Credit: rblfmr, Shutterstock

At the start of this year, Luckin Coffee was sitting pretty. On January 17, its Nasdaq-listed stock hit its all-time high — just above $51 per share — and its market capitalization passed $12 billion. The company also announced it had opened over 4,500 stores, overtaking Starbucks in China.

The coffee startup, founded in 2017, was touted as tech-savvy with a business model that focused on pick-up and delivery and payments made primarily through its mobile app. But in January, an anonymous report — backed by several prominent short-sellers — alleged it had been fabricating its sales. Luckin’s stock price plunged to less than $5 before trading was halted on April 7.

In this week’s edition of The Big Picture, we introduce readers to the people behind Luckin Coffee, the institutional investors who fell for Luckin’s inflated numbers, and the short-sellers who suspected Luckin’s numbers were too good to be true.

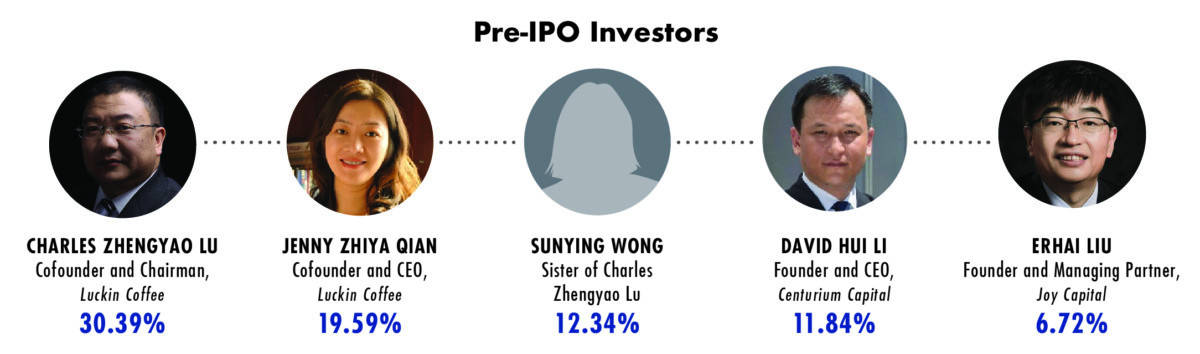

Insiders

Five people owned more than 80 percent of Luckin Coffee at the time of its IPO. Its co-founders, Charles Zhengyao Lu and Jenny Zhiya Qian, owned double-digit stakes, and Lu’s sister, Sunying Wong, owned another 12 percent — all through Cayman Islands companies.

Several members of the company’s board, including Chairman Lu, used their Luckin shares as collateral to borrow hundreds of millions of dollars from global investment banks, including Credit Suisse. Luckin also rented office space and advertising services from UCAR Inc. and related companies controlled by Chairman Lu.

David Hui Li and Erhai Lu were major early investors through their venture capital and private equity firms, Centurium Capital and Joy Capital. They each had business ties to UCAR and sat on Luckin’s board of directors. Both firms were exposed to major losses after the crash, though Centurium sold 25 percent of its Luckin holdings for $232 million in January.

Data: Luckin Coffee IPO Prospectus, SEC

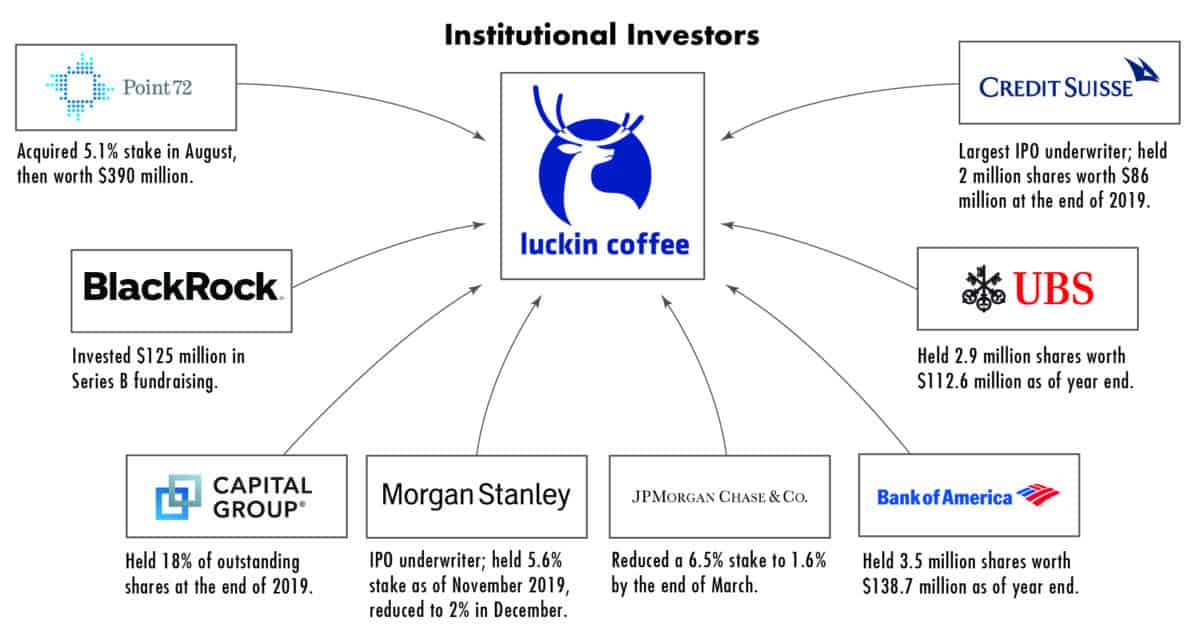

Institutions

Some of the world’s biggest and most sophisticated asset managers bought into Luckin’s model. In April 2019, BlackRock invested $125 million in Series B fundraising. Credit Suisse led its IPO, as the single largest underwriter of Luckin stock, followed by Morgan Stanley and the state-backed investment bank China International Capital Corporation, or C.I.C.C. UBS and J.P. Morgan were among Luckin’s top institutional investors. Legend Capital — which has ties to Lenovo — and GIC, the Singapore’s sovereign wealth fund, also bought early stakes.

Some of these institutions had cashed in before Luckin’s big crash — BlackRock, for example, had sold much of its stake before January — but plenty still believed the hype. In its quarterly earnings reports to investors, Luckin touted an aggressive strategy for growth, including opening 717 stores in the third quarter of 2019 alone. In January, Howard Penney, an analyst for the online financial program Hedgeye, called Luckin “the most digitally savvy company in the world.”

Data: S&P CapitalIQ, SEC filings

Short-sellers

Despite proclamations like Penney’s, a cloud of suspicion began to form late last year. Circulating among short-sellers was an anonymous report, based on thousands of hours of surveillance footage at Luckin stores, alleging that the company had fabricated millions of dollars in sales.

Carson Block’s firm, Muddy Waters Capital, tweeted Jan. 31 that they were short Luckin. Citron Research hit back, claiming that data from app sales and calls with competitors corroborated Luckin’s financials. But Anne Stevenson-Yang, founder of J Capital, issued her own report saying Citron had misinterpreted the data and that the anonymous report was credible. Jim Chanos, known as the “dean of short-sellers” and famous for his bet against Enron, said he too shorted Luckin.

In April, Luckin admitted that its chief operating officer and some other employees had fabricated $310 million worth of revenue between the second and fourth quarter of 2019, beginning ahead of its I.P.O. on the Nasdaq Stock Market. Eleven billion dollars of wealth has vanished since January.

Graphics and design contributed by Hiram Henriquez from Miami.

Emma Bingham is a Boston-based editor for The Wire. Previously, she was editor in chief of The Tech at the Massachusetts Institute of Technology. @emmapbingham

Kara Greenberg is an editor at The Wire. @karagreenberg_