our belief that that behavior can be intentional, can be happening with the purpose of driving companies in our country, [and] in those of our allies, out of business,” Canada’s finance minister, Chrystia Freeland, told reporters in April.

U.S. Ambassador to Australia Caroline Kennedy also described the dynamic in Indonesia as “unchecked exploitation by state-owned Chinese companies.”

“We can’t let them destroy vulnerable communities and the markets for Australian minerals under the guise of economic development,” she said in a speech last month.

But some longtime nickel analysts see a much simpler explanation for why Indonesian producers are thriving at these prices: because they can.

“They have labor and ore on tap,” says Angela Durrant, a senior metals analyst at CRU Group, who recently visited a Chinese nickel operation in Indonesia. “The original reason to go to Indonesia was because of cheap power. It has its own captive coal supply… which is one of the key drivers in keeping costs down.”

Chinese producers are also adept at getting new mines up and running fast, mitigating one of the factors that frequently deters would-be investors in the West from putting their money into mining.

Chinese producers “have economies of scale and learned experience in how to build things,” says Jim Lennon, managing director for commodities at Macquarie Group. “Their capital costs are a fraction, so their capital payback [time] is a matter of two to three years, versus ten to twenty years [in the case of a Western mining company].”

Vertical integration between mines and manufacturers has also helped to steel some of China’s industry against price fluctuations. For instance, major Chinese battery makers, including CATL and Gotion High-Tech Co., have invested in domestic lithium extraction projects, even though the cost of processing the type of lithium ore found in China, known as lepidolite, is higher than operations in the U.S. or South America.

“If you’re more integrated,” says Henry Sanderson, executive editor at Benchmark Minerals Intelligence and author of Volt Rush, “you can sustain losses in one part of your supply chain.” As the price of lithium falls, Chinese battery makers will still stick with their overpriced Chinese producers “for security of supply,” according to Sanderson. “It means [the market] is not necessarily rational in how it behaves.”

Chinese producers are not immune from the current pricing chaos, however. Two of China’s largest lithium miners, Ganfeng Lithium and Tianqi Lithium, have seen their share price plummet over the last year. And some Chinese suppliers are starting to complain that companies are undercutting one another in a race to the bottom.1According to reporting by Reuters that cited anonymous sources, China’s lithium producers agreed in March to set a floor price for their product. But Ganfeng Lithium, a major Chinese lithium producer, denies any such conversation took place. At China’s annual “Two Sessions” legislative conference in March, Chen Xuehua, chairman of Huayou Cobalt, a major cobalt and nickel miner, publicly called on Beijing to step in and take control of the situation.

Some people think the Chinese are trying to kill the rest of the world’s producers. But there’s so much competition in the domestic Chinese market, they’re almost trying to kill themselves.

Jim Lennon, managing director for commodities at Macquarie Group

“Capacity utilization has dropped significantly, and some companies are facing great operational difficulties,” he warned, according to an article published in Shanghai Securities News. “Production lines have been suspended, product prices have been reduced, equipment has been idle, and there have been company layoffs.”

“Some people think the Chinese are trying to kill the rest of the world’s producers,” says Lennon. “But there’s so much competition in the domestic Chinese market, they’re almost trying to kill themselves.”

Sources: Company disclosures, WireScreen

The Chinese players that emerge on top, however, aren’t just winning the China market — they are also figuring out ways to crack into the U.S. market.

‘THE AMERICAN DREAM’

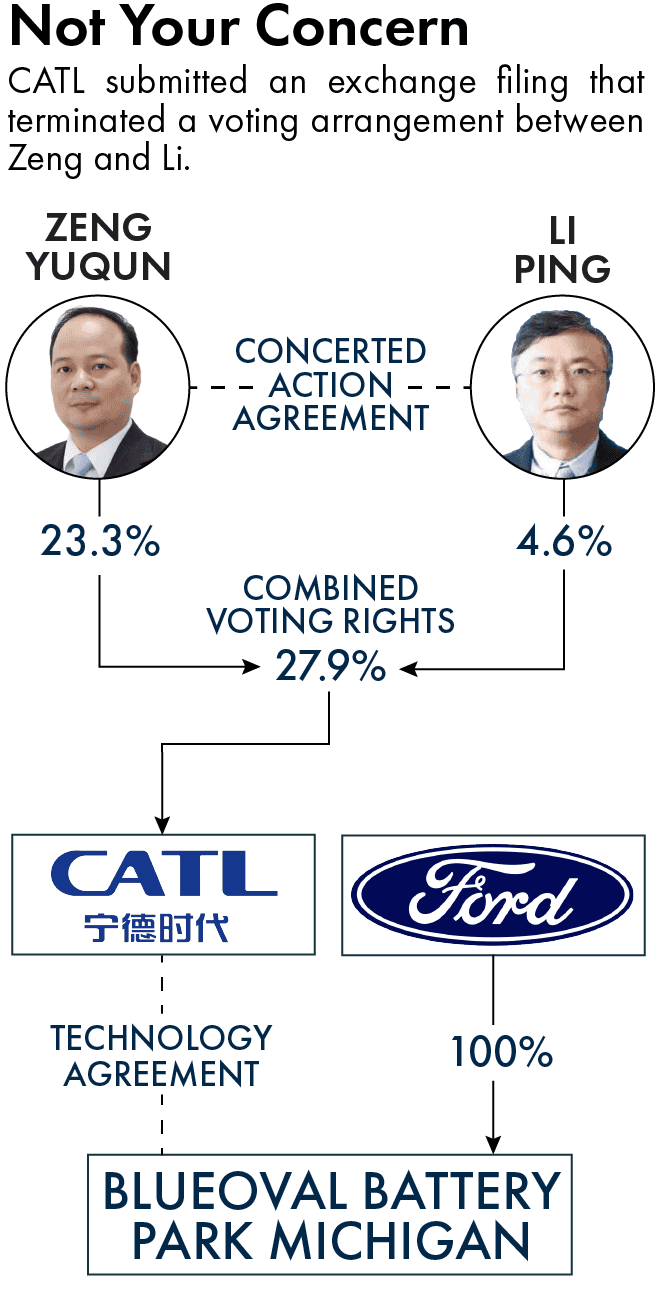

In early February, CATL submitted an inconspicuous exchange filing that terminated a voting arrangement between two top executives. Some analysts now say the simple adjustment has multi-billion dollar implications.

Under the IRA, EV makers that source minerals from companies deemed “foreign entities of concern” (FEOC) are prohibited from receiving taxpayer subsidies. These include companies owned, controlled or subject to the jurisdiction of the governments of China, Russia, Iran or North Korea. But, given China’s dominance in the field, the Department of Energy issued guidance in December that created an exemption for companies if less than 25 percent of its voting rights are held by entities affiliated with the Chinese government.

Since 2013, CATL’s founder Zeng Yuqun and vice chairman Li Ping have had a concerted action agreement that obligates them to vote together on company decisions. Zeng, who is a member of the Chinese People’s Political Consultative Conference, a top political advisory body, owns 23.3 percent of CATL. Li, who does not have a political affiliation, owns 4.6 percent. Their combined vote share of 27.9 percent thus risked putting CATL on the wrong side of the FEOC rule, imperiling its ability to work with U.S. companies looking to benefit from IRA subsidies — most notably Ford, which is building a $3.5 billion battery plant in Michigan with CATL’s help.

It is a crafty solution — but also one that some believe violates the intent of the IRA.

“There’s a fairness issue about U.S. taxpayer money going to adversarial interests to the U.S., particularly given Chinese content has already been subsidized by the Chinese state in innumerable ways,” says Frank Fannon, who served as assistant secretary of state for energy resources under the Trump administration. “Another issue is the stranded investment people aren’t going to make, because the Chinese have already captured the market.”

If Chinese batteries get a foot in the door of the U.S. market, Fannon argues that dreams for “a responsible, secure American supply chain” will likely never be realized. And it’s not just CATL pushing its way in.

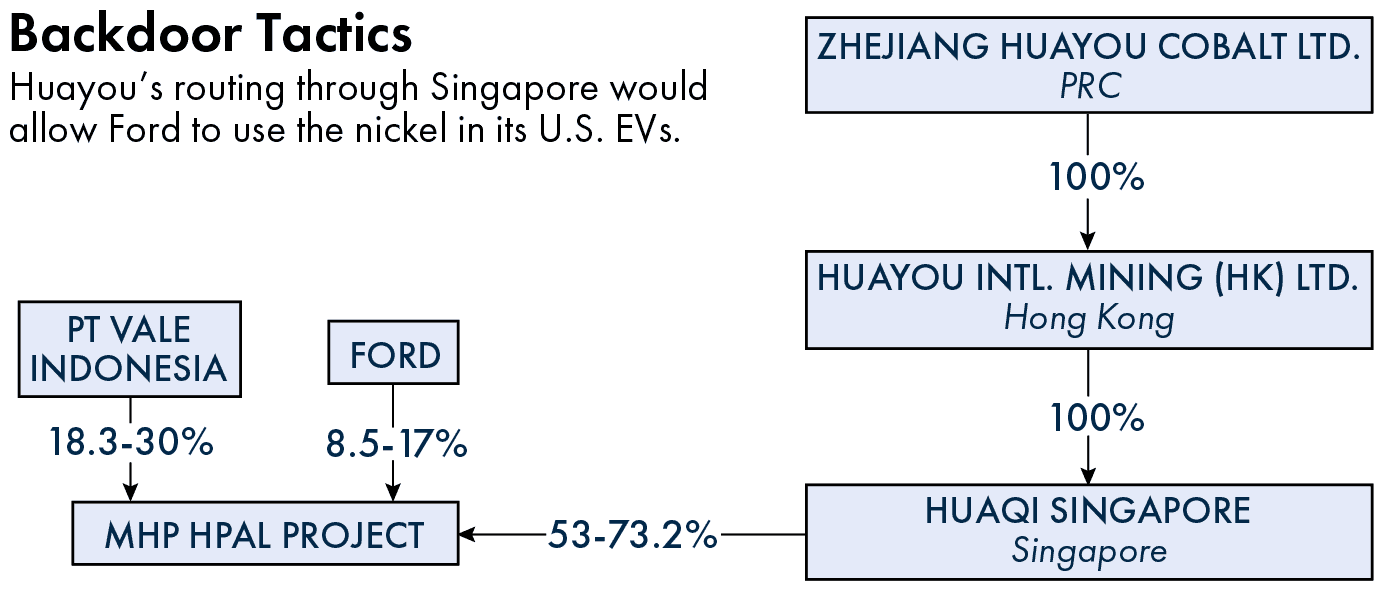

In Indonesia, Ford and Huayou Cobalt established a nickel processing joint venture last year alongside the Brazilian mining multinational Vale. Huayou Cobalt is the controlling shareholder in that JV, with a controlling stake of between 53 and 73 percent through a wholly owned Singaporean subsidiary.2The agreement leaves Ford and Vale the option to increase its stake in the future.

Left: Huayou’s Chairman, Chen Xuehua, PT Vale Indonesia’s CEO, Febriany Eddy, and Ford’s Chief Government Affairs Officer, Christoper Smith, sign a nickel agreement, March 30, 2023. Right: Indonesian President Joko Widodo delivers a speech at the signing event. Vale’s then Executive Vice-President of Energy Transition Metals, Deshnee Naidoo, is standing to his left. Credit: Vale, Huayou

Because the Department of Energy’s rules state that foreign subsidiaries of FEOCs are “not automatically considered” to also be FEOCs, Huayou’s routing through Singapore would likely allow Ford to use the nickel in its U.S. EVs.

On Friday, the Biden administration finalized the guidelines, cementing the 25 percent limit — and was immediately met with criticism. Rich Nolan, president of the National Mining Association, described the “loopholes” as “a blank check from the American Taxpayer to China.” Meanwhile, Senator Joe Manchin, the Democrat from West Virginia who played a pivotal role in getting the IRA passed in 2022, described the rules as “outrageous and illegal.”

Senator Joe Manchin on federal EV incentives, January 11, 2024. Credit: Senate Energy Dems

“I will lead a Congressional Review Act resolution of disapproval and will support any entity that has been negatively impacted by the illegal implementation of the law to restore the goal of domestic opportunity and security,” he said in a statement on Friday.

Some in the mining industry say it’s part of a pattern of neglect by policymakers in Washington towards the upstream sector. A longstanding call to shorten the permitting process, for instance, has gone unanswered. And draft rules issued by the Treasury Department in December disqualify the mining industry from a production tax credit introduced under the IRA to support the onshoring of clean energy technologies.

“If the final rule leaves out raw materials, Treasury would be excluding the entire beginning of the clean energy supply chain. That would be inconsistent with the intent of Congress and the administration’s own reshoring goals,” says Malan, of Talon Metals. Other mining firms, including Piedmont Lithium, a major U.S. lithium miner, have said that the absence of the credit might force them to relocate abroad.

Still, some analysts argue that small policy tweaks — like including mining in the tax credit — wouldn’t be enough to really kickstart mining operations in America. “The cost difference for some of the minerals where this problem is most pronounced is a whole lot more than the tax credit’s 10 percent,” says Columbia’s Moerenhout.

Others, including key U.S. allies, say it will be impossible for the U.S. to realize its clean energy goals in the short and medium term without some Chinese input. In an interview with The Financial Times in April, South Korea’s trade minister claimed the IRA subsidy regime “will collapse” without exemptions or a transition period, particularly for battery-grade graphite, which China controls more than 99 percent of the global market for. The Biden administration conceded that reality last week, providing a two-year extension for carmakers to de-risk their supply chain of Chinese-origin graphite.

More radical solutions to closing the gap with China involve rethinking the private market that determines how critical minerals are priced. A growing chorus of western nickel producers, for example, has been calling on the London Metal Exchange (LME), the world’s oldest and largest market for industrial metals, to introduce a “green premium” for sustainably produced material. Such an index would presumably exclude Indonesia’s nickel, which is one of the most polluting sources, and would incentivize western producers to kickstart production again.

In the past, the LME, which is owned by the Hong Kong Stock Exchange, has been reluctant to discriminate between metals on qualitative factors. The exchange declined to ban the trade of Russian metal after the invasion of Ukraine in 2022, for example, saying at the time: “We believe the LME should not seek to take or impose any moral judgements on the broader market.”3The exchange recently banned from its system Russian aluminum, copper and nickel produced after April 13 in response to U.S. and U.K. sanctions.

In March, the LME argued that the market for green nickel was not yet large enough to support trading, but some price tracking agencies disagree.

“We wouldn’t put out price indexes if people weren’t interested in them,” says Daisy Jennings-Gray, head of prices at Benchmark Mineral Intelligence, which established a sustainable lithium price in November and a similar product for nickel last month. “A lot of the interest has come from downstream. Western manufacturers know that in the future they need sustainable pricing, and they want a justification in the future for why they’re paying [higher] prices. Meanwhile, upstream producers want a justification for why they’re selling for more.”

The U.S. is an engine of R&D, and with this level of collaboration we can certainly innovate. The question is can we produce a leapfrog technology that can build things in a different way?

Frank Fannon, former assistant secretary of state for energy resources under the Trump administration

In the end, the future of North American mining will likely depend on an all-of-the-above approach, involving changes in government support, market forces and the actual technology of mining. Indeed, some say the U.S.’s only hope is to do what the U.S. does best: innovate.

“The U.S. is an engine of R&D, and with this level of collaboration we can certainly innovate,” says Fannon, the former assistant secretary of state for energy. “The question is can we produce a leapfrog technology that can build things in a different way?”

Talon Metals, the Minnesota-based miner, offered a glimmer of hope just this week. After working with the Argonne National Laboratory to leverage waste from its mining operations, the company announced a breakthrough that it says will allow it to quadruple the number of batteries it can supply per ton of ore.

If there was one hopeful message that emerged from the PDAC conference in March, it was that the mining industry would eventually embrace the kind of transformation many say is necessary. “As an industry, we’re a little slow to adapt,” Deshnee Naidoo, then-CEO of Vale Base Metals, told the audience. “But we do adapt.”

Eliot Chen is a Toronto-based staff writer at The Wire. Previously, he was a researcher at the Center for Strategic and International Studies’ Human Rights Initiative and MacroPolo. @eliotcxchen