This was supposed to be a breakout year for China’s stock markets. Buoyed by the post-Covid reopening and newly announced reforms to the way companies list, investors and bankers hoped the country would be a driver of growth while the rest of the world slowed.

Instead, dozens of Chinese companies have canceled their plans for an initial public offering at home — just months after China’s securities regulator had announced major changes supposedly designed to “give the right of choice to the market.” Earlier this month, Syngenta Group — the agricultural giant whose $9 billion IPO was slated to be China’s biggest this year — announced it would delay its listing until 2024, citing weak market conditions.

Regulators’ tough scrutiny of companies planning an IPO signals a shift towards extending state control over the private sector, in line with Xi Jinping’s efforts to gain a greater say over which companies and industries succeed in China. By hand picking which companies make it onto the stock market, however, Beijing risks stifling innovation and further depressing business confidence in the country.

“Here you have the state trying to control outcomes and dictate where money goes,” says Fraser Howie, independent financial analyst and author of Red Capitalism: The Fragile Financial Foundation of China’s Extraordinary Rise. “Just when you need good decision-making and good models, China is going the wrong way.”

Since January, more than 170 companies have withdrawn or canceled their plans to go public on China’s stock exchanges, a four-fold increase compared to the same period a year in 2021. Even companies operating in sectors that Beijing deems ‘strategically important’ can’t catch a break: Many of those withdrawing are in so-called ‘hard tech’ industries such as semiconductors, AI, biotech and clean energy.

They are clearly treating private companies as arms of the state that have to obey state priorities — however they may be defined.

Andrew Collier, managing director and founder of Orient Capital Research

Companies are being scrutinized not just for their contribution to industrial policy, but their competitiveness. Wuxi Si-Power Micro-Electronics Co., a chip supplier, withdrew its application in June after stock exchange officials sent them over a dozen questions, including why its inventory turnover was lower than its peers. After officials asked Shanghai Rongsheng Biotech Co., a biotech company, about the risk its profit margins would decline as a seller of generic vaccines, the firm withdrew its IPO application in August.

And in a third case, Yisa Technology Co., an AI startup which designs products for smart cities, withdrew its application to IPO on the Shanghai Stock Exchange’s STAR market, which focuses on firms closely aligned with Beijing’s industrial policies. That came soon after it responded to more than a dozen questions about its patents and the competitiveness of its core technology, as well its profitability, R&D spending, data security, and its employee social security program.

The three firms did not respond to The Wire’s requests for comment.

“These questions are way beyond what a normal exchange does,” says Andrew Collier, managing director and founder of Orient Capital Research. “They are clearly treating private companies as arms of the state that have to obey state priorities — however they may be defined.”

Merely receiving regulators’ questions is a deal breaker for many companies looking to list, because it can harm investor perceptions of the health of their businesses.

“The more questions that come in the more they can potentially get into trouble,” says Thomas Gatley, senior analyst at Gavekal Dragonomics, a research firm.

China has historically maintained strict oversight over which companies are allowed to list at home. Starting in the 1990s, the China Securities Regulatory Commission (CSRC) adopted an “approval-based” IPO process giving it the final say over which companies could list. During the nascent years of the stock market, this tended to benefit state-owned enterprises over private companies.

“[The CSRC’s] role from early on was as a gatekeeper, channeling funds to companies in need rather than who were deserving,” says Howie. “Throughout this there were voices calling for moving to a more genuinely market-based model, but it wasn’t really until the past decade that this started to develop.”

In 2019, China adopted a U.S.-style “registration-based” IPO system for the first time with the new tech-focused STAR Market in Shanghai, with supposedly laxer listing requirements. Unlike China’s main exchanges, STAR allows currently unprofitable companies to list, for example.

Under the registration-based system, the stock exchange enforces information disclosure requirements, but gives up its role as a final arbiter of whether firms can list. This February, the CSRC unveiled new rules to apply the system to China’s main boards in Shenzhen and Shanghai — although it maintained responsibility for ensuring that listings are in line with national industrial policy.

But rather than relinquish control over the approval system, the CSRC has in effect tightened its oversight through its increasingly detailed inquiries.

Regulators have so many different agendas they have to contend with. Right now, there is no time horizon for a registration-based IPO system similar to the U.S.

Gary Rieschel, a venture capital investor

Some experts disagree that this represents a total reversal of China’s pledged IPO reforms. “A registration-based system [in China] is not a signal that it’s open season for everybody to list no matter what industry you’re in,” says Gavekal’s Gatley. “They wanted to reduce the red tape so that not everything has to go through CSRC, but they’ve also strongly signaled what kinds of firms are permitted to list and what kinds are not.”

“Regulators have so many different agendas they have to contend with,” says Gary Rieschel, a venture capital investor. “Right now, there is no time horizon for a registration-based IPO system similar to the U.S.”

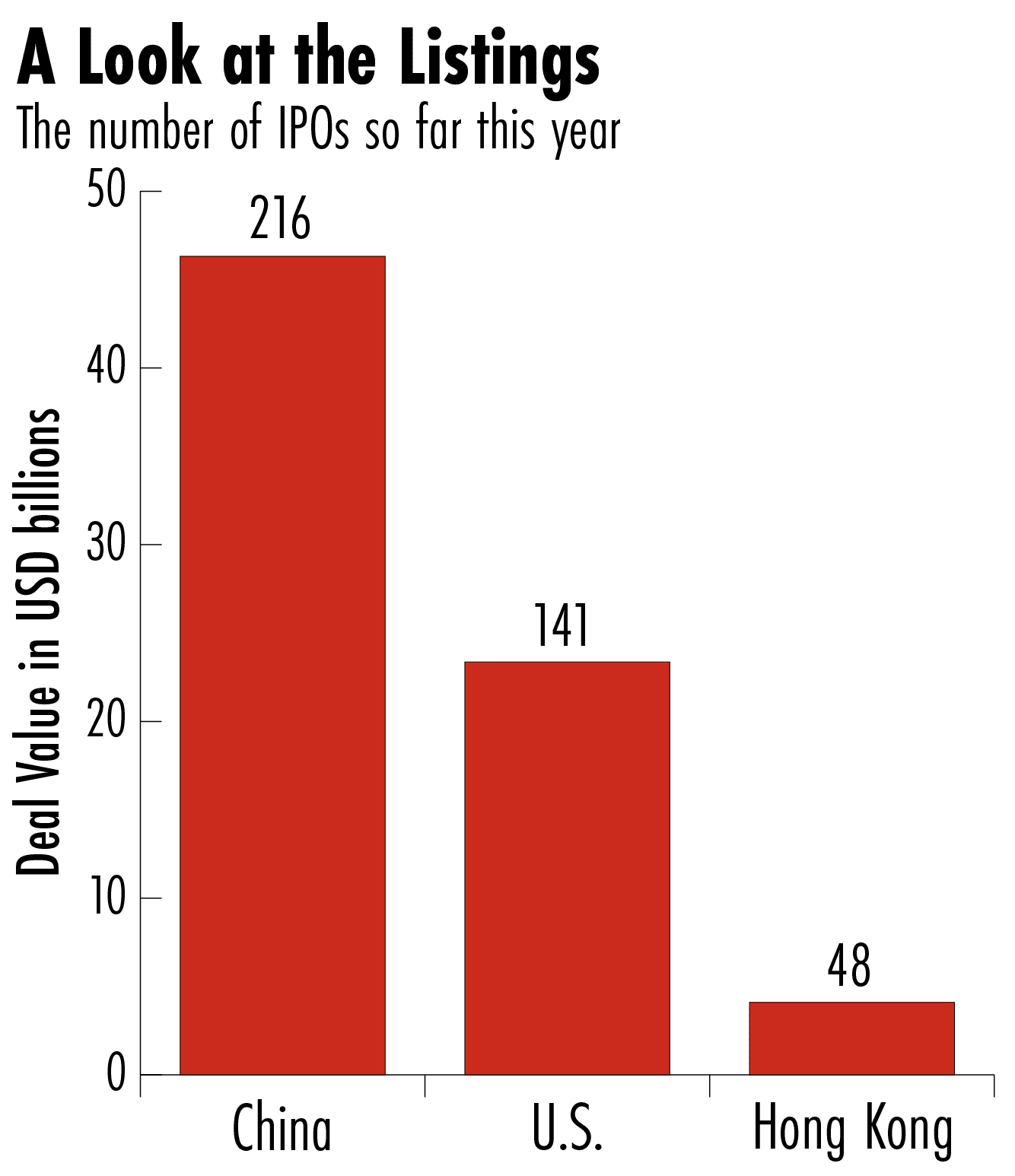

China remains on track to outperform the U.S. and Hong Kong in terms of the number and value of new listings this year. U.S. listings remain far behind China primarily due to higher interest rates, which have sent many tech stocks tumbling since last year. Newly listed companies since 2020 have largely underperformed, with a majority of firms that have listed since 2020 trading below their IPO prices. Prospective listers have been reluctant to IPO in this environment, while many of their industry peers’ stock prices remain depressed.

Still, with 215 IPOs to date this year at a total deal value of $46 billion, that is fewer new listings than the year before. And almost two-thirds of IPO applications have failed to win approval this year, more than double the rate compared to 2022.

One alternative route for companies that fail to secure listing approval on mainland exchanges is to list offshore, for example in Hong Kong. But under new rules that went into effect in March, the CSRC is also responsible for approving companies’ offshore listing applications. The agency has been similarly slow to greenlight those applications this year.

Broader economic headwinds also make offshore listings a bad bet. “Foreign sentiment about Chinese stocks has been at an all time low, so foreign liquidity in Hong Kong is very poor,” says Gatley. “On the other hand, the warming of geopolitical relations [following the Biden-Xi summit] could be very helpful, along with good earnings from Tencent and others. So if stuff goes in the other direction, particularly macro, then you could get potentially improved sentiment.”

Without an economic rebound, however, analysts predict that regulators will likely remain reluctant to open up the listing process. “Money is politicized,” says Collier. “In a time of tightening capital, the Politburo does not want money going to areas that aren’t beneficial.”

Eliot Chen is a Toronto-based staff writer at The Wire. Previously, he was a researcher at the Center for Strategic and International Studies’ Human Rights Initiative and MacroPolo. @eliotcxchen