China’s factories have been at the heart of the country’s economic rise, helping the country come to account for nearly a third of global manufacturing and providing millions of jobs in the process.

Increasingly, though, robots are taking over.

By the end of last year, Chinese manufacturers had deployed 470 robot units per 10,000 workers, some three times the global average, new data from the International Federation of Robotics revealed last month. And while a decade ago China was a global laggard in terms of robot adoption, it has now surpassed Germany and Japan to rank third behind only Singapore and South Korea, the figures show.

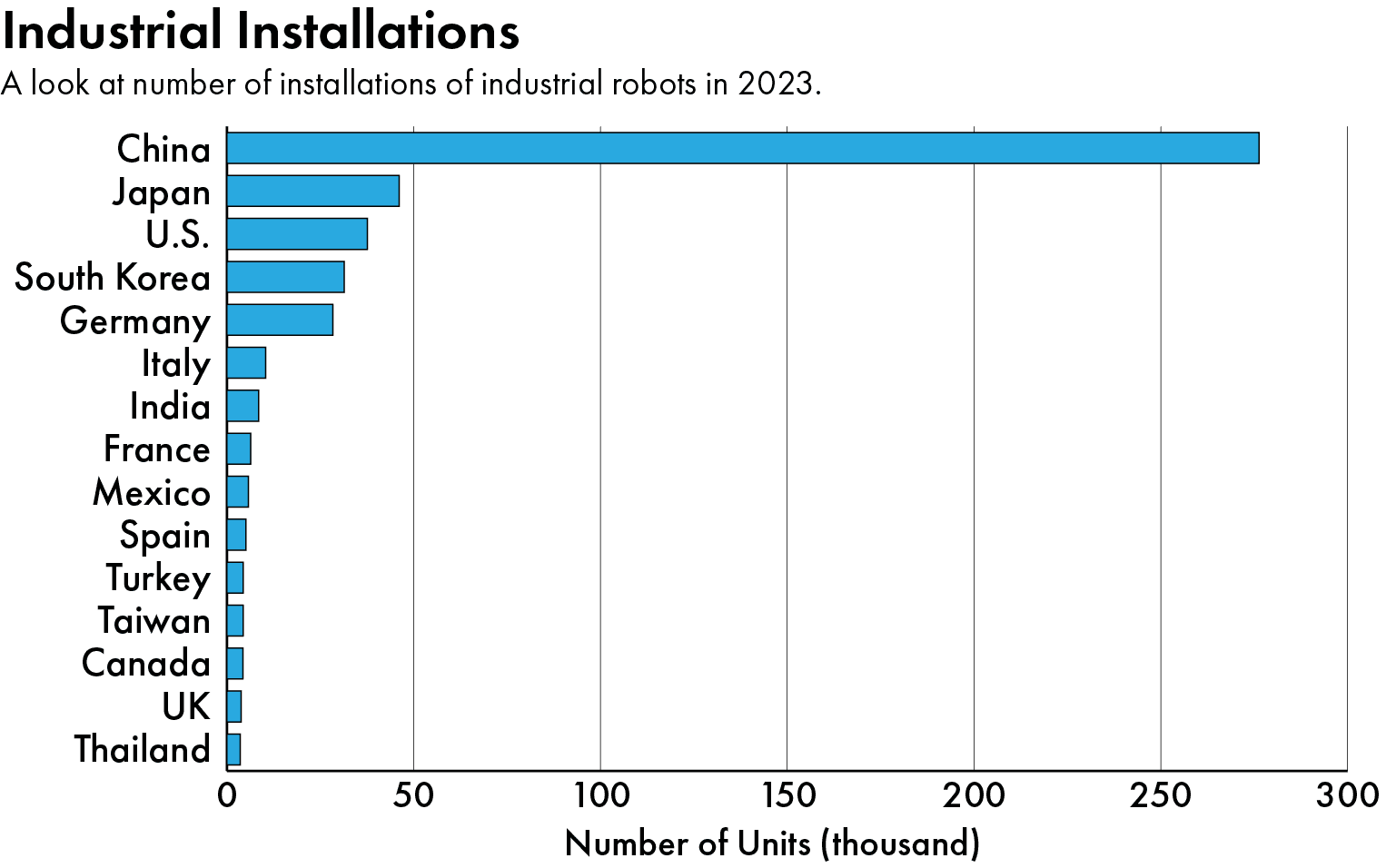

Industries from electronics and automobiles to chemicals and food processing have rushed to install robots as China’s population shrinks and labor shortages loom. The country has now been the world’s largest market for industrial robots for over a decade, dwarfing other national markets, the IFR data shows.

And though Chinese buyers once relied on foreign robot suppliers such as Japan’s Fanuc and Yaskawa, factories in China are increasingly deploying less advanced but cheaper homegrown models, as part of the country’s self-sufficiency drive led by Xi Jinping.

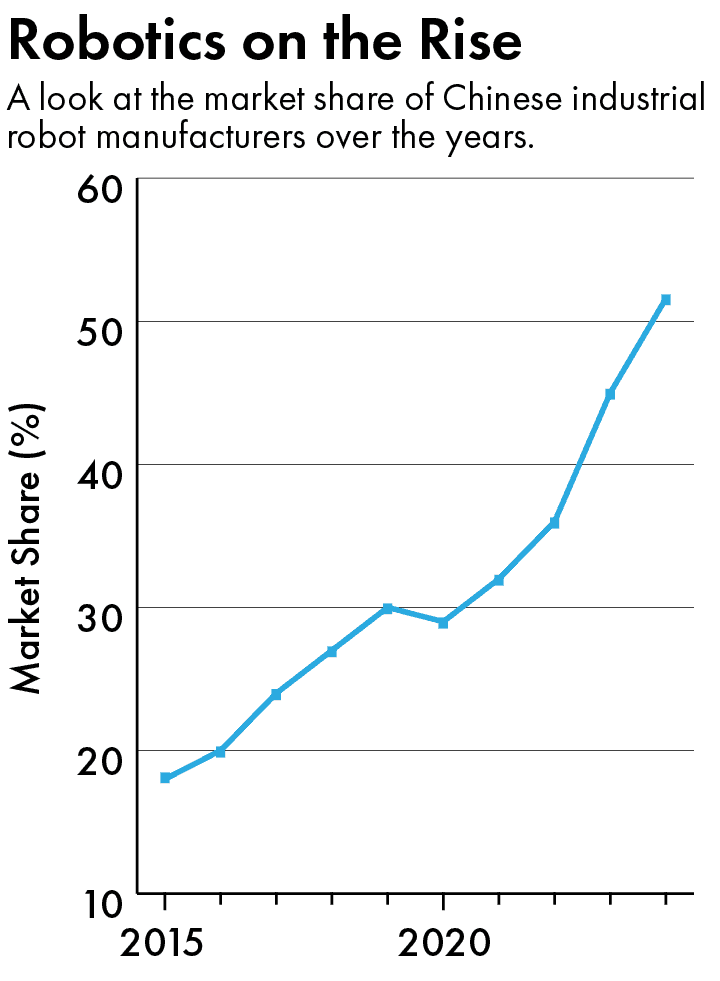

According to research firm MIR Databank, for the first three quarters of this year, domestic companies such as Shenzhen-based Inovance and Estun from Nanjing together sold more units in China than their foreign counterparts for the first time.

Leading Chinese robot suppliers are now setting their sights overseas, a factor some believe could shake up the global market.

“Chinese firms will change robotics in Europe and the U.S.,” says Georg Stieler, head of Robotics & Automation at Stieler Technology & Marketing Consulting. “Their aggressive pricing will bring more competition and force established players to rethink some of the ways they have been doing business.”

Beijing first set a goal for homegrown robot makers to take more than half of the domestic market in its Made in China 2025 plan, the ambitious industrial policy it unveiled a decade ago. The central and local governments have since been pumping money in to support Chinese manufacturers.

In January, the Beijing government set up a 10 billion yuan ($1.38 billion) fund alongside a subsidiary of Shougang Group, a state-owned steel enterprise, to give the robotics industry a boost. Siasun, one of China’s largest robotic manufacturers, has received 588 million yuan ($80.9 million) in subsidies in the last three years, according to its annual report.

Estun’s ER120 robot at work on a door panel paint and siding production line. Credit: Estun Automation

Some Chinese companies have also snapped up long-established foreign businesses with key technologies over the last decade. Estun, another leading Chinese robot manufacturer, purchased Germany’s Carl Cloos Welding Technology for $216 million in 2019 and took stakes in Barrett, a U.S. company and a pioneer in robotic arms in 2017. Inovance, which has emerged as a leader in SCARA robots (a popular type of robots that perform similar motions to a human arm), acquired the French software company Irai for an undisclosed sum this July.

The best-known example is Chinese electronics giant Midea’s $5 billion takeover of Germany’s Kuka — known as one of the industry’s Big Four, alongside Switzerland’s ABB as well as Japan’s Fanuc and Yaskawa — which went ahead in 2016 in the face of a political backlash in Europe.

Robotics firms in China benefit from the ecosystem that evolved here during the last 10 to 15 years. They can make product iterations much faster and at considerably lower costs than [firms] in Japan, not to speak of Europe.

Georg Stieler, head of Robotics & Automation at Stieler Technology & Marketing Consulting

Despite these acquisitions, Chinese players’ share of the domestic industrial robotics market had hovered under 30 percent until recently. The pandemic provided them with a window of opportunity. During that period some Chinese factories turned to local robotic companies, as foreign manufacturers suffered supply chain disruptions that led to longer delivery times, says Wang Feili, a China industrials analyst at UBS Securities, adding that the quality of domestic robots has steadily improved.

Chinese industrial robotic companies have also ridden on the booming growth of industries such as lithium batteries and solar panels. Unlike industries such as auto and chip making, these sectors do not require very sophisticated robots and their needs match with what Chinese suppliers have to offer, Wang says.

“Robotics firms in China benefit from the ecosystem that evolved here during the last 10 to 15 years. They can make product iterations much faster and at considerably lower costs than [firms] in Japan, not to speak of Europe,” says Stieler. “What amazes me still is the speed at which this happened.”

While the Chinese authorities have not issued a strict order for state-owned companies to phase out foreign robot suppliers, as they have done in other industries such as chips and software, analysts say Chinese state-owned factories have pivoted to local suppliers all the same.

It helps that Chinese robots are 10 to 15 percent cheaper than comparable models from foreign brands, due to their localized supply chain, according to estimates from HSBC Qianhai Securities.

To meet the growing demand, Efort, a company known for its paint-spraying robots, announced plans to build a 1.9 billion renminbi ($261 million) factory at its headquarters in Wuhu, Anhui province, in August. The company says the plant will focus on high-end and specialized robots, and increase its annual output tenfold to 100,000 units by 2029.

Some of those units may well end up in factories outside of China, as Efort and other Chinese robotics companies step up their expansion abroad.

“Like any business looking for a new market, Chinese robot companies go where there is demand for their products,” said Xiaogang Song, executive director of the China Robot Industry Alliance recently. He estimates that only 5 percent of Chinese robots are currently exported.

Cédric Pujols from Inovance Technology Europe presents a SCARA robot during SPS 2024, held in November. Credit: Inovance

But many companies have plans which could lead that figure to rise. Inovance launched its SCARA robots in Europe at a trade show in Germany last month. The company, which has sales and engineering offices across the region, hopes to increase its overseas sales from 6 percent of its total now to up to 30 percent eventually. Chinese companies building plants overseas gives Inovance an opportunity to tag along, Song Junen, an executive said at an earnings call in April.

Estun, which launched in Europe in October, is now aiming for up to 10 percent of the European market, its regional chief executive officer Gerald Mies said in an interview last month.

ABB Robots work at a factory belonging to Chinese car manufacturer BAIC. Credit: ABB Robotics

“We expect to see further competitors arriving in the global market from China,” an ABB spokesperson told The Wire China, adding that it is confident in its “local for local” strategy to support and serve local customers.

To compete with global market leaders such as ABB, Chinese companies must overcome challenges from innovation and software development to brand recognition. Foreign industrial robots remain known for better precision and reliability, and longer life cycles, for example.

“It takes time to close the gap in key metrics,” says Ni Tao, a Shanghai-based tech blogger. “The adoption of Chinese industrial robots is mainly concentrated in the low-to-mid-end segments, while rivals like Fanuc and ABB still dominate the premium sectors.”

All these are very new technologies that can only be achieved if you are part of a wider, global tech ecosystem and have the willingness to be open and collaborate.

Lian Jye Su, chief analyst at tech research firm Omdia

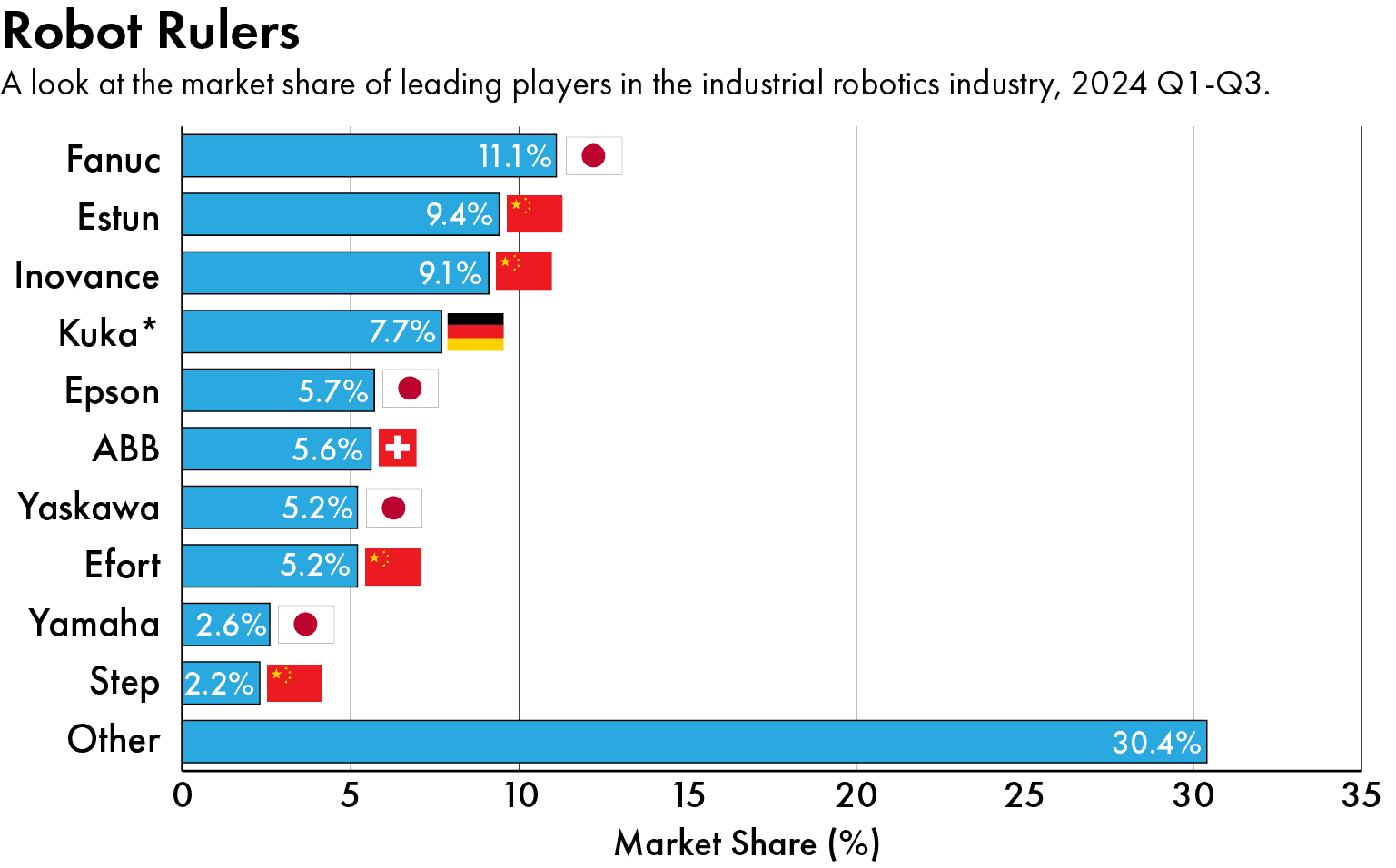

As a result, Chinese companies still lag behind in terms of revenue. Even though Estun was second to Japan’s Fanuc in market share by unit sales in China last year, it only recorded $640 million in sales, less than half of Fanuc’s $1.61 billion.

Moreover, German and Japanese companies still maintain a lead in some essential components, such as the drive systems that feed electricity to robots, says Lian Jye Su, chief analyst at tech research firm Omdia.

In the long run, Chinese players will have to find a way to differentiate their products or they risk getting dragged deeper into a price war as competition intensifies, says Walter Zhu, head of robotics at MIR Databank. “This is not an industry where you can keep gaining market share just by cutting prices.”

Another weakness is in software. China’s push has mostly been hardware-centric, but analysts say the next robotic revolution will come from the integration of cutting-edge technologies such as AI into machines, a step that has the potential to transform manufacturing processes.

“All these are very new technologies that can only be achieved if you are part of a wider, global tech ecosystem and have the willingness to be open and collaborate,” says Su, of Omdia. “It takes time, investment, and the ability to see something far beyond just installing a piece of hardware onto a factory floor.”

Rachel Cheung is a staff writer for The Wire China based in Hong Kong. She previously worked at VICE World News and South China Morning Post, where she won a SOPA Award for Excellence in Arts and Culture Reporting. Her work has appeared in The Washington Post, Los Angeles Times, Columbia Journalism Review and The Atlantic, among other outlets.