In 2002, when Xu Jiayin wanted to take his property business public for the first time, he teamed up with a company linked to the brother of Wen Jiabao, who was about to take over as China’s premier. Years later, after his company, Evergrande, had grown into China’s second largest property developer, three Hong Kong billionaires who Xu played poker with gave him cash infusions to help settle some debts. When Xu took a wild leap into electric vehicles, he pitched the project to Jack Ma at a dinner party — and ended up securing an investment from Ma’s fund. And then last year, in a bid to save his increasingly indebted company, Xu convinced the CEO of a Chinese retail conglomerate not to collect the $3 billion that Evergrande owed him.

In other words, Xu — who is also known by his Cantonese name, Hui Ka Yan — has a knack for convincing important people to back him and then catch him when he falls. In Chinese business culture, this talent for cultivating personal relationships in order to facilitate deals is known as having good guanxi — and Xu Jiayin is considered a guanxi genius.

“He is very generous with helping his friends,” says Chen Zhiwu, finance professor and director of the Asia Global Institute at the University of Hong Kong (HKU). “He can easily throw hundreds of millions, or even billions into something. It is important to have that perspective in understanding how Xu came from a modest family to where he is today. His guanxi had to have been pretty good.”

Evergrande is now on the brink of collapse. But before that,1Evergrande failed to make a $150 million bond payment on Monday after missing $130 million worth of payments in the previous week Xu Jiayin was one of the most powerful business people in China. His property giant had $78 billion in annual revenue last year and more than 1,300 projects in 280 Chinese cities. At its peak, Xu’s net worth was estimated to be $43 billion. Indeed, one of the reasons Evergrande got away with carrying such excessive debt over the years, analysts say, was because creditors assumed Xu’s extraordinary guanxi would always step in and save him.

This isn’t as far-fetched an assumption as one might think. Observers note that Xu was uniquely able to curry favor partly because of the way the real estate sector functions in China. While real estate industries across the world are prone to insider dealing, it is particularly susceptible to manipulation in China, where the government technically owns all land and sells it to the highest bidder.

“Xu Jiayin has probably had a project in every prefecture-level city in China. That means he has helped the economic development and personal wealth of thousands of prefecture-level government officials,” explains Victor Shih, a professor at the University of California, San Diego who specializes in Chinese elite politics and fiscal policy. “That buys you a lot of political capital, including with many officials who are now in the Politburo.”

Xu Jiayin has probably had a project in every prefecture-level city in China… That buys you a lot of political capital, including with many officials who are now in the Politburo.

Victor Shih, a professor at the University of California, San Diego who specializes in Chinese elite politics and fiscal policy

While being close to influential people is important for doing business in every society, the concept of guanxi has had an outsized role in China’s rapid economic ascent over the past 40 years. As the Chinese government chased economic growth at all costs, the authorities seemed to ignore much of the unscrupulous behavior of the nation’s business elite, including their attempts to acquire political connections.

Yuen Yuen Ang, the University of Michigan scholar and author of China’s Gilded Age, calls this form of corruption “access money” and says it functioned as the steroids of Chinese capitalism. “By rewarding politicians who serve capitalist interests and enriching capitalists who pay for privileges,” she has written, “this now dominant form of corruption has stimulated commerce, construction, and investment, all of which contribute to GDP growth. But it has also exacerbated inequality and bred systemic risks.”

The recent publication of Red Roulette by Desmond Shum, an insider who made deals with the country’s political elite before leaving China, provides a front row seat to the oftentimes shameless entanglements between China’s tycoon class and the Chinese Communist Party (CCP) over the past few decades — all in the name of building the “New China.” Still, among that rarified group, Shum writes that Xu’s tactic of “giving outrageously expensive gifts” to win connections was particularly “bald-faced.”

As a result, Xu Jiayin became something of an archetype: the very model of how business people became successful in early twenty-first century China. Following a rags-to-riches trajectory, he greased palms, nurtured networks, and rode the liberalization and rapid expansion of the Chinese economy to become the nation’s richest man. And once he ascended to the very top of China’s business elite, he wanted everyone to know.

“Xu is very flashy,” says Dexter Roberts, a senior fellow at the Atlantic Council’s Asia Security Initiative and the author of The Myth of Chinese Capitalism, noting that when Xu wore a gold Hermes belt to a somber Chinese political meeting, he earned the nickname ‘Belt Brother.’ “He is clearly emblematic of extreme wealth in China, and for a long time, he wasn’t afraid to show it.”

Beijing has taken increasingly drastic steps against private entrepreneurs — including Wanda’s Wang Jianlin and HNA’s Chen Feng — but Evergrande’s sheer size and Xu’s impressive guanxi made him seem untouchable. When Andrew Left, a well-known short seller, published a damning report on Evergrande in 2012, Hong Kong’s financial regulator barred him from trading in Hong Kong and forced him to repay what he made from shorting the stock. More recently, even as the government was signaling that it wanted to curtail real estate lending, Citic Group, the powerful state-owned financial conglomerate, reportedly loaned $10 billion to Evergrande.

“Xu is very well connected at all levels. He is a master player,” says Chen.

The game, however, seems to have changed on him. While Beijing’s decision to look the other way paid off — China is considerably richer thanks to tycoons like Xu and the companies they led — China’s economy today is in a much different position. The single-minded pursuit of growth created structural problems, exacerbated inequality, and set up a system in which connections, not performance, were incentivized. Today, the massive debts — $300 billion in liabilities, to be exact — that Evergrande piled up under Xu’s leadership are threatening to trigger an economic crisis.

China’s debt-fueled real estate bubble has been an open secret for years, but since 2017, when Xi Jinping said that housing is “for living in, not for speculation,” Beijing has issued warnings about its desire to change the industry. Last year, the government finally drew a clear line in the sand, enacting a series of policy changes to restrict lending. Now, with Evergrande’s debts coming due, Beijing is taking steps to contain the Evergrande crisis, but does not seem willing to directly bail out the company, as many observers always thought it would do. Evergrande did not respond to requests for comment.

“These systems generated massive economic growth, but also created risky corruption,” says Meg Rithmire, a professor at Harvard Business School and an expert on state-business relations in China. “The CCP wants to say that they are no longer tolerant of this kind of financial behavior, and Evergrande is a great company to nail against the wall — because everyone will notice.”

Although Xu stepped down as chairman of the company’s main property unit in August, he seems to remain on the front lines of the last-ditch attempt to save his company. In a letter to Evergrande employees in September, Xu acknowledged that the company “has encountered unprecedented difficulties.” He went on to extol Evergrande’s “army of loyal, immensely hardworking staff” who “are never defeated and only grow stronger in adversity,” before promising that, together, they could “overcome all difficulties and win this war.”

Who Evergrande’s enemy is, however, remains less clear.

PARTY ON, XU

From his plush red velvet chair at the Tiananmen Square gate tower, just above the portrait of Mao Zedong, Xu Jiayin looked out over the celebration filling Beijing’s most famous square. Flag-waving performers, military tanks, and bright red fireworks were on display, all in celebration of the nation’s 70th birthday. It was 2019, and Xu’s seat — not far from the country’s top leaders — was seen as a great honor, the culmination of years of hobnobbing with China’s political elite.

Xu, 60 years old at the time, probably marveled to himself at how far he’d come in life. Not much is known about Xu’s early years, but he has described his childhood as humble — in one speech, he even said, “I myself have a deep understanding of poverty.” After his mother died, he was brought up by his grandparents in rural Henan, went to college in Wuhan — where he says he received state subsidies because he had no money to support himself — and then returned to Henan and spent a decade working at a state-owned steel mill.

It wasn’t until 1996 that he took what looks like a leap of faith. He moved to Guangzhou, one of the country’s early special economic zones, just as the city was experimenting with housing reform, moving away from state housing to a private market.2A paper on housing reform in southern China Xu started a private real estate enterprise — what later became Evergrande. To this day, it’s unclear where Xu got his initial capital for the venture, but his first development, Jinbi Garden, netted $12 million in sales. Seeing the potential of a new middle class eager to become homeowners, Evergrande expanded — first in Guangdong, and then in other provinces — by aggressively borrowing money to buy up land.

“What made their success is exactly what is causing them trouble right now,” says Zhu Ning, deputy dean at the Shanghai Advanced Institute of Finance and author of China’s Guaranteed Bubble. “They were an aggressive developer, and they thought land prices and demand for housing would keep going up.”

Evergrande’s rapid expansion meant Xu quickly linked up with a wide network of politicians. In China, in order to finance basic government functions, local governments buy land from farmers at very low prices and then sell it to developers like Evergrande for a huge profit. “The only thing happening economically in some of these poorer places is infrastructure and property development,” says UCSD’s Shih.

Shih contrasts Xu to Jack Ma, explaining that while Alibaba has a much bigger impact on China’s overall economy, that impact is mostly concentrated in Hangzhou, where Alibaba is located. “Ma’s guanxi net is in the dozens, but Xu Jiayin has invested in hundreds of Chinese cities — he has a rolodex of thousands of officials,” says Shih. “Counterintuitively, Jack Ma’s ability to mobilize someone in the government is less than Xu Jiayin’s.”

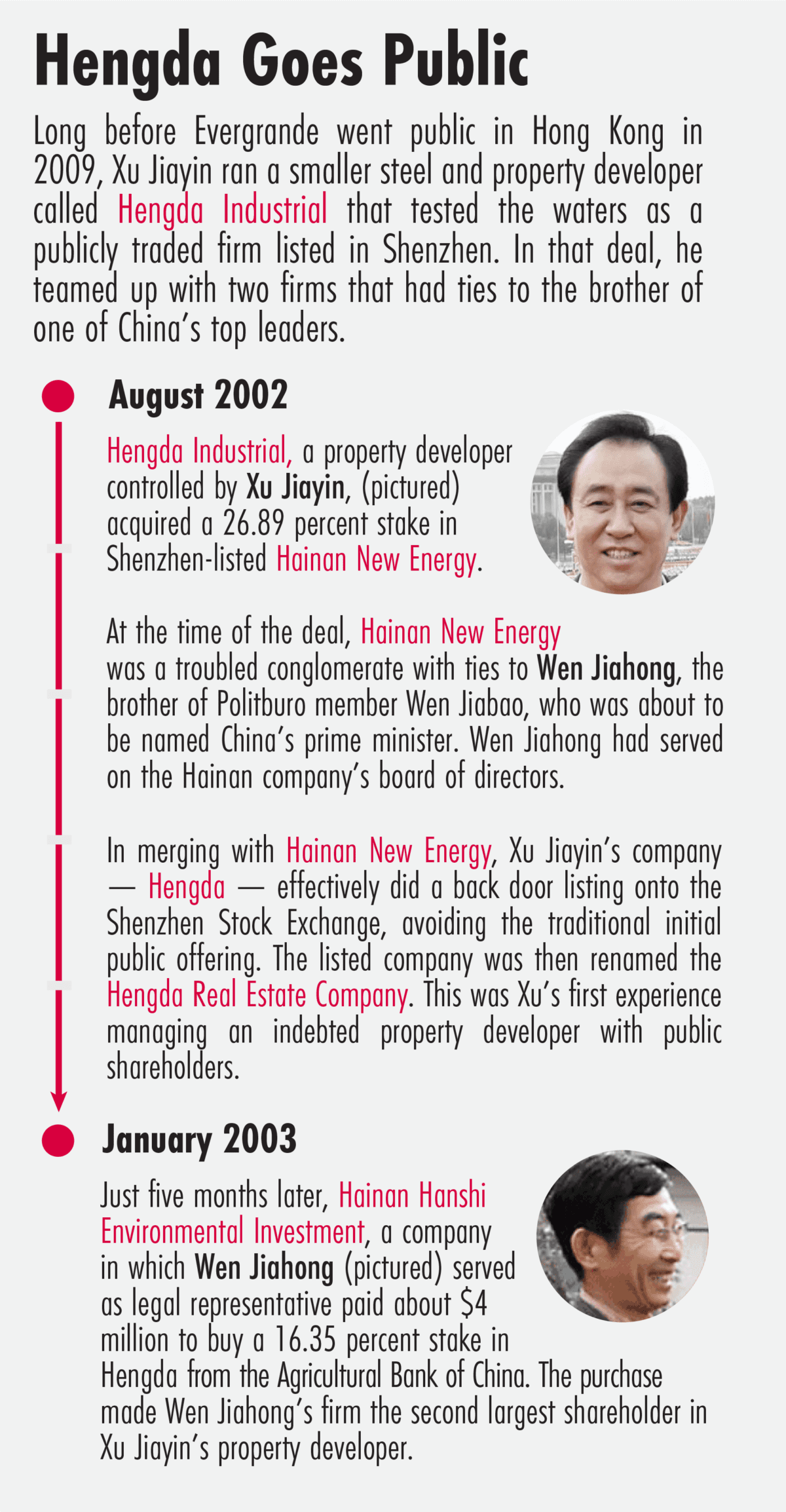

From the start, however, Xu’s rolodex included people at the highest levels. In 2002, Evergrande’s predecessor company, Hengda Industrial, went public through a backdoor listing in Shenzhen by buying a 26 percent share of Hainan New Energy, a troubled, public company whose founder, according to Chinese media, had been accused of corruption in the years prior. The name was changed to Hengda Real Estate. According to corporate records reviewed by The Wire, Wen Jiahong, an active businessman and the brother of Wen Jiabao, who became China’s premier, had served on the company’s board of directors. Xu’s connection to the Wen family doesn’t stop there: In 2003, the very same year that Wen Jiabao became premier, a company in which Wen Jiahong served as legal representative bought 16 percent of Hengda Real Estate, Xu’s then listed company, making Wen’s company the second-largest shareholder, according to corporate records.

Xu’s guanxi advanced considerably in the following years. In 2008, Xu secured a spot in the Chinese Political Consultative Conference, a political advisory body that includes a group of select entrepreneurs. He also seems to have developed personal relationships with the families of the Politburo around this time. According to Cersius Group, a Montreal-based consultancy focused on Chinese elite politics, Xu is closely connected to the family of Zeng Qinghong, who was China’s Vice President from 2003 to 2008. He owned a mansion, for instance, next to Zeng’s son in a glitzy oceanside suburb of Sydney. And, in Red Roulette, Shum describes Xu’s travels to Europe in 2011 to sample wine with the daughter of Jia Qinglin, who served on the Politburo Standing Committee at the time. On that same trip, Shum writes that Xu went to visit a $100 million yacht docked on France’s southern coastline: “Xu envisioned a floating palace to wine and dine officials off China’s coast, away from the prying eyes of China’s anti-corruption cops.”

In 2006, according to company documents, Evergrande sold its stake in the Shenzhen listed company, Hengda Real Estate, and initiated an extensive corporate restructuring with the goal of bringing a new property company public by 2008, in Hong Kong. Unlike in Shenzhen, a Hong Kong listing meant access to foreign capital and the backing of Wall Street banks, including Morgan Stanley. Xu even got an honorary doctorate from the University of West Alabama, perhaps in an effort to flaunt his American education to foreign investors.

But with the global financial crisis roiling international markets at the time and questions already emerging about Evergrande’s extensive debt and business approach, the listing failed. After raising some capital from his poker buddies — Hong Kong developers Joseph Lau and Cheng Yu-tung — and a few Western banks, according to the prospectus, Evergrande successfully listed the next year, but at a much lower price, raising only 34 percent of what it had initially hoped.

While the Hong Kong listing was a significant setback for Evergrande, Xu seemed uninterested in reconsidering his aggressive borrowing approach. The cash infusion helped pay back some of the company’s debt, but Evergrande went on to incur significantly more as it began to rely on “pre-sales”: customers paying for developments that were not yet constructed. This meant that Evergrande essentially borrowed twice for each development, first from a bank and then from the customer.

“They have always been very good at finding novel sources of financing,” says Nigel Stevenson, an analyst at Hong Kong-based GMT Research. Stevenson points especially to a deal in 2016, when Evergrande raised $20 billion from strategic investors with the promise of another backdoor listing in Shenzhen. If the company wasn’t public by 2021, Evergrande was required to pay the investors back. But after waiting years for government approval for the listing — and after documents were leaked showing Evergrande urgently requesting approval for the deal because of a cash crunch — they scrapped the plan. Even then, however, Xu managed to convince some investors, such as the retail conglomerate Suning Appliance Group and the state-owned firm Citic, not to collect on the debt.

“We thought the party had to end at some point,” says Stevenson. “But Xu managed to continue it far longer than we expected.”

Xu brought the party to other areas as well, diversifying over the years into what, on the surface, seem like wildly random sectors. In 2010, for instance, he bought Guangzhou Football Club, a soccer team; in 2013, he launched a bottled water company; in 2014, he went into cooking oils and grains; and in 2019, he made his publicly-listed healthcare subsidiary pivot to electric vehicles, despite the fact that the company never created a single car and Xu had zero experience in the industry.

“There was definitely some hubris there,” says Zhu. “Many of those moves didn’t pan out, but Xu is the richest guy in China, so he thought, ‘If I can be successful in property, I can be successful in those other things, too.’”

While some of these may have been vanity projects, others may have served a useful purpose for Xu and his pursuit of guanxi. Investments in soccer, for instance, took off after Xi Jinping, a known soccer fan, became president, but Xu Jiayin saw the potential earlier. “He was ahead of the game,” says Rowan Simons, an expert on Chinese soccer and head of China ClubFootball, an amateur soccer network in Beijing. By buying the Guangzhou Football Club, Simons says, “Xu was looking to build local government relations.” Government officials often suggest that wealthy business people invest in the local team, says Simons, or tycoons may offer it up as a gesture of their generosity.

Xu even parlayed his soccer team into a bonding experience with Jack Ma, convincing the tech mogul to buy a 50 percent stake in the team for $192 million in 2014.

“A few days ago in Hong Kong, by accident I got [Jack Ma] drunk,” Xu said at the time. “I told him my Evergrande soccer team is planning to issue shares and raise money to support strategic development, will you join? He said, ‘I will.’ We finished it in 15 minutes.”

Xu’s peers at the time were also diversifying at supersonic speeds, buying luxury hotels in New York or Middle Eastern energy assets, but Xu seemed to be acutely aware of the source — and limits — of his success. While the ‘Belt Brother’ was personally flashy about his wealth, he never forgot the requirement of staying in the good graces of China’s politicians, and he gave generously to social causes like poverty alleviation — one of Xi Jinping’s biggest priorities — way before that practice came into vogue with the recent ‘common prosperity’ campaign.

He was also particularly adept at paying lip service to the preeminence of the Chinese Communist Party. In 2018, for instance, the Ministry of Civil Affairs gave Xu the “China Charity Award” for his philanthropic work. In the Great Hall of the People in Beijing, he humbly proclaimed, “All I have and all that Evergrande Group has achieved were endowed by the Party, the state and the whole society.”

Perhaps better than anyone, Xu seemed to understand that anything the Party can give, it can also take away. Now, the question for Xu — who as of this week, according to Forbes, is estimated to be worth $11.9 billion — is precisely how much it will take away.

FRICTION AND FAVOR

The relationship between the Party and China’s business elite has always been one of utility. Entrepreneurs use politicians to get privileged access and then, in turn, pursue goals that the Party determines.

“The Party has always had a policy towards capitalists in the private economy — one that uses capitalists to strengthen the national economy and the role of the Party,” says Neil Thomas, an analyst at Eurasia Group who has written for this magazine about the historical example of Rong Yiren, a prominent Chinese businessman.

When Xu first started out in the late 1990s, the government needed help developing vast swaths of land, promoting urbanization, and providing a revenue source for local governments. Xu happily complied. But now, the government’s priorities have shifted. Logan Wright, a Hong Kong-based director for Rhodium Group, estimates that peak demand for housing was in 2014, and after that point, the government artificially inflated demand by pumping billions into urban redevelopment programs. But by around 2018, regulators, who were worried about property bubbles and hidden debt, began to scale back these programs.

The combination of government-driven demand and a growing reliance on pre-sales, says Wright, made the whole market more speculative in those four years. “And if you inject any sort of friction into that kind of model, you are going to have an issue,” he says. “The friction was the three red line policies in August of 2020.”

Beijing put in place the “three red line policies,” which set specific guidelines for how much debt property companies could carry, because it had become increasingly attuned to the systemic risks in the real estate sector. With real estate currently contributing close to 30 percent of the nation’s GDP, Beijing is determined to reduce the precarious sector’s footprint on the economy — all in the name of promoting sustainable, rather than runaway, economic growth.

“The government system is addicted to growth, but now there is a very concerted effort to shift away from high growth,” says Thomas. “They still want people to get rich through entrepreneurship, but you can see why Xi Jinping wants to get rid of a system where people like Xu Jiayin were using connections, speculation and debt to make personal fortunes.”

Thomas notes that the crackdown on property and speculation is different from the government’s crackdown on Jack Ma’s Ant Group IPO and internet companies, which moved too fast and spooked regulators by being too far out ahead. But both, Thomas says, are “about sending a signal about which areas of economic activity are no longer as favored.”

In favor, analysts note, is hard technology, such as semiconductors, and industries that require innovation, such as green energy. Chinese entrepreneurs are used to this type of sharp turn in government policy, says Rithmire, at Harvard Business School. “Business people in China have shorter time horizons,” she says. “Suddenly this is important, or that is important. So people are pretty savvy. These entrepreneurs are used to adapting and listening to the political winds domestically.”

Observers note that one of the ways Xu Jiayin tried to ensure he wouldn’t fall over from each and every changing wind was to be “too big to fail.” Over the course of his quarter-century career, “going big and bigger was Xu’s top operating principle,” says HKU’s Chen.

But according to Rithmire, there’s one problem with this strategy: “How do you grow big in China? You protect yourself by connecting yourself to political elites. In return, you pursue the goals that the state wants. But once you get really big, who controls who?”

Xi Jinping has made it clear that the Chinese government will never have its hands tied by private business. Starting with the anti-corruption drive in 2013 and intensifying again this year with various corruption dragnets and takedowns of business leaders, he has been reasserting the CCP’s control over the corporate sector and — in the process — systematically dismantling the guanxi networks that Xu leans on. While Xi’s motive in all this could be as simple as eliminating rivals and consolidating his own power, he is known to detest the kind of chummy relationships Xu has spent his life cultivating.

How do you grow big in China? You protect yourself by connecting yourself to political elites. In return, you pursue the goals that the state wants. But once you get really big, who controls who?

Meg Rithmire, a professor at Harvard Business School

“Xi’s campaign has successfully struck fear into corrupt officials,” says University of Michigan’s Ang. “But it will not remove the root causes of graft — namely, the enormous power of the government over the economy and the patronage system in the bureaucracy.”

Rithmire agrees, saying that in the absence of durable reform — such as more transparency from regulators and the media and the Party subjecting itself to the rule of law — the pattern of “cozy relationships between business leaders and politicians, and then crackdowns” will just keep repeating itself in China, “like a dance.”

Now 63 years old — he celebrated his birthday earlier this month — Xu Jiayin has seen for himself the ebbs and flows of this pattern. Although it’s unclear what will happen to Xu now that his company is in free fall, he has outlasted many of his peers.

“A lot of the other property developers who got in in the ’80s and ’90s have quit, are in jail, or have died. But not Xu,” says UCSD’s Shih. “He built the type of connections he needed to keep his company growing.”

Evergrande is no longer growing — the company halted trading in Hong Kong last week and the company is reportedly in restructuring talks — but Xu shows no signs of quitting. Publicly, he has vowed to settle all of Evergrande’s debts and continues to tow the CCP-line: “My colleagues,” he wrote in his September letter, “let’s unite and demonstrate courage in the face of a hundred adversities, and a tough, solid spirit. Let us fulfill with all our strength the responsibility we have to our society, and build a better future together!”

Privately, however, the master player may have shown his cards. Together with his wife, Xu controls 77 percent of Evergrande shares. In 2020 alone — as Evergrande’s debts mounted — he paid himself $239 million in stock dividends, according to Forbes calculations. Many of his assets — which include a $90 million jet that can seat up to 160 people — are owned through shell companies outside of China and Hong Kong, as exposed by the Panama Papers.

“He will likely keep some of his personal wealth offshore,” says Chen. “And his descendents will enjoy those accounts.”

Perhaps his family will even be invited back for China’s next dance with private entrepreneurs.

Katrina Northrop is a journalist based in Washington D.C. Her work has been published in The New York Times, The Atlantic, The Providence Journal, and SupChina. @NorthropKatrina

{kind=link}