China dominates global solar production, and it’s not even close. In 2021, eight of the world’s top 10 solar manufacturers were Chinese, accounting for two-thirds of global shipments.

But while China Inc. has maintained a steady stranglehold on global solar output, the identity of the companies involved has been more changeable. Two of the biggest solar producers today, LONGi Green Energy Technology and Tongwei Solar, were just minor players in 2015, failing to break the top ten list. Even within an industry known for dramatic boom and bust cycles, the pace at which these two firms have reached the top is impressive.

This week, The Wire looks at the current leaders of the solar manufacturing race: who they are, how they got so big, and — amid a U.S. Commerce Department investigation into alleged tariff evasion by Chinese solar firms — their prospects of staying at the top.

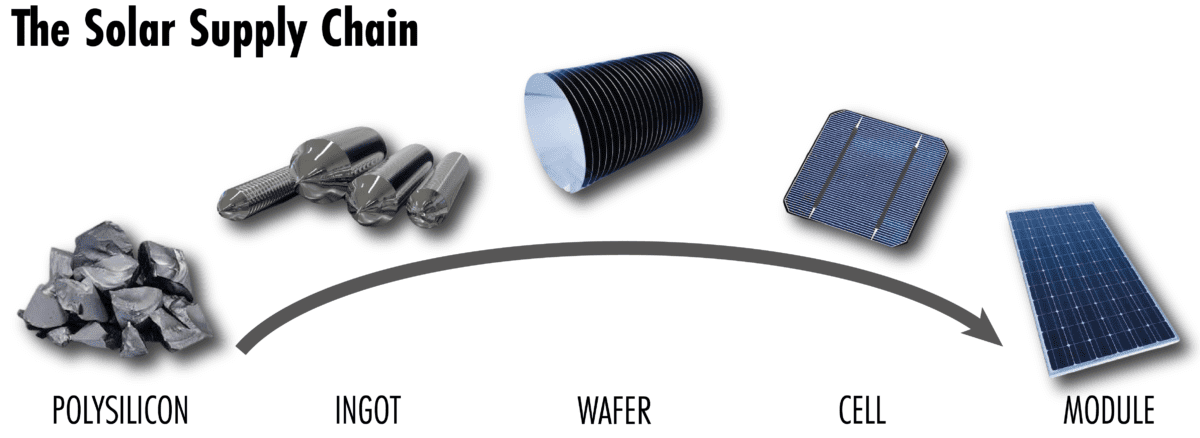

THE SOLAR PROCESS

The solar supply chain can be broken down into roughly five parts. The key raw material is polysilicon, a high-purity form of silicon used in most solar panels. Polysilicon is melted at high temperatures to make ingots, which are sliced to make wafers. A multi-step process turns wafers into cells, the all-important, electricity-generating component of a solar panel.

The fiercest industry competition lies here, at the cell level. Manufacturers that can eek the most electricity out of a cell, at the lowest cost, tend to achieve market supremacy. A collection of cells makes a module; a collection of modules makes a panel.

In recent years, a small circle of high-performing cell makers have come to dominate the industry. “Module manufacturers buy cells because, for the most part, they don’t want to get into cell manufacturing. It’s a brutal part of the market,” says Paula Mints, founder and lead analyst at SPV, a solar market research firm. The world’s top ten cell manufacturers grew their collective market share from 63 to 71 percent between 2015 and 2020.

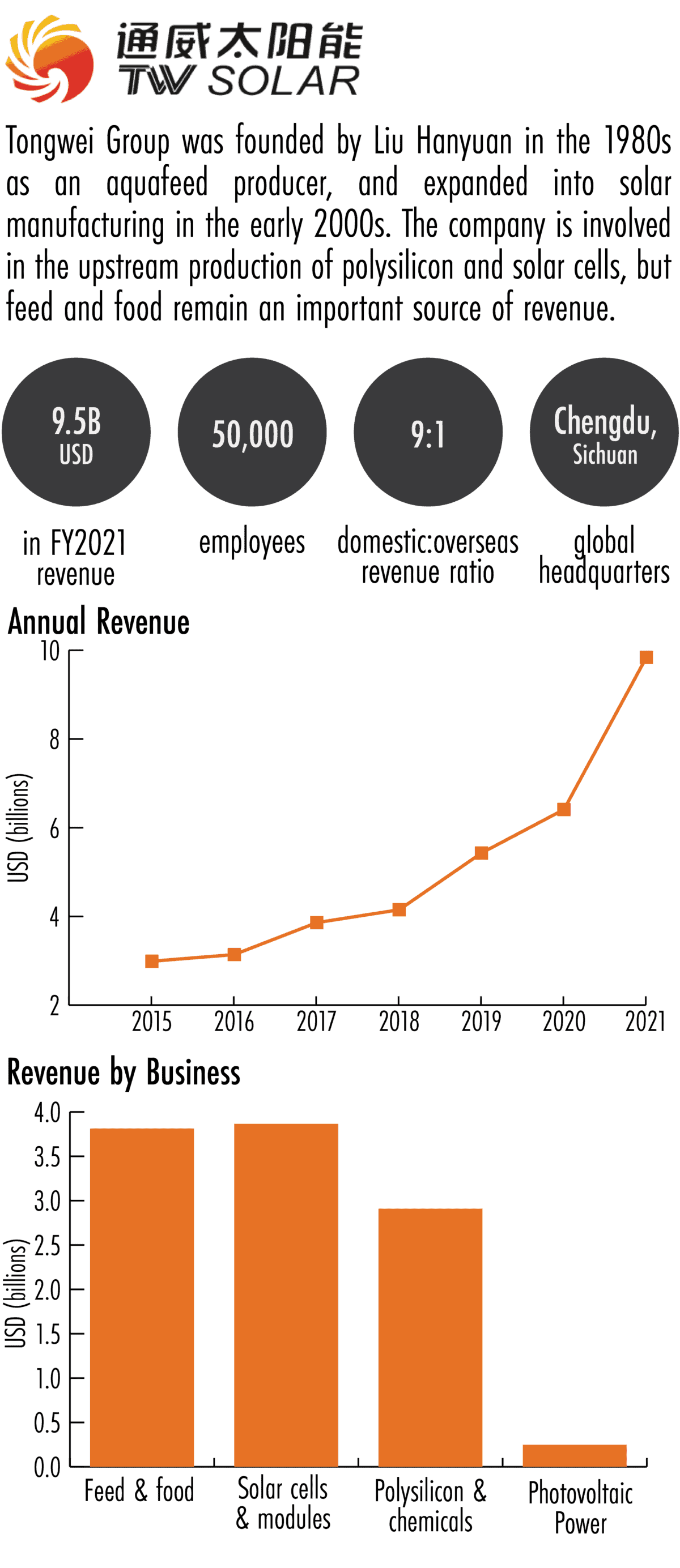

TONGWEI SOLAR

Tongwei Solar is the world’s largest solar cell producer by shipment volume, with a global market share of approximately 20 percent. Its brand may be little known to consumers, but many of its downstream partners are household names, including Samsung, Panasonic and Tata.

The Sichuan Province-based company, which has a market cap of more than $30 billion, started out making something a far cry from photovoltaics: fish food. It was founded by Liu Hanyuan, an engineer who had trained at the Sichuan Fisheries School at the time of China’s economic opening in 1978 — a period when fish was considered a luxury good.

Liu expanded Tongwei’s focus to solar power in the early 2000s, after completing a dissertation on new energy sources for his doctorate in business administration. The company began manufacturing polysilicon in 2008, and expanded into solar cell production after acquiring a loss-making cell and module business from a rival in 2013. Today’s Tongwei is a vertically-integrated solar juggernaut, producing its own polysilicon, wafers and cells. It’s also a key cell supplier to top module producers including LONGi, Jinko, and Trina.

Liu, who has become Sichuan Province’s richest man, has not forgotten his roots: Tongwei has become a pioneer of solar-aquaculture projects that integrate solar installations with fish farming.

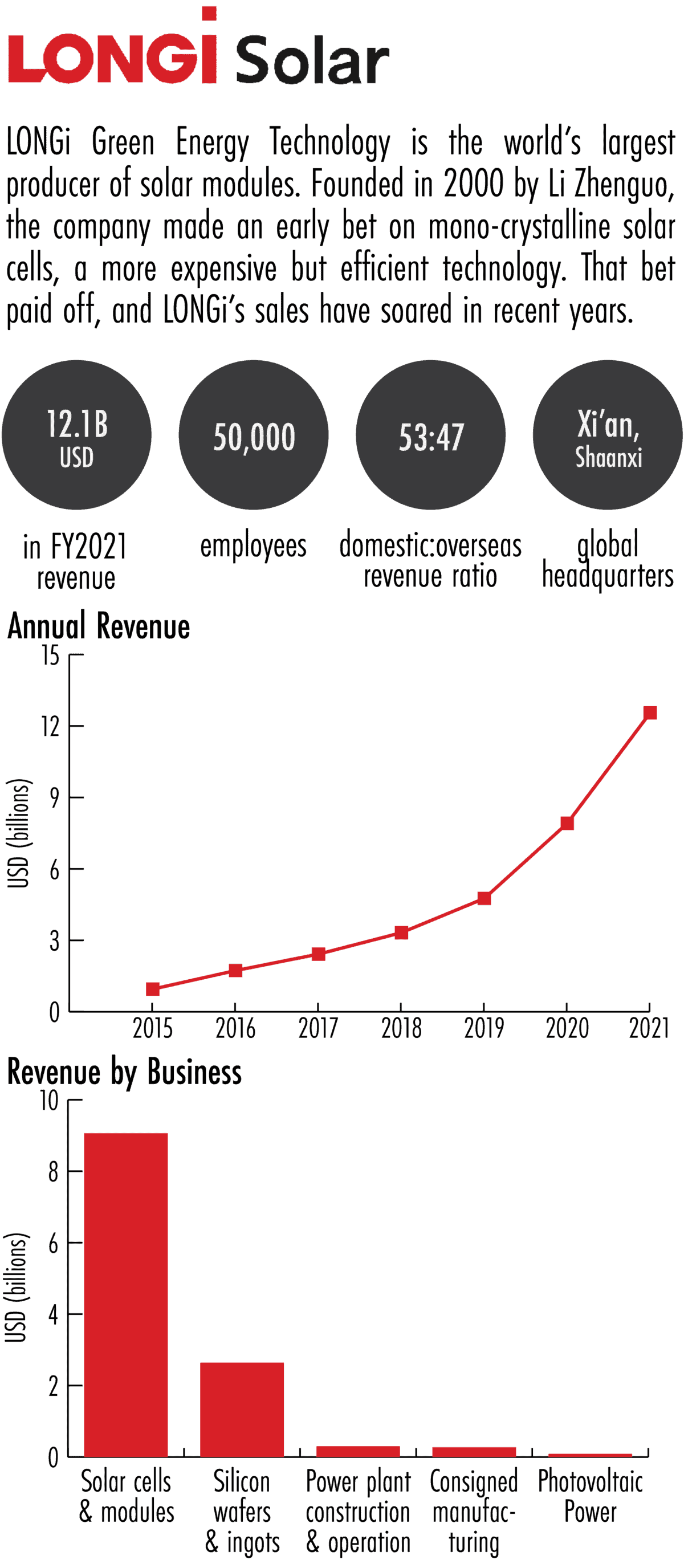

LONGI GREEN ENERGY

LONGi Green Energy Technology is king of the module stage of solar power manufacturing. The vertically-integrated company is a major producer of its own wafers and cells, but it also buys a large number of solar cells to assemble into modules and panels. Approximately 20 percent of all solar panel shipments that arrived at U.S. ports in the second quarter of 2021 were sent by LONGi and its subsidiaries.

LONGi was founded in 2000 by Li Zhenguo, a physicist by training who studied semiconductors at Lanzhou University (The company is named after the president of his alma mater, Jiang Longji). Li’s big bet was to focus on producing solar wafers from a single source of silicon — the so-called mono-crystalline method, a comparatively expensive process that ultimately produces more efficient cells than alternative processes used by many of LONGi’s early competitors. That bet has paid off in the last five years as solar panel prices have fallen, incentivizing manufacturers to compete on technology as much as cost. Monocrystalline cells made up 35 percent of the market in 2015: By 2021, they made up 95 percent.

LONGi’s mastery of this technology has seen its cells achieve records for efficiency. But several factors are now disrupting its run of success in the U.S., including its links to suppliers in Xinjiang that have been accused of using forced labor in their factories, such as Hoshine Silicon Industry Co., a silicon producer whose products were banned from the U.S. last June. In November, LONGi said that some of its shipments had been seized by U.S. customs agents — a portion was later released in February.

A second roadblock stems from the Commerce Department’s recent probe into whether Chinese manufacturers are circumventing tariffs by routing their solar panels through countries in southeast Asia. That investigation has all but ground to a halt hundreds of solar installation projects in the U.S., to the exasperation of the industry and even White House officials.

The U.S. has sought to use tariffs to incentivize solar manufacturers to shift production back to the United States, to little avail. Instead, imports have largely shifted to countries like Malaysia, Vietnam, Thailand and Cambodia, which account for 83 percent of imported solar modules.1Page 72 LONGi, for example, has factories in Vietnam and Malaysia. For comparison, the U.S.-made share of global solar shipments stands at just 1.2 percent.2Page 52

Experts doubt whether the tariffs and investigation will bring solar manufacturing back to the U.S.. “We don’t have anything to protect, really,” says Mints, the market research analyst. “We have no crystalline cell manufacturing. We’re protecting very little here, so it’s [the investigation] just kind of silly.”

Others say U.S. policy makers would be better off focusing on future challenges rather than established industries like solar where China is already dominant.

“I would rather see the government focusing on the next generation of technologies,” says David Hart, an energy expert at the Information Technology and Innovation Foundation, a Washington D.C.-based think tank. “Batteries are really worth worrying about, where we’re much earlier in the development of the industry and there’s much more of a chance to shape it.”

Eliot Chen is a Toronto-based staff writer at The Wire. Previously, he was a researcher at the Center for Strategic and International Studies’ Human Rights Initiative and MacroPolo. @eliotcxchen