In April 2018, Zhao Weiguo, the chief executive of Tsinghua Unigroup, took Chinese President Xi Jinping on a tour of a semiconductor facility in Wuhan. At the time, Unigroup, the partially-state-owned semiconductor company, was five years into its aggressive campaign to design and manufacture more advanced chips — a campaign inspired, in large part, by Xi’s wish to sever China’s reliance on foreign suppliers. The photo op of the two men strolling in matching white lab coats seemed to offer proof that everything was proceeding as planned.

As Zhao went on to boast — on multiple occasions — the general secretary had wished him a happy birthday during the tour, which was “not just an encouragement for me, but for the entire Chinese semiconductor industry,” he said.

Indeed, Zhao is one of the best known faces of the Chinese semiconductor industry. Bespeckled and portly, he has a reputation for being a daring and pugnacious businessman. Unlike China’s other top chip champions — SMIC, Hua Hong and Huawei’s HiSilicon — Tsinghua Unigroup operated less like a technology company and more like a venture capital or private equity firm under Zhao’s stewardship. The company became “known for having a lot of money, doing acquisitions and being willing to go bold,” says J.D. Lau, who has worked in sales for various chip firms in China and East Asia.

The strategy seemed to work. When Zhao took over Tsinghua Unigroup in 2009, the Tsinghua University-adjacent firm1Until recently, the university owned 51 percent of the firm. was struggling with both its purpose and its profits. Zhao shifted its focus from consumer electronics to semiconductors at the perfect time: just four years before Beijing published its National Integrated Circuit plan, a component of the Made in China 2025 initiative, which called on China to domesticate 70 percent of its semiconductor needs by 2025 and reach parity with leading international chip companies by 2030. Beijing went on to flood the industry with an estimated $100 billion.

Zhao put all that money to use. He identified high performing smaller companies and gobbled them up — spending tens of billions in the process. Unigroup now has 286 subsidiaries, two of which — UNISOC and Yangtze Memory Technologies Co. (YMTC), an Apple supplier — are major players in the global chip industry, specifically for older model chips, such as chips for 3G.

Given his swashbuckling style, Zhao — himself worth $2.2 billion last year — earned the nickname “the semiconductor madman” within the industry. Yet, like any madman, Zhao’s daring had a downside.

According to industry insiders, he developed a reputation as something of a “serial bullshitter,” with a penchant for excessive self-promotion. For instance, numerous sources indicate that Zhao was born in November — not April, which is when he claimed Xi Jinping wished him a happy birthday.

He is also not known for being particularly strategic or wise in his financial decisions.

“Unigroup threw money around in this extraordinarily wild and reckless fashion,” says Chris Miller, an economic historian at Tufts University and author of Chip War: The Fight for the World’s Most Critical Technology. “If you’re looking to attract attention, Zhao knew how to do it.”

And attract attention he did. In July, Zhao, 55, was arrested alongside a dozen other leaders from China’s state-managed semiconductor industry.

No charges have been publicized — elite machinations in China are notoriously opaque — but the arrested individuals were targeted for “serious violations of discipline and laws,” which often implies corruption.

Others jailed include Xiao Yaqing, China’s Minister of Industry and Information Technology (MIIT); Ding Wenwu, manager of the “Big Fund”2Formally known as the National Integrated Circuit Industry Investment Fund., Beijing’s $50 billion quasi-governmental chip investment fund launched in 2014; and Diao Shijing, a former co-president of Unigroup. Others connected with the Big Fund, from academics to venture capitalists, have also been arrested or are under investigation by the Central Commission for Discipline Inspection (CCDI), an anti-corruption body.

While many observers say the arrests signify Beijing’s recognition of the enormous graft plaguing China’s chip industry, there are open questions about what the microchip dragnet means for the industry’s future, especially as Beijing’s ambitious goals come crashing into roadblocks from Washington.

With reports that state-supported semiconductor firms have been overstating their progress, some observers interpret the dragnet as, perhaps, a menacing goad. “You could look at this as a case of the government not being happy with the way that the whole semiconductor process has been moving,” says Jay Goldberg, an industry consultant focused on China. “They want to encourage change.”

I think Beijing was trying to send a signal that the current crop of people [leading the industry] are dirty, corrupt and not up for the task. They may have been what China needed in 2014, but they’re not the people that China needs in 2022.

an anonymous semiconductor industry insider

Others chalk the arrests up to high-level factional politics within the Party. “If this was just about corruption or missing pennies, they’d be doing this everywhere, all the time. This is something different,” says Alex Payette of the Cercius Group, a consultancy that tracks Chinese elite politics. Zhao, who is reportedly friendly with Hu Jintao’s son, Hu Haifeng, may have been seen as part of the “old regime,” Payette adds.

Whatever the reason, Beijing certainly has grounds to worry about its chip drive. Despite the dizzying sums invested into it, the industry remains years, even decades, away from achieving global dominance. Foreign firms are forecast to supply over half of China’s chip consumption until at least 2026, according to IC Insights, a U.S. semiconductor research group.

This is, of course, how the U.S. wants it to be. Since advanced microchips are critical to 21st-century technological supremacy, the U.S. has a strong incentive to subvert China’s ambitions and has, over the past seven years, instituted a series of crippling sanctions on semiconductors.

“If you think of technology as a key enabler of economic, political and military power, you do not want to see your adversary become the one that prevails in technological competition, where there is so much at stake,” says Martijn Rasser, a Senior Fellow at the Center for a New American Security and former C.I.A. analyst. “The emphasis [in the U.S.] is now shifting from keeping China a few generations behind [in semiconductors] to making the gap in capabilities as large as possible.”

Some observers see the arrests in this context, arguing that they represent a recognition by the Party that the playing field has changed considerably since Zhao arrived on the scene and China’s semiconductor goals were originally set.

“I think Beijing was trying to send a signal that the current crop of people [leading the industry] are dirty, corrupt and not up for the task,” says a semiconductor industry insider who knows Zhao but is not permitted to talk to the press. “They may have been what China needed in 2014, but they’re not the people that China needs in 2022.”

SEMI-CHARMED LIFE

Falling afoul of the Chinese Communist Party seems to run in Zhao’s family. Both of his parents hailed from families with politically problematic histories, and the couple met and married in Xinjiang after being exiled there during an “anti-rightist” campaign in 1957. Zhao was born in 1967, and his childhood in Xinjiang during the Cultural Revolution was spent herding goats in a distant village.

After Mao Zedong died, in 1976, the family was “rehabilitated” and relocated to Shawan County in northern Xinjiang. There, Zhao doubled down on his studies, graduated from high school and tested into Tsinghua in Beijing, China’s most prestigious university, to study electronic engineering.

In college, Zhao devoured a translation of Silicon Valley Fever, a 1984 book about Apple and Hewlett Packard, which sparked an entrepreneurial drive. For extra cash, he repaired televisions. After graduation, he worked for an I.T. firm in Zhongguancun, a Beijing district known as “China’s Silicon Alley.” And in 1993, he returned to Tsinghua to pursue a Masters degree.

Tsinghua had recently begun commercializing some of its research, in part to augment low teacher salaries in a weak and battered economy. On the recommendation of a professor who recognized Zhao’s business zeal, he was hired, in 1997, to head a new electronics company, Tsinghua Tongfang, which was a subsidiary of Tsinghua Holdings, the umbrella group which owns Unigroup.

The head-strong Zhao had a particular penchant for acquisitions and mergers. His first purchase for Tongfang was a state-owned supplier of satellite technology to the People’s Liberation Army, which he converted into a successful manufacturer of products for power plants. He also invested in a healthcare website and managed to sell it for a profit before the Dot Com Bubble popped.

Although Zhao had not grown up with particularly impressive family connections or networks, his success at Tsinghua University and its affiliated companies started to give him exposure and access to Beijing’s most elite circles.

But Zhao’s real break came when Tongfang acquired Xinjiang Gas Group. He was appointed chairman and relocated to the region, his childhood home, in 2004. While there as a gas company executive, Zhao discovered a passion for the real estate business. China had recently privatized its housing market, and Xinjiang real estate was booming as the government invested heavily to develop the historically neglected region. With Tongfang, Zhao formed a joint-venture that eventually became known as Beijing Jiankun Real Estate.

The timing, Zhao has acknowledged, was impeccable. “Entering the real estate market at that time was like grabbing money,” he told a Taiwanese magazine in 2015.

Although Zhao had not grown up with particularly impressive family connections or networks, his success at Tsinghua University and its affiliated companies started to give him exposure and access to Beijing’s most elite circles. For example, he became friendly with Hu Haifeng, the son of then-president Hu Jintao, who was Party boss of Tsinghua Holdings. And according to Matthew Forney, president of Gavekal Fathom China, a Hong Kong-based consultancy, Zhao also impressed Chen Xi, a Politburo member, Tsinghua University’s party chief until 2008 and a close confidant of President Xi. During a 2010 ceremony at Tsinghua University in which Zhao donated 100 million RMB to the institution, Chen was in attendance.

“Zhao’s opportunity to run so many businesses for Tsinghua University hinged on Chen’s support,” says Forney, adding that their relationship is “common knowledge in Chinese IT circles.”

Soon after being named CEO of Unigroup, in 2009, Zhao’s property development company acquired a 49 percent stake in the company for $21 million, blurring the line between the state-backed conglomerate and Zhao’s own profit-seeking. No one seemed to mind.

“He made a crap-ton of money for the university and they looked the other way on the fact that he managed 49 percent for himself, because that was part of the deal,” says the semiconductor industry insider.

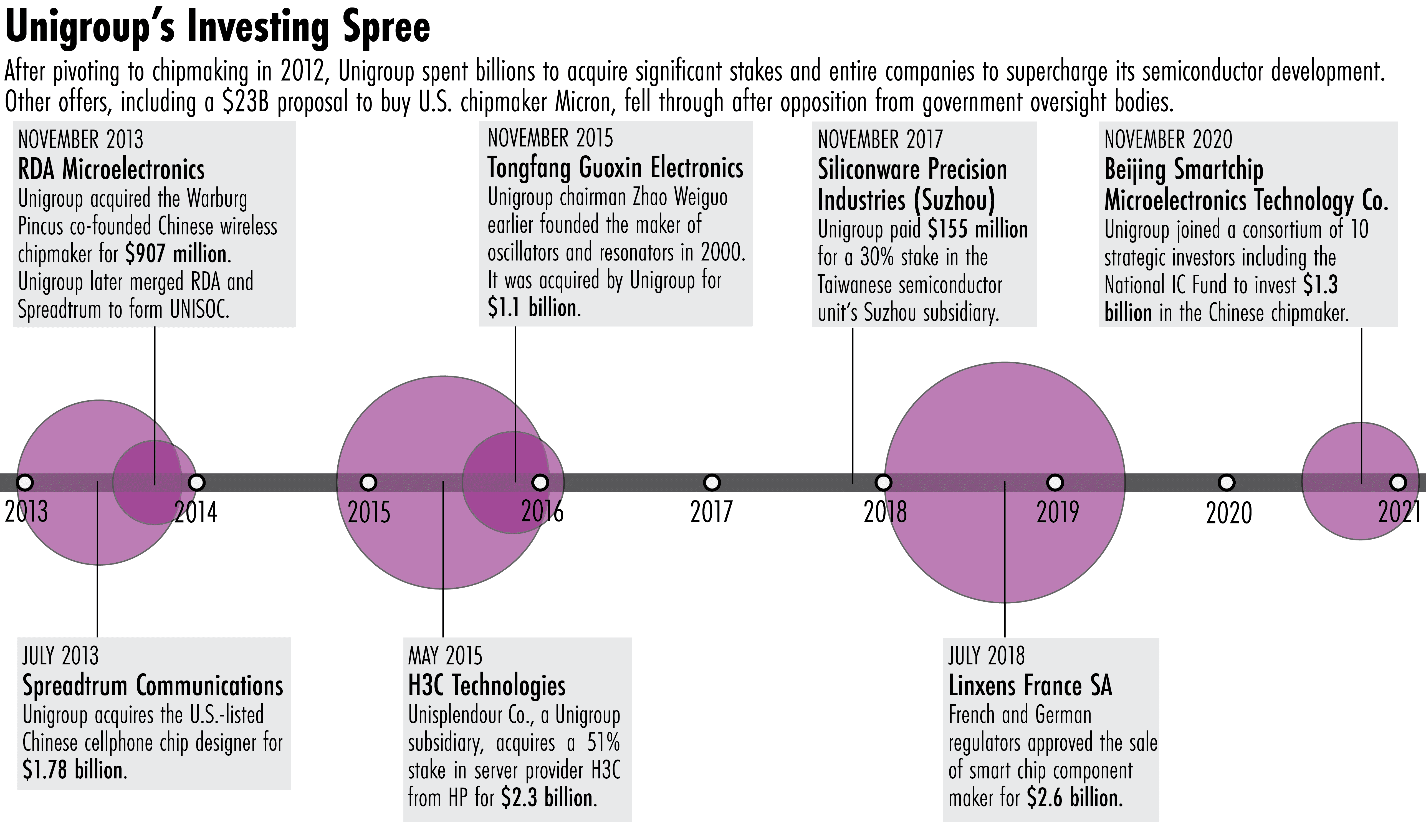

Under Zhao’s leadership, Unigroup spent hundreds of billions of dollars on acquiring integrated circuit (IC) firms at home and abroad — most notably Linxens, a chip components maker in France — and building ‘fabs’ (or semiconductor manufacturing facilities) in China. In 2013, Unigroup unloaded $2.7 billion to acquire private Spreadtrum Communications and RDA Microelectronics, two U.S.-listed Chinese chipmakers, before merging them to form UNISOC, which is now one of China’s largest mobile phone chip designers. Unigroup also signed partnerships with major Western tech companies, including Intel, and it took a stake in H3C, HP’s Chinese server and storage business, for $3 billion. (This month, corporate filings revealed that HP has left the joint-venture, leaving Unigroup with 100 percent ownership of H3C.)

In an industry where talent is critical, Zhao also proved himself as a notorious poacher. In one particularly painful grab for Taiwan, he convinced Charles Kao, Taiwan’s “Godfather of DRAM”, to join Unigroup in 2015, likely with a stupendous salary increase. He also managed to acquire a 25 percent stake in Taiwan’s Powertech Technology, which tests and assembles ICs.

Luck and gusto had propelled the former goat herder to unimaginable heights: that year, Unigroup reached an all-time high market cap of $7.6 billion. But turbulence soon followed as his buying sprees — especially those beyond China — came to be seen as presumptuous and even dangerous.

During a 2015 visit to Taiwan, Zhao attempted to purchase a stake in TSMC, the largest IC manufacturer in the world and Taiwan’s crown-jewel. He was, unsurprisingly, rebuffed. To his offer, founder Morris Chang reportedly replied, “I’m afraid you can’t afford it.”

This was the first of several embarrassing failures. Also that year, Unigroup revoked its $23 billion bid to buy Micron Technology, America’s largest memory chip company, after Congress pressed the Committee on Foreign Investment in the United States (CFIUS) to review “the national security implications of allowing China to gain market control over the production of components tied to modern U.S. defense systems.” It would have been the largest Chinese takeover ever of an American company.

Unigroup also proposed merging Spreadtrum and R.D.A. with MediaTek, a Taiwanese chip designer and national champion. The Taiwanese government, which carefully monitors Chinese investment into its IC industry, would have had to provide an exception for the merger to go through. It declined to do so.

Then, in 2016, Unigroup terminated a $3.8 billion plan to become the largest shareholder in Western Digital, a California data storage firm, after CFIUS flagged it for review.

The White House is sending a signal that it will do everything in its power to curtail China’s technological development. The tech war between the U.S. and China has gone from warm to hot.

Noah Barkin, Rhodium Group

Such national security concerns annoyed Zhao, who often brushed aside suggestions he was anything but a profit-driven businessman. “Mergers between big U.S. and Chinese companies are bound to happen,” he said, according to Miller’s Chip War. “They should be viewed from a business perspective instead of being treated under nationalist or political context.”

To industry insiders, such public failures outed Zhao as “an amateur,” said one Chinese academic expert who requested anonymity to discuss sensitive topics. “Anyone who knows the history of the industry even a little bit would know there was no way he would have been able to buy these companies.”

At home, however, Unigroup had smoother sailing. The company’s two stars, UNISOC and YMTC, grew considerably in the following years, and publicly, the state continued to smile upon Zhao. In 2017, Unigroup announced a new “investment” into the firm: some $15 billion from China Development Bank and $7 billion from the Integrated Circuit Industry Investment Fund.

But despite the patronage, by 2020, Unigroup was drowning in debt from Zhao’s spending. In July 2021, after Unigroup defaulted on several international bonds worth nearly $2.5 billion, the government, which would not allow such a prestigious semiconductor player to fail, ordered Unigroup to overhaul its $30 billion of debt.

Sharks started circling. JAC Capital, a state-backed IC investment fund run by Li Bin, an enigmatic financier with ties to Party elite, offered to rescue Unigroup with a $9 billion buy-out bid. But Zhao was offended by what he perceived as a low-ball offer. “The proposed deal is an intent to commit a crime,” Zhao griped. “Even if the creditors’ committee approves the deal, I will fight a legal battle until the end.”

Thus began an ugly and protracted public battle, in which both JAC Capital and Zhao filed lawsuits and corruption allegations against one another to the CCDI. But Zhao, some say, never really stood a chance.

“It was basically a battle between somebody who wanted to be a princeling but never was and a real princeling,” says the industry insider. “Guess who’s going to win in that fight?”

In April, JAC completed its purchase of Unigroup. Three months later, Zhao was in handcuffs.

NODE SURRENDER

Unigroup, which has since undergone “restructuring,” will remain a major player in China’s politically-charged chip sector. But the fall of Zhao and other chip giants suggests a reevaluation — some even say an abandonment — of Beijing’s silicon dreams.

Since the Trump administration, the U.S. and its allies have restricted key technologies and know-how from reaching Chinese chip firms, severely limiting China’s ability to keep pace with industry innovations. In October, the Biden administration introduced even tougher restrictions, including placing YMTC on the Entity List, which has dramatically upended China’s semiconductor grand strategy.

“The White House is sending a signal that it will do everything in its power to curtail China’s technological development,” says Noah Barkin of Rhodium Group. “The tech war between the U.S. and China has gone from warm to hot.”

Moreover, America and Europe are now investing heavily in their own IC industries, in large part because of anxiety over a Chinese invasion of Taiwan, which produces 90 percent of the world’s advanced semiconductors.

“Would we be so anxious about [semiconductors] if there was no risk that Xi Jinping would invade Taiwan?” asks Willy Shih, a professor at Harvard Business School and member of an IC advisory committee for the Department of Commerce. “It’d be a very different picture. Before 2012, this never came up.”

Now that it has though, the U.S. is taking significant action. In August, Washington adopted the $280 billion CHIPS and Science Act, which will provide $52 billion in subsidies and R&D investment for chip firms operating in the United States. Intel and TSMC are investing stateside as a result. The European Union proposed similar legislation last year with a $49 billion price tag, hoping to double its global market share to 20 percent by 2030.

The Taiwanese public, polls show, are increasingly wary of the PRC as well — and its prized semiconductor industry is becoming more defensive as a result. Chinese chip firms have long been a regular presence in Taiwan, luring talent and, crucially, I.P. to mainland firms with salaries up to five-times higher than in Taiwan.

But that, like so much in the global semiconductor ecosystem, is changing. A more bellicose and Covid-closed China lessened the country’s attraction for Taiwan’s IC workforce. The Taiwanese government, too, has made it harder for Chinese firms to attract talent, banning unregistered Chinese headhunters from operating on the island. The overall result has been less poaching and more suspicion.

Would we be so anxious about [semiconductors] if there was no risk that Xi Jinping would invade Taiwan? It’d be a very different picture. Before 2012, this never came up.

Willy Shih, a Harvard Business School professor

“Workers used to look at it as a good opportunity [to go to China],” says Daniel Nystedt, a Taipei-based IC analyst with TriOrient Investments. “But with China firing missiles over Taiwan this summer and all the intimidation that’s been going on, there’s definitely been a change.”

So how will companies like Unigroup proceed after the dust settles? One option is to abandon advanced chips and settle for the older technologies, a strategy which the greater Chinese chip industry seems to be shifting towards.

“In the past few years, the more we tried to make up for our deficiencies, the more passive we have become,” said Wei Shaojun, an official at the China Semiconductor Industry Association, in a December live-streamed speech. “We should focus not on overcoming weaknesses, but on enhancing our strengths.”

On the flip side, China could attempt more semiconductor “moonshots” — technology advances that don’t present much prospect for profit but that are strategically important. Ultraviolet lithography machines, for example, are a vital technology that China is currently restricted from accessing by U.S. sanctions. Although the hurdles remain high, some analysts and insiders are not willing to rule out such advances. Scott Moore, a Chinese tech expert at the University of Pennsylvania likens the situation to nuclear weapons and the failures of non-proliferation.

“What technology is more tightly controlled than nuclear weapons?” he says. “But that has not stopped many countries that have said, ‘We’re willing to make any investment of resources into acquiring this technology.’”

Indeed, with Zhao out of the picture, Unigroup now seems to be adopting such a militant and determined approach. The new chairman is Li Bin, the “princeling” from the state-backed JAC Capital. In a letter to staff, publicized in July, Bin denounced Zhao’s erratic leadership and “uneven” business successes, promising “a new start.” Unigroup, he added, is ready to “go into battle.”

Brent Crane is a journalist based in San Diego. His work has been featured in The New Yorker, The New York Times, The Economist and elsewhere. @bcamcrane