Derek Scissors is a senior fellow at the American Enterprise Institute where he focuses on the Chinese and Indian economies and U.S. economic relations with Asia. He also serves on the U.S.-China Economic and Security Review Commission and as the chief economist of the China Beige Book, which provides reliable data on China’s economy. Scissors has served as a senior research fellow in the Asian Studies Center at the Heritage Foundation and an adjunct professor of economics at George Washington University. Scissors holds an A.B. in economics from the University of Michigan, an M.A. in economics from the University of Chicago and Ph.D.in international political economy from Stanford University.

Illustration by Kate Copeland

Q: Under Xi Jinping, the Chinese government has expanded its presence in corporate governance, seeming to blur the line between non-state and state-owned entities. Do you think Beijing is in danger of sacrificing growth for increased control over Chinese business?

I do think [Xi] is willing to sacrifice growth for control. This sacrifice is not the goal, though. The goal is to have more control and retain innovation. It’s this magic line China always wants to walk where they say, “Well, the state is the principal, but the private actors are the agents.” Xi Jinping will accept the tradeoff of growth versus control, which is very likely, but probably some people in China think that tradeoff can be avoided to some extent.

You can see it in their macroeconomic statistics. They have become more honest in the last six months. They’ve revised some of their key indicators. They were willing to report a whole half year of GDP growth at 4 percent and that’s because I don’t think it matters as much to Xi. He wants the growth but also his other objectives to succeed. If the country is stable, if there isn’t opposition to him, if there isn’t what he sees as some sort of undermining of Chinese character, he will welcome the growth. However, these aspects of control have greater weight to him than they did under Hu Jintao and certainly under Jiang Zemin, and growth has less weight. So, I think they are willing to accept growth costs, which are not ideal and not something they want to do, but they’re willing to accept them. And once you do that, they’re going to say, “I’d rather have a private sector that knows who is boss than a private sector that is thinking that they can innovate freely.”

Is it appropriate to say a non-state sector even exists in China today?

You’re saying non-state and that is a good term. We shouldn’t say private. The reason we shouldn’t say private is that Chinese firms have never been private like American firms. It’s always been the case that if you get tapped on the shoulder by the Ministry of Public Security, the Ministry of State Security, or whomever, that you stopped being a private firm, and now your interests are the state’s interests. You don’t have the courts, you don’t have the media, you don’t have rights.

Saying non-state is nerdy, but it’s right because we shouldn’t think of these as private entities; but they’re still not the same as the state sector. Xi Jinping says, “I’m going to be telling you what to do more than you thought previously. Get used to it.” But they’re still not the same as SOEs.

Xi Jinping’s government has also pushed for an increased role for CCP committees in foreign owned and invested firms. What are the tangible repercussions this could have on American companies and on national security?

What it means in practical terms is that when you convene the decision makers of a firm, there’s a party representative there. That’s the goal of these CCP committees. And that didn’t used to be the case. If you had a joint venture and when you met to control the joint venture, you would meet with Chinese counterparties, but they weren’t necessarily party members. Now, you can have a “wholly privately-owned venture” in quotes, yet there’s a party representative there, and the party may own a tiny little amount [of the company].

| BIO AT A GLANCE | |

|---|---|

| AGE | 56 |

| BIRTHPLACE | Stuttgart, Germany |

| CURRENT POSITIONS | Senior fellow at the American Enterprise Institute, Commissioner at US-China Economic and Security Review Commission, chief economist at China Beige Book |

Now the weird thing is that there’s an advantage for foreign firms, as well as a disadvantage, when it comes to the CCP committees. The advantage is that foreign firms in China have always had to guess what’s ok. Xi Jinping has been so erratic the last few years in his behavior — and potentially could be further if he feels his political position is not set — that it’s a difficult environment to operate in. So it could be that if you have a party person in your management team who knows what’s going on, which is not guaranteed, that you could be able to turn to this person and say, “Are we allowed to do this?” And that would be more transparency in the business environment than they’ve had the last few years.

Now the downside is obvious, which is they may say no to your request. So, on the one hand, it could clarify the situation, but on the other it’s putting in more concrete interference in the operations of foreign firms and on a net basis this is a negative. I want to be clear in saying that there’s going to be interference in the operation of foreign firms under Xi Jinping anyway, so not having this person at the meeting doesn’t really matter that much.

Some argue this greater interference in the non-state sector is all part of the government’s effort to accelerate China’s technological growth, and hence its overall growth rate. What’s your take on that?

I’ve been saying Chinese growth prospects are in trouble since they spent all that money and leveraged up so much in 2009. And you see the rate of growth is declining. They smooth it out, but it was 10 straight years of weakening. For a while, people didn’t believe it and when they start to belatedly believe it, they got the “technology is coming to the rescue” slogan. And the “technology coming to the rescue” argument was always difficult because the Japanese tried that, and they failed. And the Chinese are going to have even bigger demographic problems than Japan. So, it was always a strain to say technology could come to the rescue given China’s debt issues and the demographic issues.

People who think the state can power the second largest economy in the world through tech investment are living in fantasyland. There’s just absolutely no evidence.

They made that harder to accomplish. They don’t see that, but it is the case because China is not Israel. Israel is a very innovative country. But if Israel has one major innovation, it’s all set for the year because there are 9 million people. Nine million people is like a mid-sized Chinese city. You need a lot of innovations, and the state can’t direct that level of innovation. If China wants to be a space power, then, yes, the state can make that happen. If China wants to compete in machine learning, then, yes, the state can make that happen. But when you’re trying to figure out what are the innovations that are going to drive an economy, there’s no sign that they can do it.

People who think the state can power the second largest economy in the world through tech investment are living in fantasyland. There’s just absolutely no evidence. Is there evidence that the Chinese private sector could do it if allowed to? Maybe, maybe not. Is there evidence the state can bring certain technologies to bear that matter? Yes. But that the state can direct technology to drive Chinese growth? No, it won’t work.

Shifting to the U.S. side of things, do you think that the Trump administration’s dramatic shift in policy towards China was overall good in terms of timing and measurement? How has the Biden administration improved, worsened, or sustained its predecessor’s strategy?

The Trump administration’s shift towards a tough China policy was fake news. There’s a lot of rhetoric and we’ll have a lot of anti-China rhetoric at least through the 2024 election. It doesn’t mean anything.

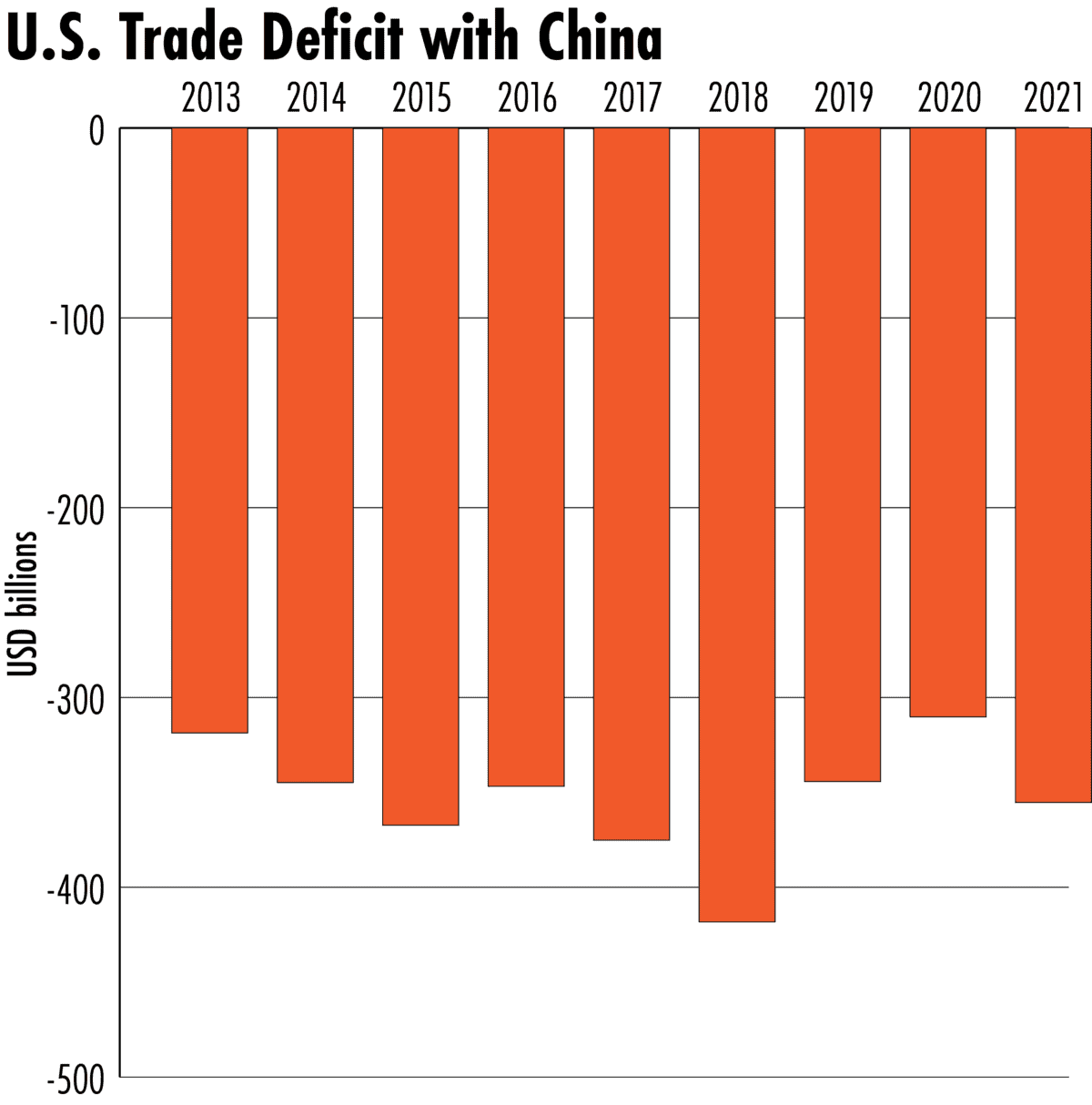

President [Trump]’s main economic action he was very proud of was that he eventually put on 25 percent tariffs on the bulk of imports into the U.S. from China. Well, the trade deficit is larger than when he took office. When he ran against the trade deficit, he said, “It was the greatest theft in history and millions of jobs are being lost” and now it’s larger than it was, and we had his tariffs. He was wrong in caring that much about the bilateral trade deficit, but on his own terms, he failed.

Meanwhile, during the Trump administration, the stock of U.S. portfolio investment in China went from $368 billion to $1.15 trillion. It grew by $780 billion, nearly $200 billion a year. That completely dwarfs all the trade effects. While we were fighting the economic cold war with China, we were giving them a ton of money. It’s a fraud. The Trump administration’s China policies were a fraud. Does that mean there was no one in the Trump administration who wanted to get tough on China? There absolutely were. But that’s not what the President wanted. The President wanted to put on tariffs, say that was great, bring the Chinese to the table, get some export quotas (which the Chinese did not fulfill), and declare victory. On his own terms, he failed.

The Biden administration has not been willing or able to change China policy. They stuck with phase one of the trade deal, which was a bad deal at the beginning and was never going to be fulfilled. If you abandon phase one, then what are you going to do? We have a supply chain problem exposed by COVID, it was there before, and the Trump administration did nothing about it. The Biden administration has written the equivalent of a grad student paper about it. They’re supposed to do something about it this month, we’ll see. I can’t blame the Biden administration for making things worse. However, they have failed to make things better.

They can point back at the Trump administration and say the Trump people have no cause to criticize them. That’s fine. But everybody outside of the administration does have cause. It is not competing with China to borrow a bunch of money for domestic programs. That does not make the U.S. stronger versus China. And that’s the centerpiece of the Biden administration’s approach. We have had five years of loud talk and action that has on net increased U.S.-China economic ties.

So, in your opinion, what should the Biden administration do tomorrow?

This is not my personal priority, but I would say we have to pull supply chains out of China in areas we find critical. We can fight over what’s critical. I don’t think low-end semiconductors are critical. I think medical supplies and equipment have shown to be critical and active pharmaceutical ingredients, which are supplied by Chinese fine chemicals, have been shown to be. We need to identify the supply chains that matter most to the United States. We cannot rely on the Chinese. The companies resisting our independence, saying that “oh, I need this for my business,” they need to shut up.

…[W]e have to pull supply chains out of China in areas we find critical. We can fight over what’s critical. I don’t think low end semiconductors are critical. I think medical supplies and equipment have shown to be critical and active pharmaceutical ingredients which are supplied by Chinese fine chemicals have been shown to be.

Does that mean we should pull 30 supply chains out of China tomorrow? No, but we should pull three or four. We need to say that we’re taking these away and that China cannot participate in supply chains at all because they will disrupt them. Do we want to relocate them to the U.S., do we want to relocate them to treaty allies, do we want to relocate them to free trade partners? These are the decisions to be made.

Why has the U.S. pursued a bilateral approach to China instead of getting its allies to work together?

The Obama administration in its second term just failed on China policy completely. Just a total failure. People won’t like hearing that. The first term they had a domestic agenda, it was a priority, that’s what should have happened. In the second term, they had stabilized the domestic economy, pat President Obama on the back, and then say, “What the hell are you doing on China?” Then the Trump administration comes in and we repeatedly have the Trump administration being angrier at our allies than they are at the Chinese. President Trump repeatedly said Europe is as bad as China, only smaller, which is a hysterically funny insult. I got into a screaming match with a senior Trump administration official saying that the German current account surplus and the Chinese current account surplus shouldn’t be compared because one is our friend and a democracy, and one is not our friend and a dictatorship. But that wasn’t his perspective.

Yes, this should be a multilateral endeavor, but it won’t work until the U.S. shows leadership. Now after we passed CFIUS, a bunch of countries, including in Europe, said “we need investment reviews too,” because we showed it could be done and we gave them a template to work from. A coalition to confront the Chinese does not happen without American leadership and American leadership can’t look like getting into a room of 20 countries and saying, “What do you guys think?”

The Obama administration wouldn’t do it, the Trump administration got in the room with 20 countries and said, “I hate half of you,” and the Biden administration is trying to do it, but they have not shown the willingness to make any difficult decisions either.

The U.S. has put new restrictions on Chinese investment into the U.S. and American companies. How effective have these restrictions been and what is the future for Chinese investment?

Chinese investment in the U.S. slowed down originally because the Chinese were worried about it. There was a lot of capital outflow in China starting in 2014 and it reached a peak in late 2015 and into 2016, which is when the record for Chinese investment in the U.S. outside of bonds was set. And the Chinese start to get worried over the course of 2016 that too much money was leaving the country.

They’re the ones who put the clamps down. Now Chinese investment in the U.S. outside of bonds has dropped to nothing. I mean, it’s a billion or a couple of billion dollars depending on how you measure and what you count as a Chinese firm and so on. But it’s totally trivial. That’s partly because the Chinese don’t want it to be as high as it was. And it’s partly because of the restrictions we’ve put on.

…[I]f CFIUS is working well, which it looks like it is, that argues very strongly for looking at investment from the US to China, which we’re not doing.

Can you tell if CFIUS is working great? No, because there’s money under the radar, they might be buying small tech firms. But I think it’s working well. We’re not seeing Chinese investment buy up highly valued U.S. assets they shouldn’t be allowed to buy. If we reform CFIUS to prevent, among other things, Chinese acquisition of U.S. technology here, what the hell are we doing allowing U.S. money pour into Chinese developed technology? So, if CFIUS is working well, which it looks like it is, that argues very strongly for looking at investment from the U.S. to China, which we’re not doing.

Are U.S. export controls on sales by American companies to China strong enough and an effective measure to enhance national security? What is their purpose?

Congress, when it passed CFIUS reform, did the right thing and recognized that another way the Chinese acquire technology is through American exports. And they reformed and tightened export controls, and they tightened them through two channels: one, emerging technologies we’re not sure of, and two, foundational technologies, which we are pretty sure of, and we don’t really want to help the Chinese acquire and improve. On emerging technologies, the Department of Commerce has taken some actions. Are they adequate? Probably not. It’s hard to tell with emerging technologies. They’ve taken several dozen actions since Congress passed this legislation in the last three and a half years. And that’s not nothing. Emerging technologies are difficult to assess.

On foundational technologies Commerce has done nothing, zero, not taken a single action. Commerce’s response is, “We don’t want to have foundational technology controls until we have multilateral cooperation, because otherwise we’ll lose business for American firms.” But they’re never going to get multilateral cooperation until they’re willing to act and in three and a half years, they haven’t been willing to do anything. So, show you’re willing to act and then say, “alright, now our partners need to follow us.” And if they don’t, we have a problem in their policy or our policy in coordination. And if they do, then you can move on.

Commerce thinks that lost sales of foundational technology are more important than the national interest. We have leaks. We have an export control regime in place, but we have leaks in it because the Department of Commerce does not see its primary job as protecting the national interest. It sees its primary job as protecting business for U.S. exporters.

How should American financial regulators approach nominally privately-owned Chinese companies seeking investment, business, and potential public offerings in the United States?

The nominal ownership of the company does not matter. If it’s a state-owned enterprise making a solar powered car or a bus, who cares? Even if it’s a state-owned enterprise, go ahead and invest in it. It does matter if it’s a private firm pushing the boundaries on China’s biotech capabilities — don’t support that. That is a potential nightmare for the United States and the world. Not tomorrow, but down the line. Don’t help them.

The ownership status of the company doesn’t really matter. What matters is the activity of that company because the Chinese private firm that has been left alone by the government, that all of a sudden has a breakthrough in a sensitive technology, now belongs to the state. The end. There’s no argument. There’s no reasonable person that can say otherwise. It would happen very quickly. We cannot support activities which threaten to give China important technologies, and it doesn’t matter about the ownership of the entity. If there are Chinese companies involved in harming U.S. foreign policy interests, fine blacklist them, but if they’re not, then give them money. Who cares?

Is it possible for the U.S. to decouple from China in a meaningful way, even if it is a national security necessity? And more generally, how will, or should the U.S. and Chinese economies interact in the future?

Sure, it’s possible. Xi Jinping could decide that he needs to cement his legacy by taking over Taiwan by force. There will still be American companies wanting to do business in China while we’re at war with the Chinese. That’s how bad some of these companies are, I’m not exaggerating. But they won’t be able to, and financial flows back and forth will be stopped and so on. We could decouple, we could have this forced on us by the Chinese. It would not be smart for us to initiate a sudden war decoupling scenario.

People who say there’s no way Xi Jinping will take Taiwan would have said there’s no way Xi Jinping would break Deng Xiaoping’s word over protests in Hong Kong, and yet he did. Do I think he’s going to attack Taiwan tomorrow? No. This would be more on the lines of if he feels his political position is threatened, which is I think more likely to occur around 2027. We should not be supporting or becoming dependent on a cult of personality dictatorship. This is obvious. Why don’t we do it? We want the problem to magically solve itself and it won’t.

It will be costly. Do we have to completely decouple? No. I don’t mind U.S. outbound investment in Chinese consumer products, that’s fine. If that’s to the tune of another $150 billion a year, go ahead. Chinese old-age services are going to be the biggest market in the world, go ahead. But there are a lot of things we should not be investing in, and we should not have a powerful pro-China business lobby in this country, which we have in both parties. Comprehensive decoupling is unfortunately possible, and it would be not a good idea and it would be very painful. Partial decoupling on the other hand: we’re going to be sorry if we don’t do it.

Garrett O’Brien is a student at Harvard University studying how China interacts with the rest of the world. His research interests include Chinese international development projects and financial regulation.