Debt collection is the latest industry to face scrutiny from Beijing, as the authorities tighten up oversight of the country’s financial sector.

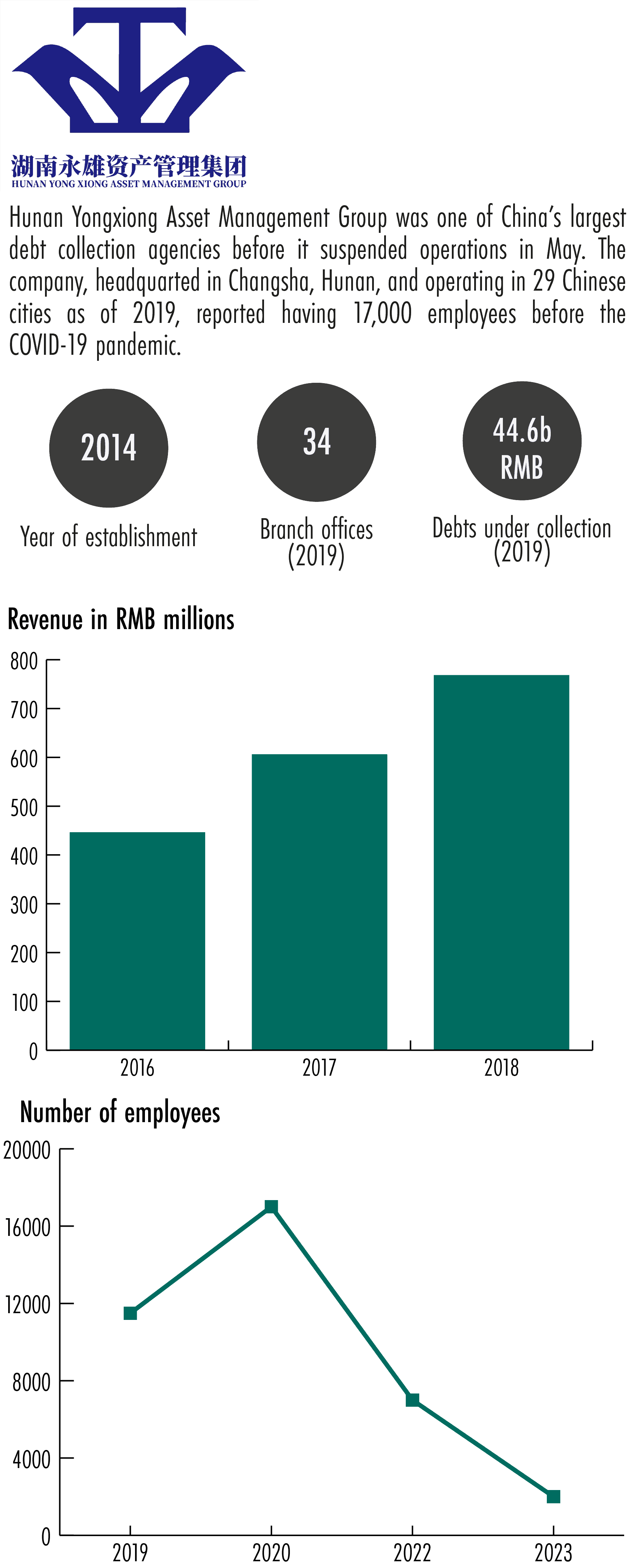

On May 25 Hunan Yongxiong Asset Management, one of China’s largest debt collection agencies, announced it was suspending its operations. In a WeChat post laden with emotional language, the company described a series of police raids at its offices across Hunan since early April, that resulted in 179 employees being detained or subject to other sanctions. At least three of those arrested have been accused of ‘picking quarrels and provoking trouble’, an infamously broad crime under Chinese law.

Debt collection in China is an industry synonymous with strong-arm tactics, but Hunan Yongxiong’s fall from grace has come at a time when Chinese regulators are working towards a standardized set of guidelines for a more ethical approach.

This week, The Wire looks at the rise and fall of Hunan Yongxiong, which once commanded an arsenal of more than 10,000 employees and had aspirations of listing on the New York Stock Exchange.

DROWNING IN DEBT

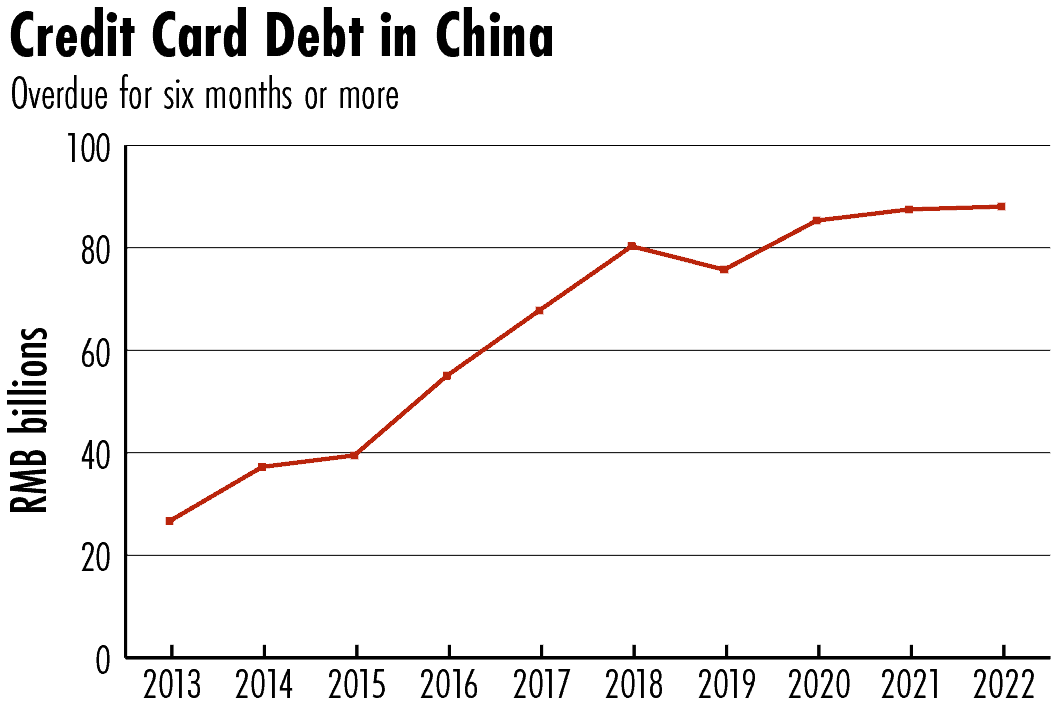

Consumer debt has been rising in China since before the pandemic, but the economic slowdown caused by Beijing’s zero-Covid approach has exacerbated the problem. The amount of credit card debt that had been overdue for at least half a year stood at more than RMB 86.5 billion ($12.85 billion) by the end of 2022, data from the People’s Bank of China shows. Disputes over loans and credit cards were the two most frequent types of commercial cases brought before courts in Shanghai in 2021, according to a white paper published by the city’s High People’s Court.

“Over the past ten years in particular, loans to households have become an incredibly important part of bank lending,” says Dinny McMahon, head of China Markets Research at research firm Trivium. While mortgages make up the majority of these loans, credit card lending accounts for a relatively high share of new loans, according to research written by McMahon and published by Macro Polo in 2019.

As credit card delinquency has risen, so has the role of debt collection agencies, whose numbers proliferated during the 2010s. Such firms typically receive a fee based on the size of the amounts they collect, with the percentage rising for older debts. Companies in the sector have long operated in a legal black hole, however, with few regulations governing best practices in the industry and no single regulator in charge of supervision.

That lack of oversight has contributed to intimidatory debt collection tactics becoming the norm. The MacroPolo report cites several examples of agencies’ bad behavior, including harassing phone calls, pressure being placed on debtors’ families and even collectors putting glue in keyholes to prevent delinquent payers from entering their own homes.

“Traditionally, the reputation [of debt collectors] wasn’t that positive, to put it mildly,” McMahon says. “Ultimately the goal was to use intimidation and embarrassment and shame and just pure frustration to get people to pay their debts.”

The Chinese authorities have taken some steps to tighten the rules around the industry, though gaps remain, particularly around agencies working on behalf of Internet finance platforms.

“In 2009, the banking regulator introduced rules which required the banks to take responsibility for the behavior of the debt collectors which they employed,” McMahon says. “The Internet sector was a little bit different. Early on, no regulator was stepping in and taking responsibility for closely regulating their behavior. It just kind of fell through the gaps.”

ONE COMPANY: HUNAN YONGXIONG ASSET MANAGEMENT

From its beginnings less than a decade ago, Hunan Yongxiong grew rapidly under the leadership of its founder and chief executive, Tan Man. By 2019, it had more than 11,000 employees and was pursuing some RMB 44.6 billion ($6.4 billion) worth of bad loans, according to a listing prospectus filed to the U.S. Securities and Exchange Commission.

Hunan Yongxiong credited its growth to 2019 to its accumulation of collection expertise, the sophistication of its IT systems and the development of China’s credit scoring infrastructure.

By the time of the company’s planned IPO, it was the largest agency in China dealing with delinquent credit cards, with a 16.6 percent share of debts collected and more than twice as many staff as its closest competitor, according to iResearch, a consulting firm.

In retrospect, its plan for an initial public offering was a high point for the company. Its application was withdrawn within weeks of the prospectus being filed. While the reason was not publicly disclosed, the withdrawal coincided with a hardening attitude towards the debt collection industry inside China.

In January 2018, the State Council had issued a notice “concerning the launch of a special struggle to fight crime and suppress evil.” The notice called on all administrative and judicial bodies to take strong measures against “all kinds of underworld forces” that engage in illegal activities. While the notice did not elaborate on the targets of this campaign, it has since been cited by local governments in crackdowns against aggressive debt collectors.

Against this backdrop, Hunan Yongxiong’s founder, Tan Man, continued to attend industry events in Hunan with local government officials. While its financial performance data for recent years are sparse, the company’s employee numbers were dwindling, falling to just 2,000 in the last few weeks before the company suspended operations.

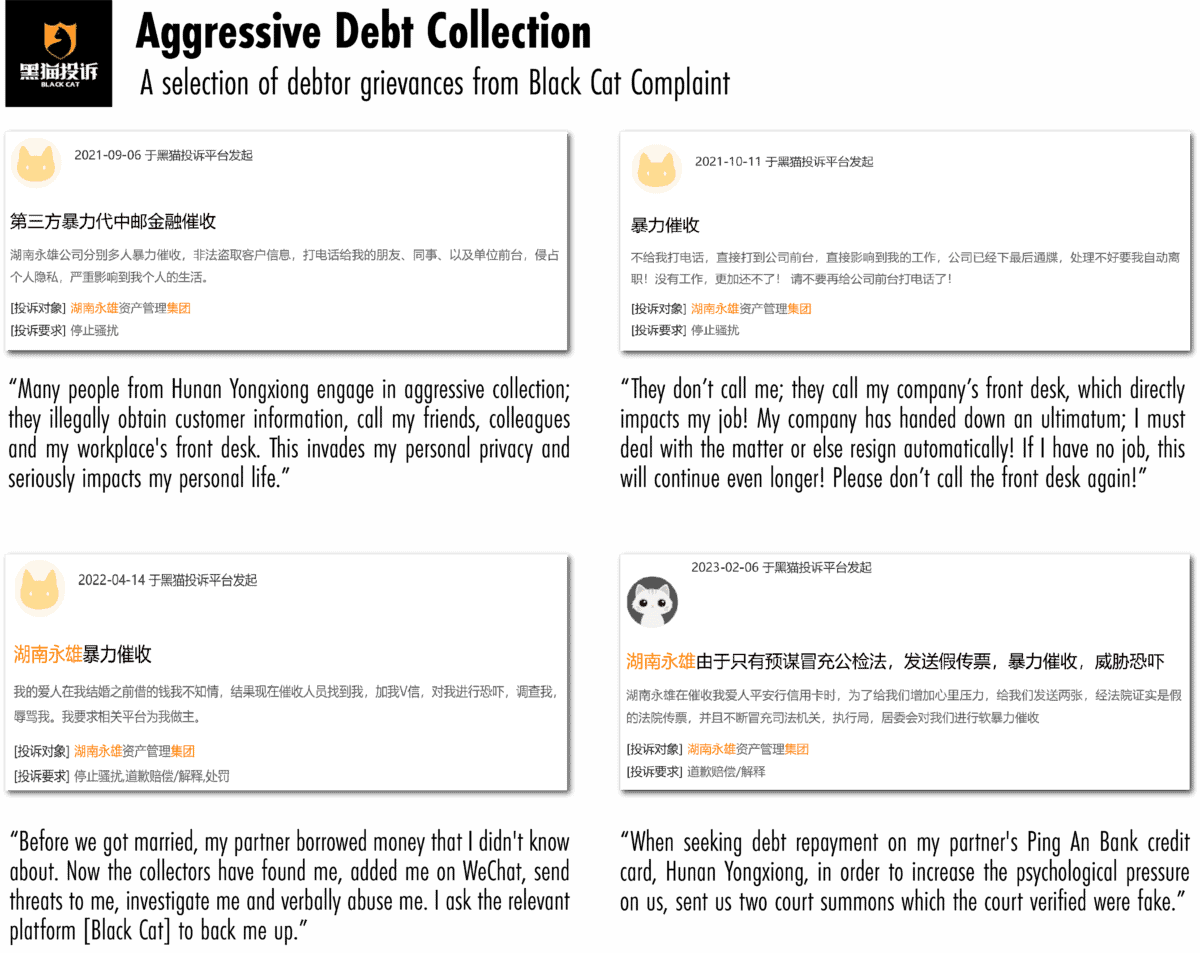

Publicly available testimonials on Black Cat Complaint, an online platform for aggrieved customers and clients operated by Sina Corporation, tell a negative story about the firm’s practices in recent years.

In its statement announcing the company’s suspension of operations, Hunan Yongxiong denied engaging in illegal activities, adding that if individual employees are suspected of violating regulations, they would be dismissed, while the leaders of their branch offices would be demoted with salaries cut.

THE FUTURE OF DEBT

Although Hunan Yongxiong’s fate is uncertain, China’s debt collection industry appears set for a revamp. Draft guidelines by the National Internet Finance Association of China on online consumer lending and collection practices have been open for public consultation since 2020, and continue to be discussed by industry stakeholders. If implemented, the guidelines would prohibit debt collectors from making calls at unsociable hours unless mutually agreed, and falsely claiming to represent a law enforcement agency. Contacting anyone other than the debtor would also be subject to stricter conditions.

However, any new rules could be tricky to implement, given the sheer number of debt collection agencies across China that are nowhere near the size of Hunan Yongxiong at its peak.

“Often debt collecting operates very locally,” McMahon says. “Local officials can often turn a blind eye with a wink and a nod. They’re often too small to garner much attention, so it might be quite difficult [to tighten regulation].”

Aaron Mc Nicholas is a journalist based in Washington DC. He was previously based in Hong Kong, where he worked at Bloomberg and at Storyful, a news agency dedicated to verifying newsworthy social media content. He earned a Master of Arts in Asian Studies at Georgetown University and a Bachelor of Arts in Journalism from Dublin City University in Ireland.

{kind=link}