Continents collided on the Arabian Gulf on Thursday as China sold sovereign bonds denominated in U.S. dollars for the first time in three years — in Saudi Arabia.

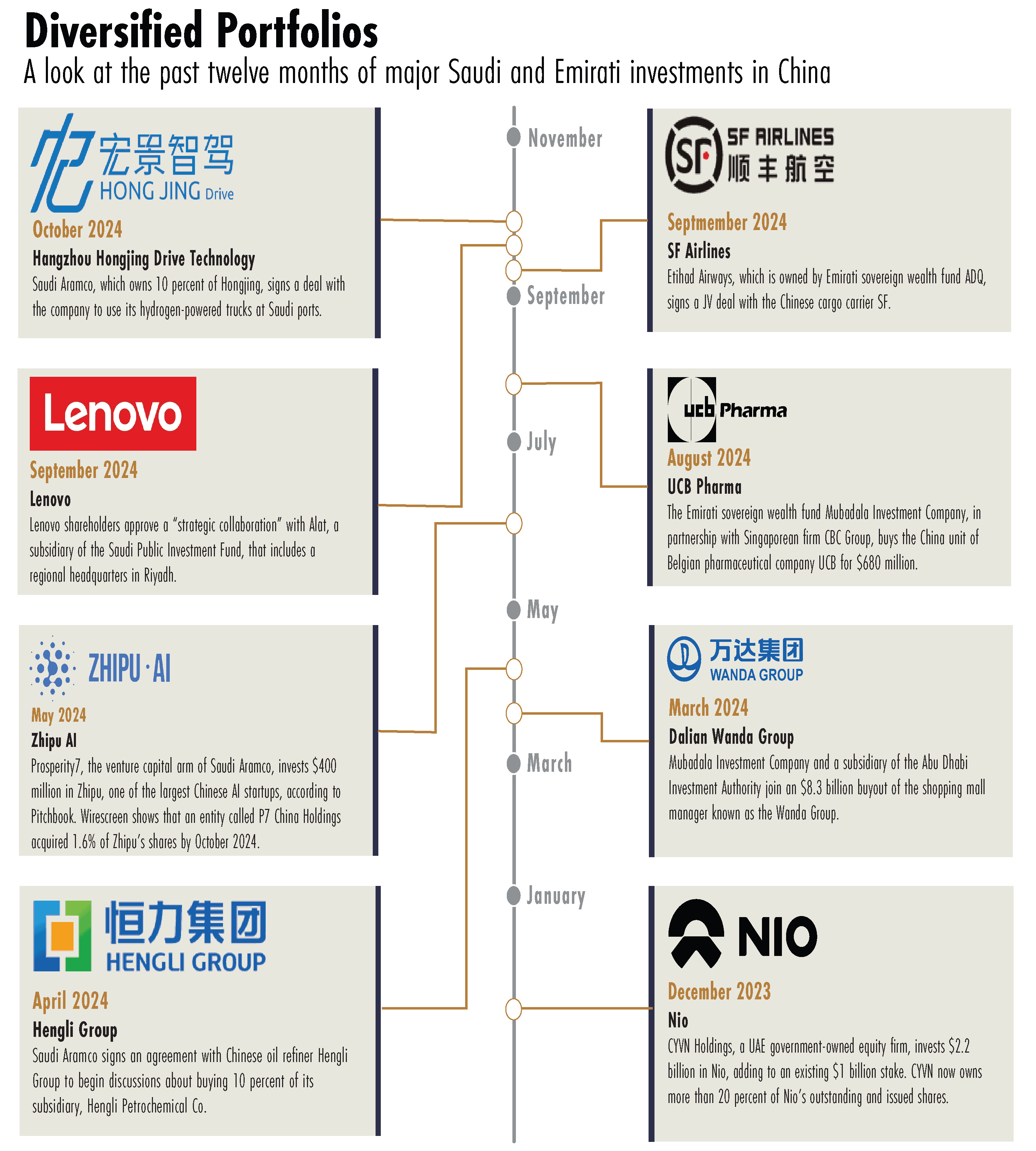

At $2 billion, the bond sale is too small to provide a serious boost to China’s foreign exchange coffers. But it does act as icing on the cake of investments that Saudi Arabia has poured into China over the past 12 months, many of which are distinct from the oil purchases that have long underpinned the two countries’ relations.

“There’s a general consensus on both sides that this is a very important relationship, but that it is in search of growth areas,” says Robert Mogielnicki, a senior resident scholar at the Arab Gulf States Institute in Washington who studies Chinese-Gulf ties.

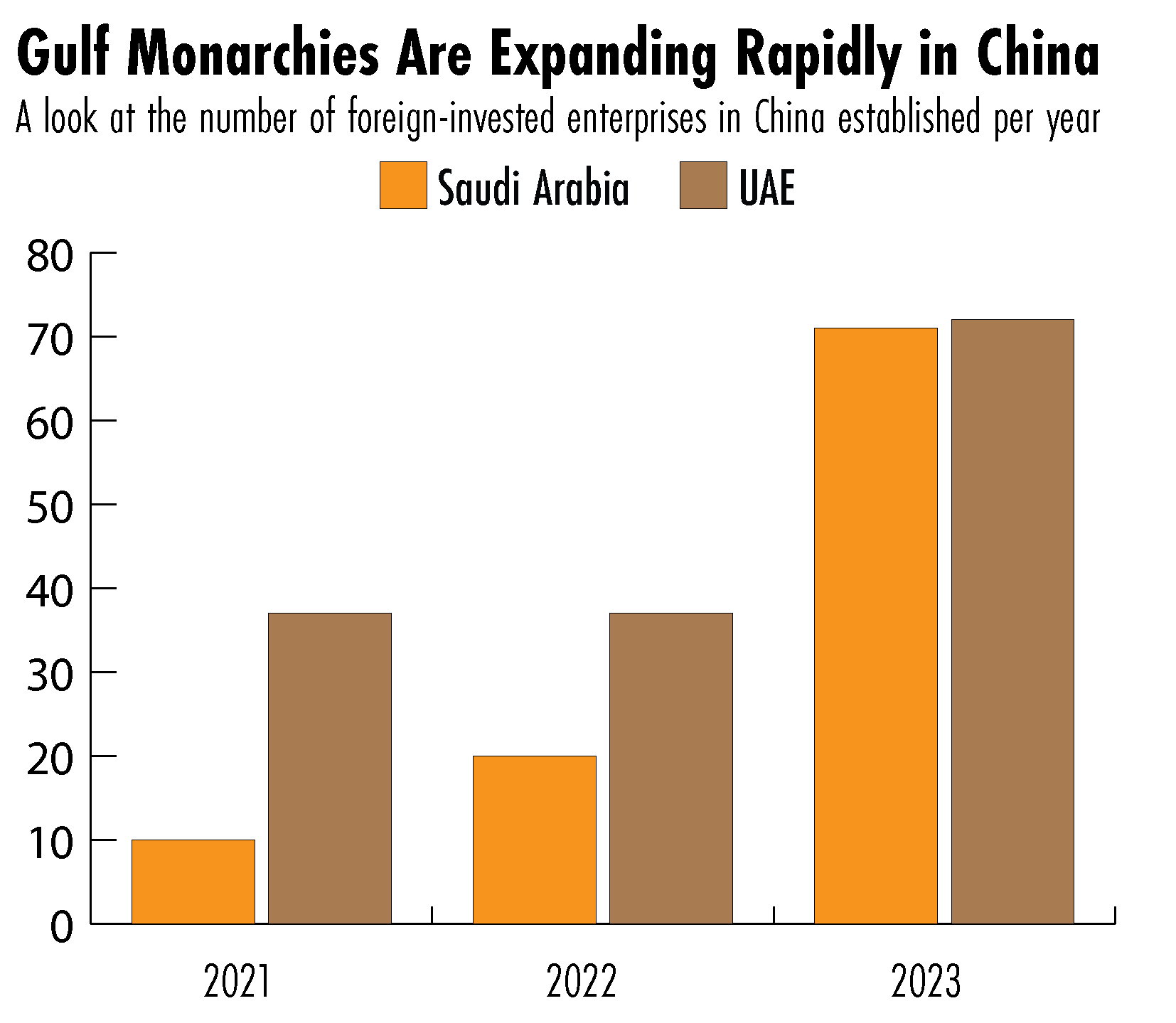

Companies in the Gulf have taken note. Saudi Arabia launched three times as many foreign-invested enterprises (FIEs) in China last year as the year prior, according to the Chinese Ministry of Commerce’s latest statistical bulletin, published in September. The United Arab Emirates launched nearly double its 2022 total.

Many deals have been concentrated in finance and technology. In May, the Saudi Public Investment Fund announced that it had signed up to $50 billion worth of agreements with six state-owned Chinese banks; less than a month later, a subsidiary of the sovereign wealth fund committed to buying $2 billion worth of bonds from Beijing-based electronics firm Lenovo, which agreed to set up a manufacturing base in Riyadh.

The Gulf is really trying to find its footing in a brave new world… if the U.S. doesn’t offer the bare minimum in terms of access to technologies, then the Gulf will have to diversify and build new types of relationships.

Mohammed Alsudairi, a lecturer on China and the Middle East at Australian National University

The UAE has also stepped up its non-energy cooperation with China this year. Last December, a fund owned by the government of Abu Dhabi invested $2.2 billion in Nio, the Shanghai-based electric vehicles manufacturer that is developing autonomous cars. A month ago, Nio announced it would pick the UAE as its first regional market and open a research and development center in Abu Dhabi.

Chinese officials have actively encouraged these trends. Visiting Saudi Arabia and the UAE in September, China’s premier Li Qiang exhorted Saudi companies to invest in China, particularly in the tech sector. He also said he would work to boost China-UAE investment.

Premier Li Qiang meets with Saudi Crown Prince Mohammed bin Salman. Credit: CCTV

“Chinese government actors and businesses are seeking to court Gulf capital, but Gulf governments are actually seeking to court Chinese money,” says Mohammed Alsudairi, a lecturer on China and the Middle East at Australian National University.

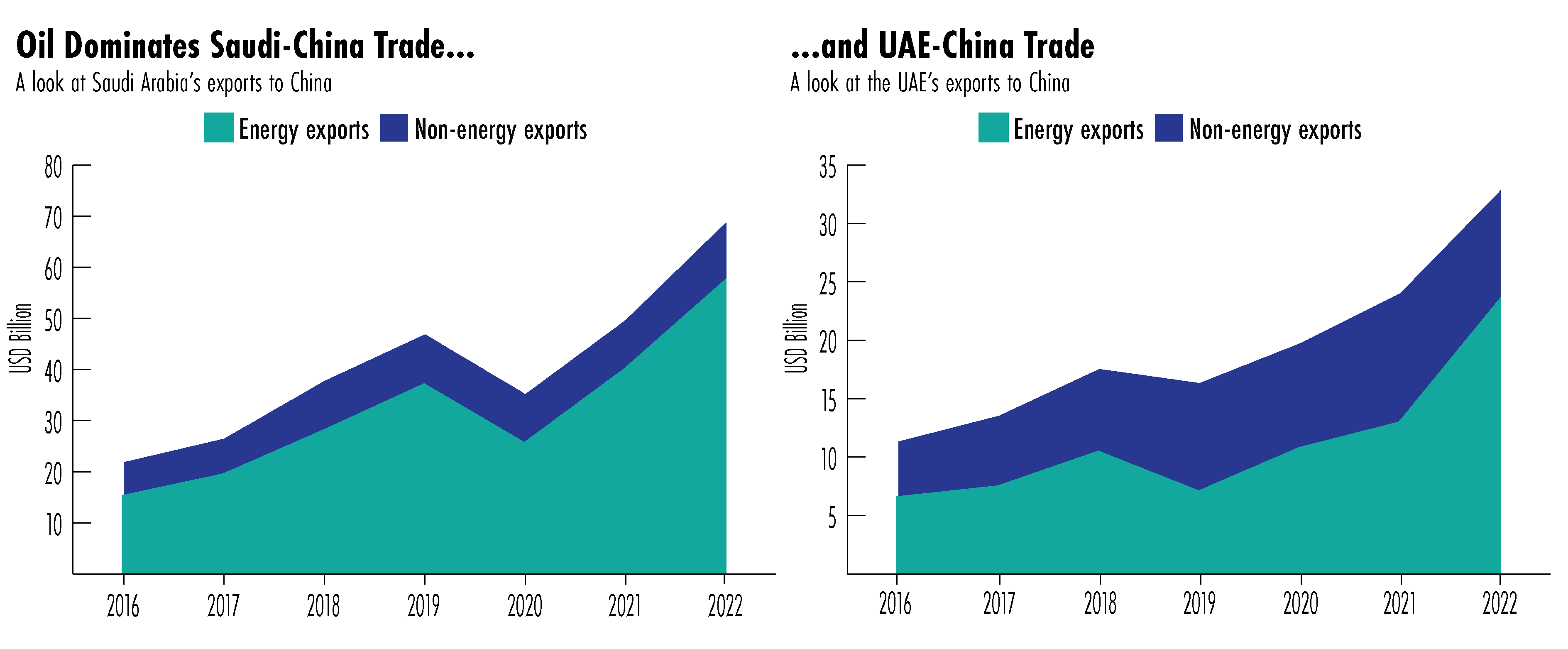

Indeed, energy exports from Saudi Arabia — and the UAE — to China are surging. Overall exports to China from each country have tripled since 2016.

The relationship is mutually beneficial. The Gulf states lack many indigenous tech companies capable of building the “cities of the future” touted by their respective leaders, and Chinese businesses are eager for expansion into wealthy foreign markets — especially as domestic demand slows, internal competition heats up, and Europe and the United States crack down on Chinese autonomous vehicles and other tech firms.

However, structural challenges, including capital controls and a lack of familiarity with the Chinese market, could prevent Gulf investors from seeing China as a more desirable market than the United States, currently the destination of choice for Gulf money.

In high-tech arenas, competition between Washington and Beijing could also get in the way of dealmaking. Earlier this year, Emirati artificial intelligence company G42 divested from Chinese firms before accepting $1.5 billion in backing from Microsoft.

“The Gulf is really trying to find its footing in a brave new world, and they would rather be within the U.S. orbit,” Alsudairi says. “But if the U.S. doesn’t offer the bare minimum in terms of access to technologies, then the Gulf will have to diversify and build new types of relationships.”

Noah Berman is a staff writer for The Wire based in New York. He previously wrote about economics and technology at the Council on Foreign Relations. His work has appeared in the Boston Globe and PBS News. He graduated from Georgetown University.