In April 1999, Chinese Premier Zhu Rongji made a visit to Washington, D.C., to meet with President Bill Clinton. A few days earlier, the American president had delivered a speech voicing strong support for China’s admission into the World Trade Organization, a long held priority for Beijing. While acknowledging the Chinese Communist Party’s human rights abuses and other problems, Clinton stressed the hope that economic development would liberalize China.

“Is this a country to be engaged or isolated? Is this a country beyond our power to influence or a country that is ours to gain and ours to lose?” the president asked. Zhu was there to be gained.

At a White House dinner, Clinton introduced the Chinese premier to some of the 224 dignitaries in attendance: novelist Amy Tan, the Rev. Billy Graham, cellist Yo-Yo Ma and Janet Yellen. At the center of each table, bamboo containers held roses, tulips and orchids. Corporate America was well-represented, with chief executives from Kodak, Motorola, Boeing and more. All were eager to chisel inroads into China’s nearly-open market of one billion consumers.

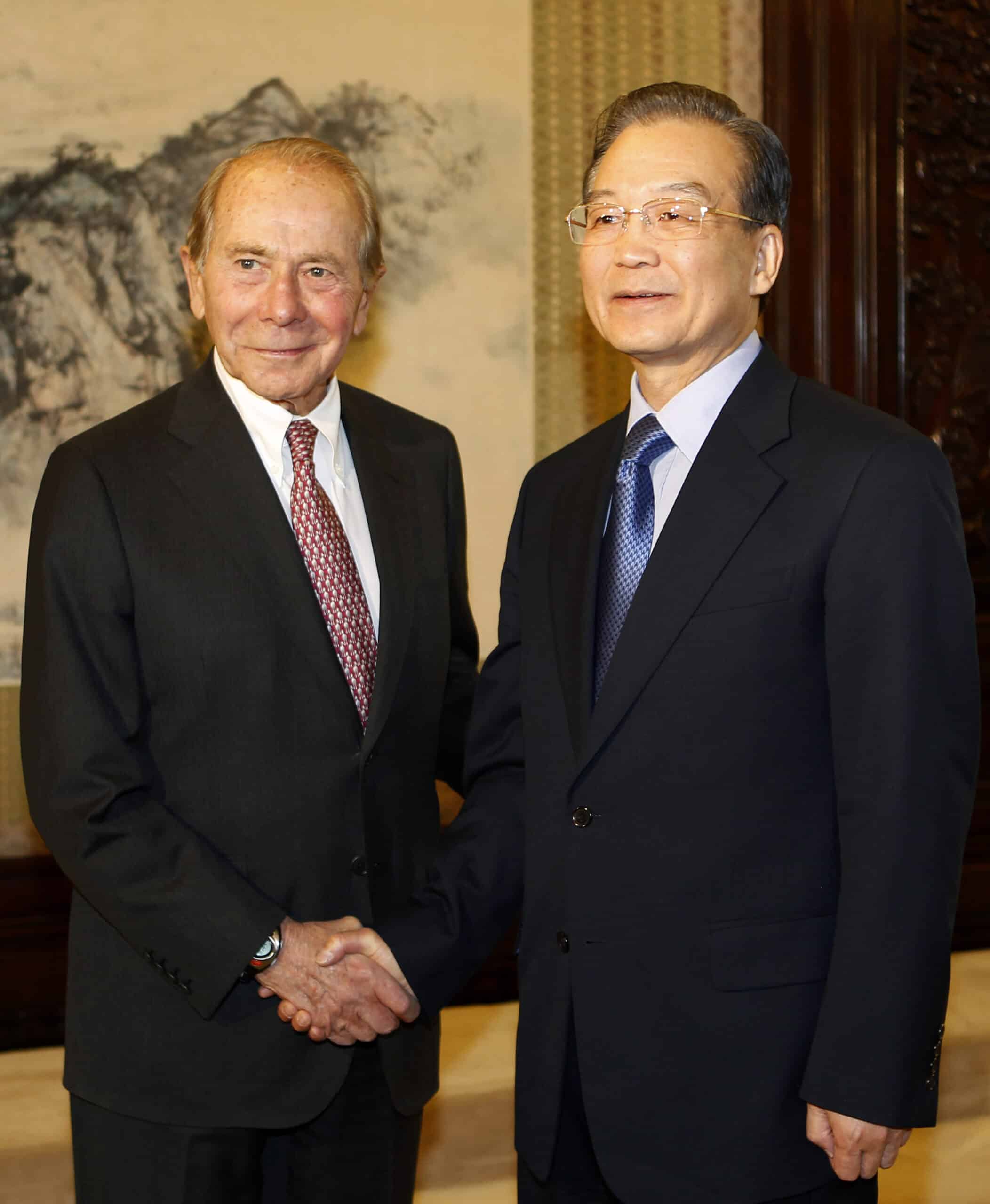

In a receiving line, Clinton introduced Premier Zhu to Maurice R. Greenberg, a dwarfish insurance mogul from Manhattan. The premier chuckled. “I know Hank,” he beamed, using the CEO’s nickname. The billionaire and the apparatchik came together in a warm embrace, and The Washington Post noted that, out of all the American powerbrokers in the room, Greenberg was “the guest Zhu seemed most pleased to see.”

Two years later, China was admitted into the W.T.O., turbocharging its remarkable economic ascent. Many in corporate America had lobbied on Beijing’s behalf, but Greenberg was, in many insiders’ accounts, particularly influential. Indeed, now at age 97, Maurice Greenberg has advocated for deeper U.S. engagement with the People’s Republic of China for longer than perhaps any living American businessman, earning him the reputation of a private sector statesman.

Hank has always been held in great appreciation in China for the contribution he made to its development.

Robert Lawrence Kuhn, an American investment banker and China Reform Friendship awardee

“Just like Kissinger was a businessman masquerading as a diplomat in China, Greenberg was a diplomat masquerading as a businessman,” says Isaac Stone Fish, author of America Second: How America’s Elites Are Making China Stronger.

Greenberg made his name with American International Group, or AIG. From 1967, when he became chief executive, to 2005, when he resigned following a fraud investigation, the company’s market value swelled from $300 million to $180 billion. Under him, AIG became the largest insurance company in the world. It was, he often boasts, “a national asset.” Through spearheading insurance access across the world, from Mumbai to Moscow, AIG paved the way for American companies to do business abroad, often with the help and blessings of the U.S. government.

“We didn’t hesitate to use the U.S. government to support our desire to open markets around the world,” Greenberg reflected in 2011.

Much of his influence extended from his large donations to some of Washington’s most important think tanks and policy institutions: the Council on Foreign Relations (CFR), where he served as vice chairman; the Nixon Center, where he served as president; and the Asia Society, where he served as chairman. He has also enriched the Atlantic Council, Yale University, the Heritage Foundation and the Brookings Institution, among others.

For Beijing, figures like Greenberg are a kind of national asset, too. In 2018, he was awarded the China Reform Friendship Award medal by President Xi Jinping for having played “a key role in helping China open up to the world,” one of only two Americans to receive it.1Greenberg has also been christened an “honorary citizen” of at least five Chinese cities. He is a member of the advisory board at the Tsinghua School of Economics and Management, a member of the International Advisory Council of the China Development Research Foundation and a member of the China Development Bank. From 1998 to 2005, Greenberg served on the Hong Kong Chief Executive’s Council of International Advisers.

“Hank has always been held in great appreciation in China for the contribution he made to its development,” says Robert Lawrence Kuhn, an American investment banker close to Chinese leadership and also the other American recipient of the China Reform Friendship medal.

“There’s no American business person who has stood up stronger for constructive U.S.-China relations, who fundamentally believes that trade and investment between the United States and China is good for the American people,” says Stephen A. Orlins, president of the National Committee on U.S. China Relations. “He believes going down this path of confrontation is wrong.”

Greenberg certainly possesses a passionate devotion to China, which he has visited nearly every year since 1975, often multiple times. And he has long contended that “a world where the U.S. and China are allies is a very safe world.” Over the years, he has also discouraged haranguing Beijing about human rights and other sensitive issues.

“It is unlikely that China’s political system will ever mirror ours,” he argued in 2005. “China’s political system will reflect its own history and culture, and while it may change over time, we should not expect that our model is the only acceptable political system.”

Given how China’s system has changed over time — becoming more authoritarian and less open since Xi Jinping came to power — Greenberg’s views seem emblematic of a long-ago moment in time, when engagement with China was widely celebrated at places like White House dinners. But while America’s approach to China has changed considerably in the years since, Greenberg’s has not.

In July, he wrote an op-ed in The Wall Street Journal arguing that through trade and investment, western industry in China can help “re-establish a constructive bilateral dialogue based on mutual respect and understanding.”

“It is in our national interest, now more than ever, to do all we can to improve U.S.-China relations,” he wrote. “I understand that opposing worldviews make attempts to establish a constructive dialogue difficult, but given what is at stake, it only makes sense to try.”

A list of 13 business and policy leaders signed on to the essay, including Orlins, Max Baucus, the former U.S. ambassador to China, and William S. Cohen, the former U.S. defense secretary. But such sentiment seemingly grows rarer by the day.

To Joerg Wuttke, president of the E.U. Chamber of Commerce in China, Greenberg’s position that entrenching business ties between America and China will inexorably lead to stable relations “sounds a bit like a slogan from the nineties.”2See Wuttke’s lengthy Q&A here in The Wire from two weeks ago.

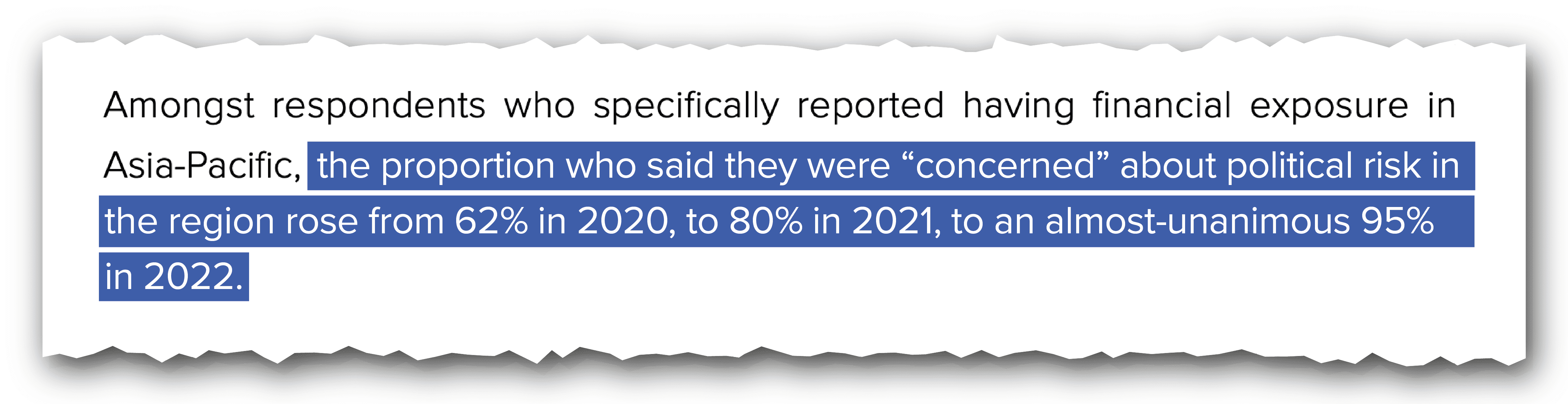

Indeed, once reliable cheerleaders for engagement, many American businesses seem to be, at best, quiet on the subject of China and, at worst, souring on an increasingly erratic and combative Chinese Communist Party (CCP). A 2022 political-risk survey by the insurance broker Willis Tower Watson found that 95 percent of firms surveyed were now worried about the risk of operating in China, up from 62 percent in 2020. China’s dismal demographics, overextended banking sector and chaotic “Covid-zero” policy even have some whispering the word “uninvestable.” Others argue that China is simply not as appealing as it once was: in the second quarter of 2022, China’s GDP growth was a mere 0.4 percent, its lowest rate in decades. As one economist put it in The Wire recently, “China’s economic ‘miracle’ seems to be well past its peak.”

But despite the negative news about China, momentum may be brewing to update Greenberg’s China slogan for the current moment. Leading the charge is none other than Greenberg’s own son, Evan, who is chief executive of the New York Stock Exchange listed insurer Chubb Ltd. In recent months, Evan G. Greenberg has given speeches and published essays that reframe U.S. business engagement with China as a patriotic endeavor — something that strengthens the U.S. — while also insisting that the American business community ought to be more present and vocal when it comes to deciding America’s China policy — the way it was when his father was at his peak.

Both Greenbergs have financial incentives in China, of course: Hank’s current firm, Starr Insurance Companies, has considerable insurance deals in the country, including with projects associated with the Belt and Road Initiative, Xi Jinping’s sprawling global infrastructure project. And at Chubb, Evan has doubled down on investments in China, including a large stake in Huatai Insurance.

Neither men responded to repeated requests for comment, but as public opinion on China sours, the Greenbergs are presenting themselves as something of a “silent majority,” as one analyst puts it, in the American business community — saying what other business leaders believe but are too afraid to say. That is, that despite its risks and political blemishes, China’s market remains too large to ignore.

A country with 1.3 billion people could not be left out of the world’s trading system and be isolated. It was only a matter of when, not if.

Hank Greenberg reflecting in 2016 about China’s opening

China’s inbound foreign direct investment, after all, actually rose in 2021 by a third to $334 billion — an all-time high. One could argue that such stats suggest there is a new generation of CEOs who are, contrary to popular opinion, just as committed to doing business with China as Hank Greenberg has always been.

100% FOREIGN OWNED

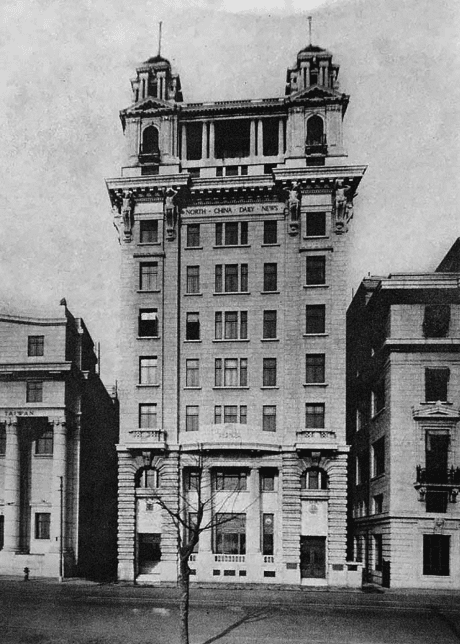

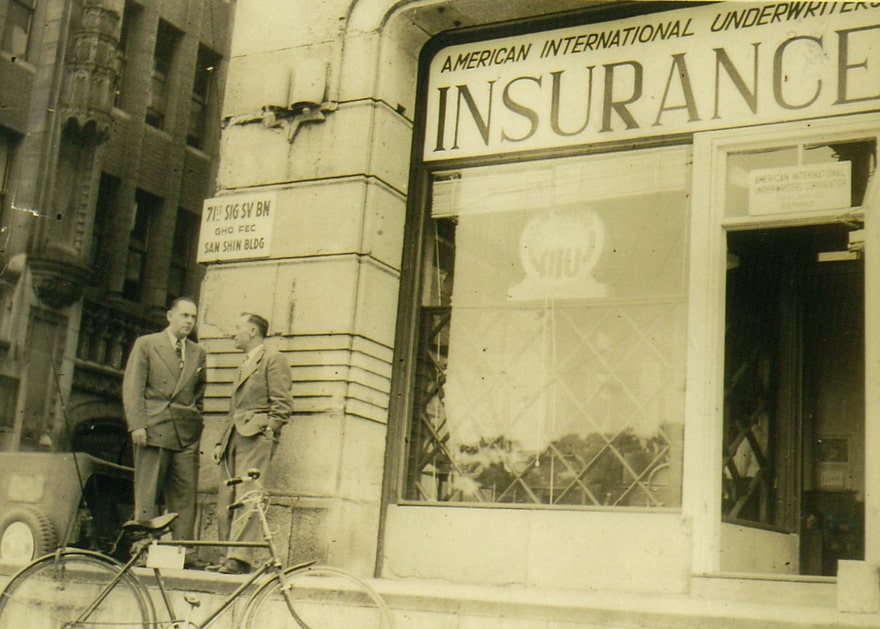

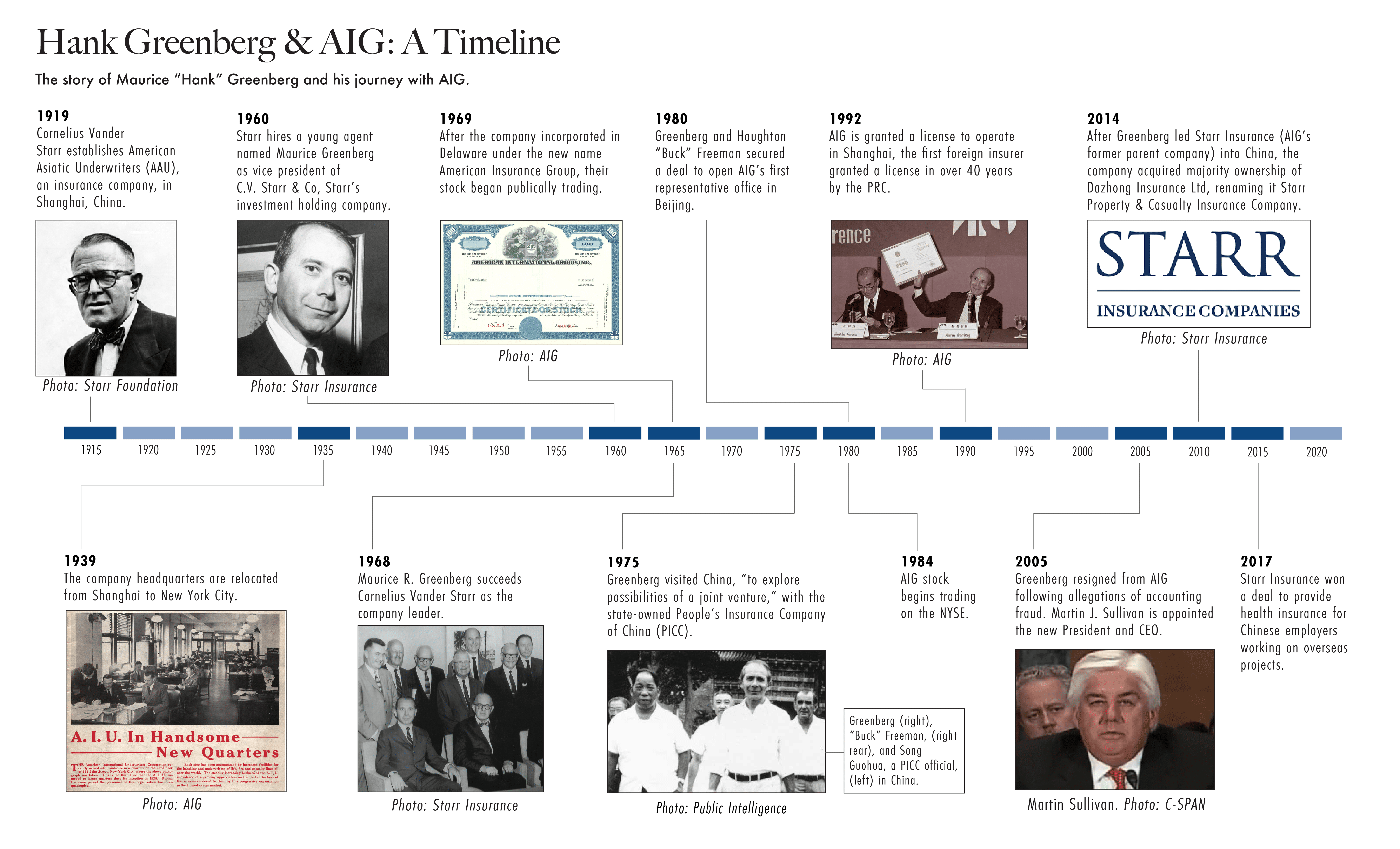

On December 19, 1919, a 27-year-old Californian named Cornelius Vander Starr opened an insurance agency in Shanghai called American Asiatic Underwriters (AAU). The company prospered, and in a few years Starr had opened branches throughout East Asia as well as in the United States. AAU’s headquarters remained in Shanghai, where Starr amassed real estate holdings and purchased two newspapers and a magazine.

The company was located in the regal No. 17 North-China Building on The Bund. Starr, who resided on the eighth floor, became one of Shanghai’s most important powerbrokers. “His is a machine-gun mind, tactful at times, but often tough,” described a 1935 Fortune profile. “His operations form a vast and intricate web, the outer limits of which no one knows.”

In 1939, after Japanese forces invaded and occupied the city, assassinating the editor of the Chinese edition of Starr’s Post and Mercury newspaper, Starr relocated to New York. When the war ended, he returned. But it was a short-lived reunion. Following the communist victory in 1949, Starr again had to flee for Manhattan.

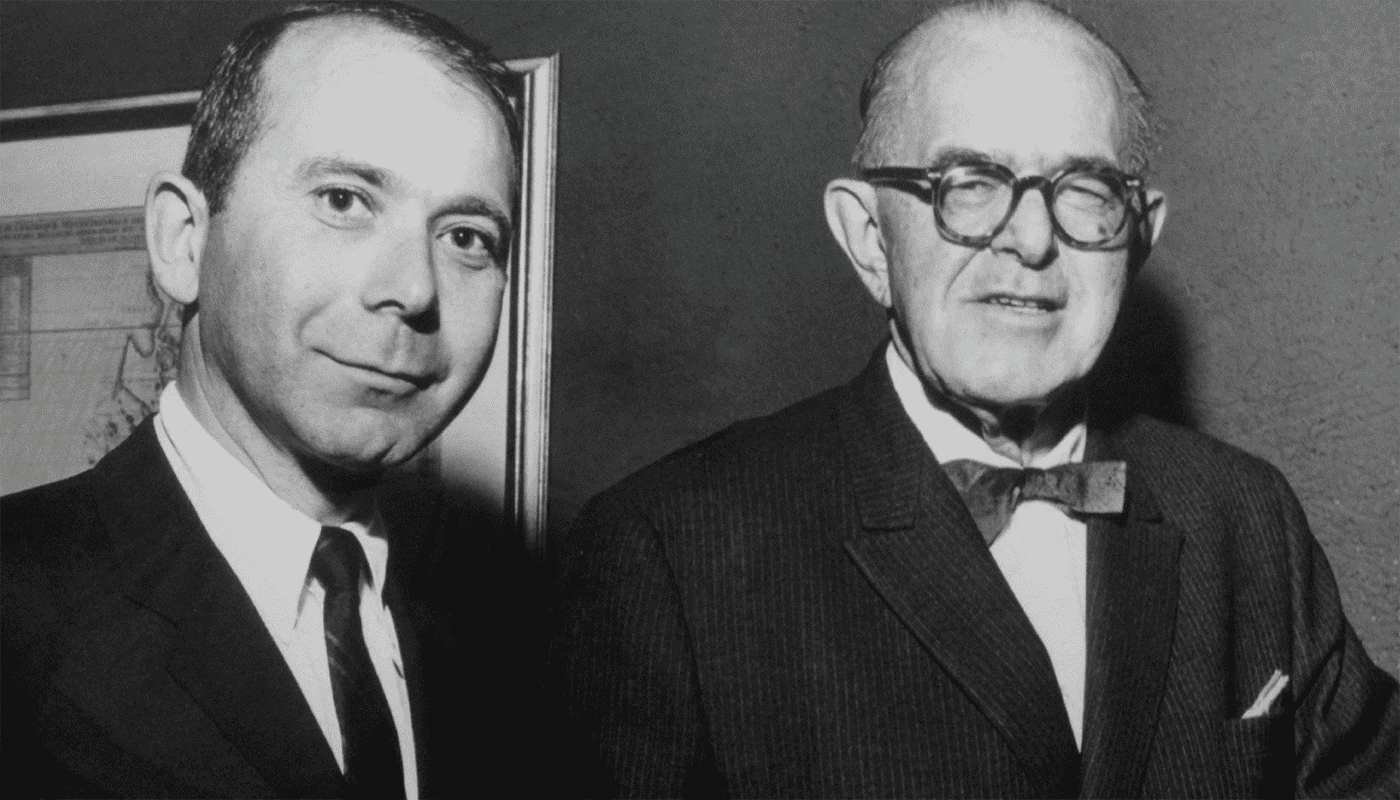

In 1960, Starr hired a promising young agent named Maurice Greenberg as vice president of C.V. Starr & Co, Starr’s investment holding company. The enterprising New Yorker, who grew up on a dairy farm, had fought in Europe during World War II and then in Korea as an Army captain. Intensely driven, he went by Hank, after the Depression-era baseball star, “Hammerin’ Hank” Greenberg.

Starr took an immediate liking to the bombastic young man, who he saw as the son he always wanted, according to Ron Shelp’s Fallen Giant: The Amazing Story of Hank Greenberg and the History of AIG. Just eight years later, when Starr retired, he made Greenberg president. In 1969, the company went public under the name American Insurance Group, a change intended to invoke a “strong U.S. identity,” Greenberg writes in his co-authored memoir, The AIG Story.

Greenberg transformed Starr’s company, streamlining operations, cutting costs and boosting profitability. He relished being boss. “To say that Greenberg ruled AIG understates the measure of control he kept over the company,” writes Shelp. “He was an archetypal autocrat.” He stressed “the three 15s”: 15 percent revenue growth, 15 percent profit growth and 15 percent return on equity.

Underlings were as mesmerized as they were fearful of Greenberg, who they referred to by his initials, M.R.G.

“He had a monumental memory, and he knew the answer to a lot of the questions he asked, but he wanted to see how you responded,” recalls a regional manager for AIG Hong Kong in the 1980s and 1990s who requested anonymity because he signed a non-disclosure agreement. “He could be engaging and solicitous, but could turn on a dime and brutally eviscerate an under performer.”

AIG operated in 137 countries but “China was his baby. He valued the opportunity China presented very much,” says the employee.

Part of that attraction stemmed from AIG’s history. China, notes Shelp, played an “almost mythological role within the culture of the company” because of its origins there. But Greenberg also harbored a “conviction that China will be a huge economic power where AIG can make a ton of money.”

“A country with 1.3 billion people could not be left out of the world’s trading system and be isolated,” Greenberg reflected in 2016 about China’s opening. “It was only a matter of when, not if.”

Greenberg first visited China in 1975, after requesting an invitation from the state-owned People’s Insurance Company of China (PICC) “to explore possibilities of a joint venture.” At the time, he told Shelp, who worked closely with Greenberg, “I want us to be invited back. And I expect us to be the first invited back.”

In a November trip that year, a reinsurance deal — basically an insurer insuring another insurer — was signed between the two firms. In 1980, Greenberg and his sidekick on China matters, Houghton “Buck” Freeman,3Freeman himself was born in Beijing and is fluent in Mandarin. His father, Mansfield Freeman, taught at Tsinghua University before being recruited by Starr to help found AIU. https://china.usc.edu/memoriam-houghton-buck-freeman-1921-2010 secured a deal to open AIG’s first representative office, in Beijing. PICC and AIG also soon formed a joint-venture, the China America Insurance Company, which targeted companies involved in China-U.S. trade.

But that wasn’t enough and for many years after, Greenberg lobbied Shanghai Mayor Zhu Rongji (who was the Premier at the Clinton White House dinner) and Premier Li Peng for full ownership of AIG’s China operations. While Beijing’s efforts to soften up American business executives is often described as “love bombing,” Greenberg was just as adept at playing the game. In the early 1990s, he purchased a pair of antique Chinese bronze window panels from a Paris gallery, returning them to China in a solemn ceremony broadcast on Chinese television.

“The Chinese are very grateful,” he said. “It’s the first time that somebody gave something back to the Chinese that was taken away. So I’m proud to do that.”

His charitable Starr Foundation also made a number of philanthropic donations to China, such as children’s hospitals. And Greenberg assured Zhu he would use some of AIG’s China revenues to invest in local projects if they were given full ownership.

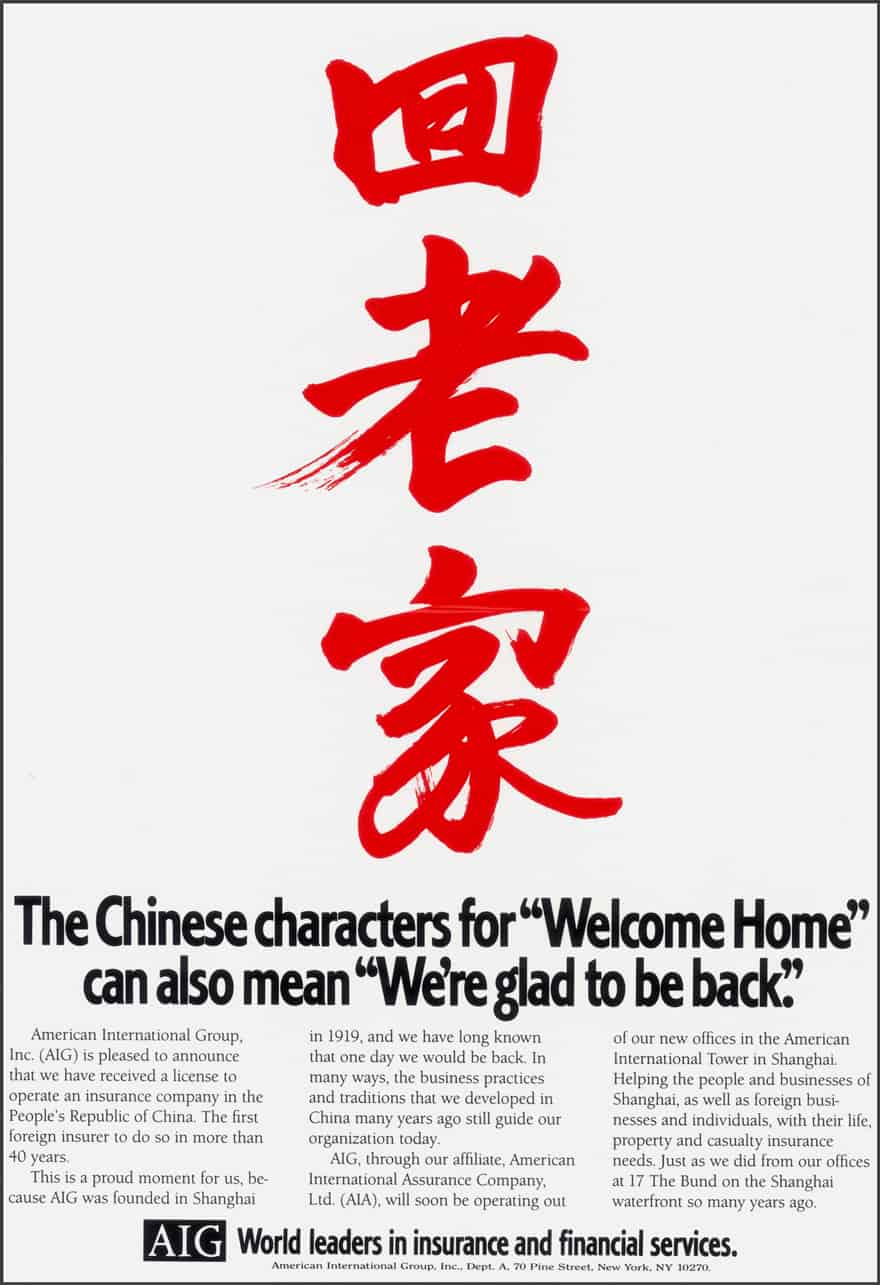

In 1992, Greenberg’s wish was granted. Although China in the late 20th century was generally reluctant to allow foreign firms into the country, the insurance industry, which was virtually undeveloped there, was an exception. It was viewed as a relatively benign form of foreign capital.

“Insurance is just a series of bets that something bad won’t happen,” says Fraser Howie, co-author of Red Capitalism: The Fragile Financial Foundations of China’s Extraordinary Rise. “It fit into government plans neater than some other aspects of financial markets, such as securities trading.”

China’s willingness to accede to Greenberg, he wrote to President George H. W. Bush, was “further evidence of the reform movement gaining strength and opening more of the economy to the outside world.”

For decades after, AIG remained the only “100% foreign-owned” insurance operation in China, as Greenberg often boasts. (In 1994, Chubb Insurance Ltd., which Evan Greeberg would come to run, opened its first office in China in a joint-venture.)

Around 50 foreign insurance firms eventually set up in China — including Germany’s Allianz, France’s AXA and Britain’s Prudential — but AIG was the first. It even returned to Starr’s building on the Bund in a 1992 ceremony that Greenberg described as “emotional.”

Yet it is unclear if AIG’s early forays offered any long-term advantages.

“It took years before we made money in China,” says the Hong Kong employee. And it was an open secret that the company was “opening up its intellectual capital [to China],” the employee added. “How we marketed our business, how we trained our agents, what our policy terms and conditions were, how we handled claims — the whole spectrum of how an insurance company does things.”

AIG, notes Nicholas T. Omondi, an analyst with Z-Ben Advisors, an analytics firm in Shanghai, “created the template for what the industry [in China] now is.”

And the insurance industry in China is now booming. Although China’s insurance market is not as developed as the American or European ones in terms of products offered, it is the world’s third largest — worth about $318 billion in premiums — after the U.S. and Japan. The consultancy Oliver Wyman forecasts China will become the world’s largest life insurance market by 2030.

Out of the ten largest life and non-life insurance firms operating there, all are Chinese-owned. And, according to Deloitte, no single foreign insurer accounts for greater than 2 percent of China’s insurance market.

Indeed, while AIG made modest profits through the nineties and early 2000s in China, the company doesn’t seem to have reached the full potential Greenberg hoped for. AIG’s Asian regional spin-off, the Hong Kong-based firm AIA, has done well — it remains the only wholly-owned foreign life insurer in China — but it split from AIG in 2012 with a $6.45 billion sale. AIG’s relationship with PICC outlived Greenberg’s leadership, but in 2019, AIG sold its entire stake in the firm for $482 million, gaining a mere $8.6 million profit, according to calculations by Bloomberg.

That’s not to say there isn’t money to be made for Western insurance firms in China. After being forced to resign from AIG in 2005 following allegations of accounting fraud made by New York attorney general Eliot Spitzer4Greenberg eventually paid a $9.9 million settlement, in 2016, after a nearly 12-year court battle., Greenberg led Starr Insurance Companies, AIG’s former parent company, into China. In 2014, the company acquired majority ownership of the Shanghai-based Dazhong Insurance Company Ltd., which was renamed Starr Property & Casualty Insurance (China) Company. The transaction value was not disclosed, but it was the first privatization of a state-owned insurance company ever and “a homecoming for Starr,” the firm said.

“It was [Shanghai Mayor Han Zheng’s]5Han Zheng is now a vice premier and member of the powerful Politburo Standing Committee. idea that Starr should invest in Dazhong,” Greenberg said at the signing ceremony. In 2017, the firm won a deal to to provide health insurance for Chinese employees working overseas on Belt and Road projects.

For foreign insurance firms, the Belt and Road Initiative, which launched in 2013 and spans 130 countries, has been a major source of profits. Given the particular complexity of infrastructure insurance, BRI projects — which include railways, ports, highways and more — are attractive for more experienced foreign insurance firms. By 2030, BRI could generate $27 billion in premiums for the international insurance industry, notes a Swiss Re report.

Starr Insurance Companies, Greenberg said in 2019, counts China as “one of our most important markets.”

But Greenberg’s “pandering” to Chinese officialdom, as some deem it, has gone beyond mere business interests. He has written several op-eds — in the National Interest, the The Wall Street Journal and elsewhere — that criticize American policy towards China while downplaying Beijing’s own problems. At times, he has reportedly used his influence at places like CSIS and the Heritage Foundation to blunt thinkers seen as too hawkish on China.

While few would expect him to publicly excoriate China given his history there, Wuttke notes a line is crossed when someone starts “dancing and singing songs to the praise of the party.”

“This kind of vocal support of the political system is really not necessary,” he says.

A 2019 exchange during a CFR Distinguished Series event exemplifies Greenberg’s tight-lipped posturing. The host asked Greenberg how he felt about China’s increasing authoritarianism under President Xi, who has aggressively policed dissent, ramped up surveillance and censorship and is orchestrating a campaign of wanton internment and cultural genocide against the Muslim Uyghur minority in Xinjiang.

“It doesn’t bother me,” he replied. “We have pretty good relationships. We have access to see the people. We candidly tell them they’re doing something that we think is harmful to us, or the economy overall. We talk about it.”

The host pressed. “So it doesn’t bother you?”

“No,” he repeated.

ASSET RISK

Greenberg’s son Evan doesn’t hesitate to gently chide the CCP, but he also has some admonishments for the United States. In June, for instance, as he took the stage at the Center for Strategic and International Studies (CSIS), where his father is a trustee, he warned the audience that they better get comfortable.

“I hope you all took advantage, went to the restroom before this,” he said. “You’re going to be here for a while. Not too long. But I do have a lot to say today, and I think it’s on a serious subject. And it needs to be said, because we need to have a fulsome debate.”

Evan, 67, is known by senior China officials as “Greenberg Junior.” If he lacks the charm and wit of his father, as many say, he does not lack the drive and business acumen. Chubb Ltd. — he joined its predecessor, ACE Ltd., in 2001 — is worth $80 billion, double AIG’s current value. Evan worked at AIG for 25 years, but according to Hank, he did not get special treatment. Of him and his brother, Jeffrey, who also worked at AIG, Hank told the WSJ that he “expected more from them than anyone else.”

Prior to Evan’s CSIS talk, Zurich-based Chubb — the world’s largest property and casualty insurer, with $200 billion in assets — had recently increased its majority stake in Huatai Insurance Group to 86.1 percent. The firm had gradually been increasing its ownership of the Chinese insurer, which boasts 191 million customers and over 600 branches, including with a $1.5 billion share buyout in 2019; in its first nine months, the stake garnered Chubb a profit of $161 million.

But Evan assured the audience at CSIS that such financial incentives didn’t impact his desire to “elevate the public debate on China.”

Currently, U.S. China policy is pretty much dictated by domestic politics… It’s to the point where there’s very little public space to talk constructively about China, if any.

Max Baucus, the American ambassador to China under Obama and a signatory of Greenberg’s July op-ed

Acknowledging the common accusation that “American companies operating in China are unpatriotic, or at best, gullible and naive,” he went on to argue that U.S. business engagement with China is as patriotic as it gets. The U.S., he said, “must recommit to an interest-based approach to our economic relationship with China. I believe deeply that America is strengthened by having its companies compete and thrive in the global marketplace, and in China.”

Concerns of human rights abuses, authoritarianism and morality, he said, while valid, were beside the point: “It is hardly my image for humanity,” he said. “But it is also not my decision. China is a sovereign country.”

In the aftermath of the speech, Orlins, from the National Committee on U.S. China Relations, said Evan, who serves as vice chair of the National Committee, had emerged as “the voice of the business community on why business and trade are in America’s national interest.”6Evan Greenberg is also the former chairman of the U.S.-China Business Council, a lobbying group for more than 200 American companies doing business in China.

But it’s unclear if Evan’s desire to reclaim the Greenberg mantle of promoting U.S. business interests in China can hold sway like it used to.

“It used to be the case that American business was the ballast that would straighten out the U.S.-China relationship when things got bad,” says Kuhn. “Now, in both countries, you have a lot of pressure from the masses in being anti the other country.”

Indeed, much of the current discomfort with China is bubbling up from society at large, where there is a growing, if vague, suspicion of Chinese intentions in the world.

“Currently, U.S. China policy is pretty much dictated by domestic politics,” says Max Baucus, the American ambassador to China under Obama and a signatory of Greenberg’s July op-ed. “Members of the House and Senate — Republican and Democrat — help their reelection efforts by criticizing China. It’s bipartisan. It’s to the point where there’s very little public space to talk constructively about China, if any.”

If you want to induce the Americans to stop resisting China, you go to people like [Hank] and he’ll write obedient op-eds that say, ‘Don’t resist China.’

Edward Luttwak, geopolitical consultant and author of The Rise of China vs. the Logic of Strategy

But if the American zeitgeist is indeed turning away from China, American corporations may not yet be ready to. Part of the reason is that Beijing is finally making it easier, at least on paper, to operate there in some sectors, opening up new areas to foreign firms and cutting some joint-venture requirements. In a 2021 survey of 300 American companies from the American Chamber of Commerce in Shanghai, 60 percent reported increased investment compared to 2020. Unlike the Greenbergs, many CEOs may be keeping their heads down when it comes to China, even as they are still committed to it.

“A lot of people [in the business community] support Evan and respect him for having spoken out,” says Orlins. “Those in China for the Chinese market believe that it is fundamentally in the interest of the United States to have more trade investment between the United States and China.”

“The silent majority are endeavoring to make it work in a way that’s not just throwing good money after bad,” adds Omondi, of Z-Ben Advisors. “You do see, though, a deliberate effort made by companies to explain their long-term China outlook to shareholders.”

The corporate world, after all, has its share of grievances with China: I.P. theft, data security, challenges around acquiring licenses, the use of forced labor in supply chains and other practices deemed unfair or discriminatory.7Wang Huiyao, founder of the Center for China and Globalization, a think-tank, retorts that “there is much more unfair treatment of Chinese companies in the U.S. than what has been experienced by multinational companies in China,” citing the Entity List and threats to delist Chinese companies from U.S. stock exchanges. There is a long list of companies — such as Uniqlo, H&M, Nike, Intel and Walmart — that have suffered painful backlashes in China after criticizing government policies, even in the most mild of ways.

Given the track record, China hawks say that corporate doves like the Greenbergs are dangerously naive, as encouraging further engagement with China only strengthens an inevitable adversary intent on undermining U.S. interests in the world.

“People like [Hank] Greenberg don’t understand grand strategy,” says Edward Luttwak, a geopolitical consultant and author of The Rise of China vs. the Logic of Strategy. “They think that it’s pointless to resist China’s rise and why not just go along with it and be a beneficiary. If you want to induce the Americans to stop resisting China, you go to people like [Hank] and he’ll write obedient op-eds that say, ‘Don’t resist China.’”

Others note that it can be easy to have selective hearing when it comes to the CCP. Clyde Prestowitz, an economist and China watcher who has known Hank Greenberg since the 1980s, says that there is “a romantic streak in Hank about China.”

“He’s no dummy,” Prestowitz adds. “But I don’t know if he’s fully aware of how the Chinese Communist Party is operating.”

Evan, for his part, knows he won’t be seen as the private sector statesman that his father once was. As he told Orlins, he expects to be “vilified” or labeled a “mercantilist” for his viewpoints, but, he said, “you don’t do this for the popularity contest.”

All he hopes, it seems, is to get the business community invited back to the policy table — like the one his father once so aptly dominated in Washington.

“I raised my voice in the hopes that that will cause others to raise their voices as well,” he said, “so that we can have a balanced discussion about what’s in our national interests.”

Brent Crane is a journalist based in San Diego. His work has been featured in The New Yorker, The New York Times, The Economist and elsewhere. @bcamcrane