In a call that lasted just three minutes this August, executives at tech giant IBM told employees it was shutting its research and development operations in China — closing two labs and cutting more than 1,000 jobs.

“It’s the end of an era,” an IT specialist who had spent 18 years at the company wrote on the social media platform Xiaohongshu in late October.

The layoffs at IBM, which first entered China in 1984, are part of a wider trend of multinationals across sectors pulling back from the Chinese market, once viewed as indispensable for any successful international business. Many of them have been in the country for decades.

Last month, Finnish telecoms company Nokia cut 2,000 jobs in China, a fifth of its local workforce; the same week, UK-headquartered financial firm Fidelity International dismissed 500 of its China employees. U.S. law firm WilmerHale said it is winding down its Beijing office last month too, joining over a dozen American law firms in retreat since last year. Consultancy McKinsey has trimmed its China workforce by a third over the past year and is hiving off the unit, The Wall Street Journal reported last month.

Xi Jinping addresses national security during the 20th National Congress of the Communist Party of China, October 16, 2022. Credit: CCTV

Foreign companies face unprecedented challenges as Beijing has prioritized national security over economic growth, tightened its grip on the business hub of Hong Kong and unleashed an apparently never-ending crackdown on the private sector. Late last month, the China president of British-Swedish pharmaceutical giant AstraZeneca was placed under investigation with few details as to why — typifying a lack of transparency that has shaken the business community’s confidence. AstraZeneca declined to comment.

Multinationals’ operations in China are also under scrutiny at home. Companies such as German auto giant Volkswagen have faced public criticism for producing in Xinjiang, where China’s government stands accused of cultural genocide. Others, such as Calvin Klein’s American brand owner PVH Corp, face penalties from Beijing as they seek to comply with U.S. laws against using forced labor.

Above all, foreign firms’ profits have suffered as competition intensifies from domestic rivals, even as demand falters amid China’s economic slump.

As a result, a growing number of companies have reached “a tipping point,” where the challenges of doing business in China are starting to outweigh returns, said Jens Eskelund, head of the EU Chamber of Commerce in China in September.

“If you have all these issues with market access, red tape, geopolitical tension, and supply chain concerns; and on top of that, you’re not making as much money in China as you are outside, the question becomes, why China?” he told The Wire China in an interview.

More than two thirds of the respondents to the chamber’s annual survey this year said doing business in China has become more difficult, marking an all time high. Pessimism about future profitability and growth also rose sharply.

The optimism you had among Chinese business people is not bouncing back. The role that private entrepreneurs in China were playing has shifted and China is now more focused on state-owned enterprises.

Joerg Wuttke, a former president of the EU Chamber of Commerce in China and now a partner at DGA-Albright Stonebridge Group

Their American counterparts share such sentiments. For sure, two-thirds of the respondents to The American Chamber of Commerce in Shanghai’s annual survey still said they were profitable in China last year: but that is a historic low since the survey began 25 years ago. The proportion of companies who see China as their top global investment destination sank to a record low of 13 percent.

Hard data reinforces the picture. Net foreign direct investment into China dipped to $42.7 billion in 2023, the lowest level since 2001, according to the State Administration of Foreign Exchange. In the second quarter of this year, a record balance of $15 billion flowed out.

The following chart shows how FDI into China has developed over the years along with some of the major milestones along the way.

Images: Volkswagen AG, Shanghai Stock Exchange, WTO, Kris Krüg via Wikimedia Commons, Andy Wong via AP Images. Design: Hiram Henriquez.

Even if companies are not heading for the exit, they are hesitant to make additional investments, says Michael Hart, president of The American Chamber of Commerce in China. “The political environment in the U.S. makes it difficult for companies to talk about expansion in China.”

The bleak outlook is a far cry from the optimism that abounded at the turn of the century, as China joined the World Trade Organization in 2001. That positivity lingered as multinationals rode on China’s stimulus efforts after the global financial crisis.

A realization has set in that China’s high-growth era is over and few see an imminent turnaround. “Not too long ago, there was the perception that, despite hiccups and ups and downs, there would still be growing opportunities in the Chinese market,” says Dexter Roberts, a senior fellow at the Atlantic Council. “That changed within the last five years.”

The game changer was the COVID pandemic, says Joerg Wuttke, a former president of the EU Chamber of Commerce in China and now a partner at DGA-Albright Stonebridge Group.

“The optimism you had among Chinese business people is not bouncing back,” he says. “The role that private entrepreneurs in China were playing has shifted and China is now more focused on state-owned enterprises.”

There are still many reasons to be in China. The world’s second largest economy is projected to grow at an average annual rate of 3.3 percent through 2029, according to the International Monetary Fund — still higher than the 3.1 percent average global growth forecast over that period.

Another 80 million people could join China’s middle class ranks by the end of the decade, the Boston Consulting Group estimates. Once the world’s factory, China has also emerged as an innovation powerhouse in areas from pharmaceuticals to artificial intelligence. “The key reason [to stay in China] these days is that [multinationals] believe their next global competitor is coming out of China,” says James McGregor, chairman of consultancy APCO’s greater China region, adding that a presence in the country allows them to monitor developments or partner with local companies.

But the question of whether to stay or go is no longer a given.

“China is for many, but not for all,” Eskelund says. “That’s where companies need to do their homework and see whether they have a product portfolio, a price point, and an infrastructure that is a good fit with what China offers.”

Changing Calculations — a Sector by Sector Review

Ever since China started opening up in the late 1970s, there has been an understanding that China would invite in foreign companies when it needed them.

In some areas — notably social media — the Chinese authorities have never seen much need for outsiders. Google gave up on China in 2010; Facebook has never been accepted, although it makes money from Chinese advertising. China’s Great Firewall keeps out other foreign media giants, from X to Netflix.

What those allowed in may not have appreciated is that their period of outsized profits in China might prove finite.

“China has produced companies that can substitute foreign importers or foreign players. And so China has evolved from the market to a competitor for many foreign companies,” Wuttke says.

The issue now is that Chinese companies are not just catching up with, but leapfrogging foreign companies. A sector by sector review shows where Eskelund’s ‘tipping point’ may now have arrived — and those where optimism still exists.

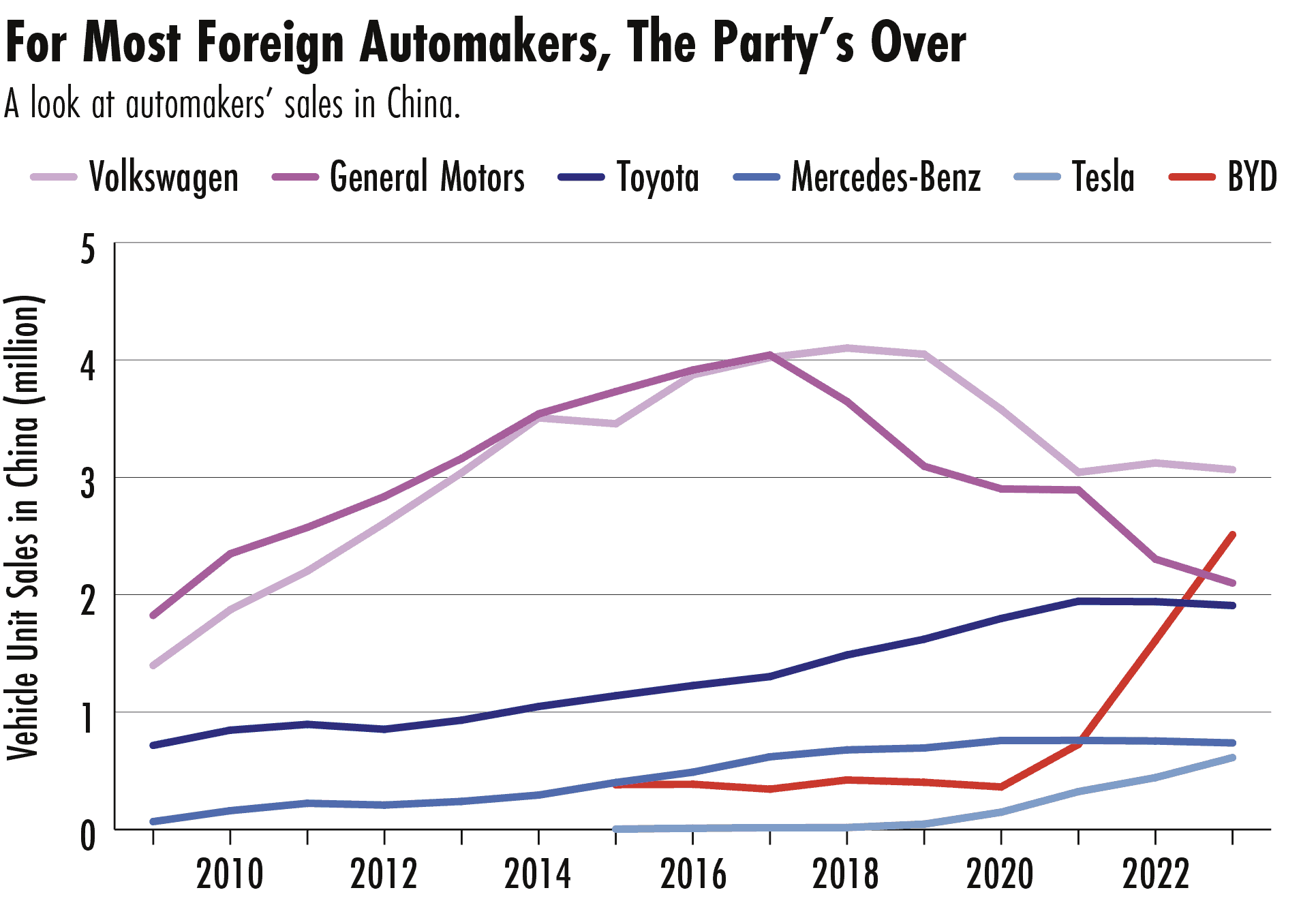

Autos

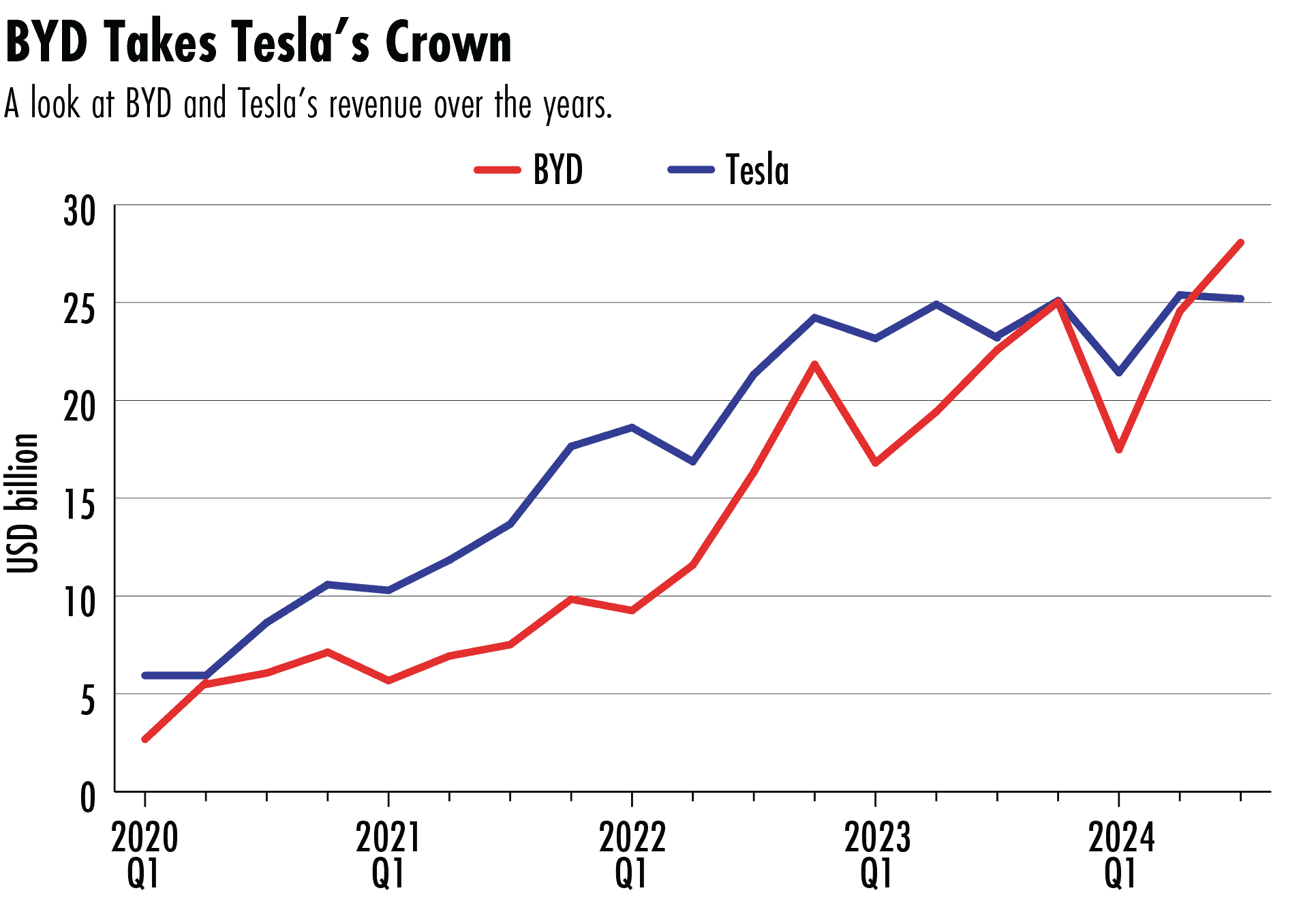

Automaking is the most high profile industry where the balance has tipped towards Chinese companies. Foreign carmakers such as the U.S.’s General Motors and Japan’s Toyota have seen their sales in China plummet, as the likes of BYD soared past them amid China’s transition to electric vehicles.

Chinese EV makers’ success is often put down to robust state support, as well as their cost advantages. But Elon Musk’s Tesla has played no small part.

The U.S. carmaker helped build an EV supply chain in China when it opened its first factory in Shanghai in 2019 and switched to Chinese-made parts. And though the Chinese market only accounted for one-fifth of Tesla’s total revenue last year, its Shanghai gigafactory now produces half of its global output.

The question is whether Tesla can stay ahead. In the third quarter of this year, BYD’s revenue toppled Tesla’s for the first time. Tesla did not respond to requests for comment.

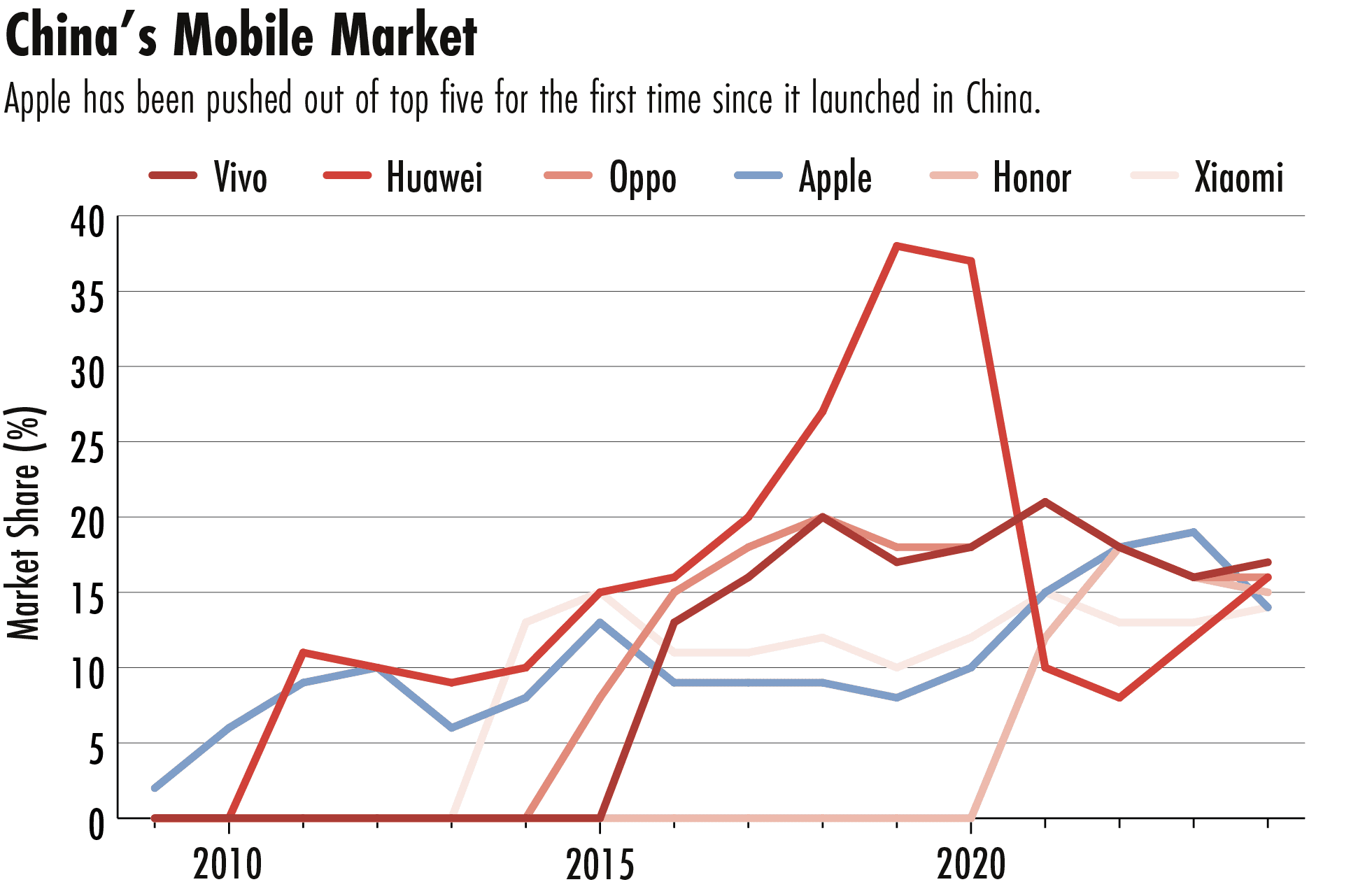

Mobile Phones

A non-Chinese company can only survive in China’s cutthroat market if it has a prestigious brand, advanced technology, a vast consumer user base or a superior supply chain, says Lele Sang, a fellow at the University of Pennsylvania’s Wharton School and author of Winning in China.

For a long time, Apple’s iPhone ticked all the boxes. But it now faces a growing number of domestic rivals that churn out sleeker models with flashier features, such as Huawei’s latest tri-fold phones. In the first half of this year, Apple fell out of the top 5 smartphone vendors in China by unit sales, for the first time since it started selling in China — although it still retains a 14 percent market share.

Apple’s prospects could hinge on the deployment of its new AI tools to enhance users’ experience. “The timeline for the introduction of Apple Intelligence in mainland China remains uncertain and depends on Apple’s ability to meet local legal and regulatory requirements,” says Le Xuan Chiew, an analyst with the research firm Canalys. It’s little wonder that Apple chief executive Tim Cook has twice traveled to China this year to meet with regulators there. Apple did not respond to requests for comment.

Semiconductors

Foreign companies have long held a technological lead over Chinese rivals in semiconductors. U.S. firm Qualcomm’s portion of revenue from China grew from single digits to 62 percent over two decades as local demand for gadgets powered by chips soared.

But as tensions between China and the U.S. simmered, some chipmakers are now downplaying their China links.

Take Idaho-based Micron, which specializes in memory chips. Prior to 2019, it disclosed its revenue by geographic region based on where it was shipping its products.

Since then, it has switched to recording sales based on company headquarters: so a sale to an American fab in China now counts as U.S. revenue. The new methodology has brought the China share of Micron’s global revenue down from over half in 2017 to 12 percent in the fiscal year ended August 2024.

U.S. chipmakers such as Micron and Intel are anyway being squeezed by both sides. The Biden administration has banned companies from selling advanced chips to China since 2022; meanwhile, their sales of mature nodes for items like TVs have languished due to China’s self-sufficiency drive. Micron did not respond to requests for comment.

Note: The final revenue figures for Intel, Qualcomm, and Broadcom are based on 2023 data. Source: Annual reports, company filings

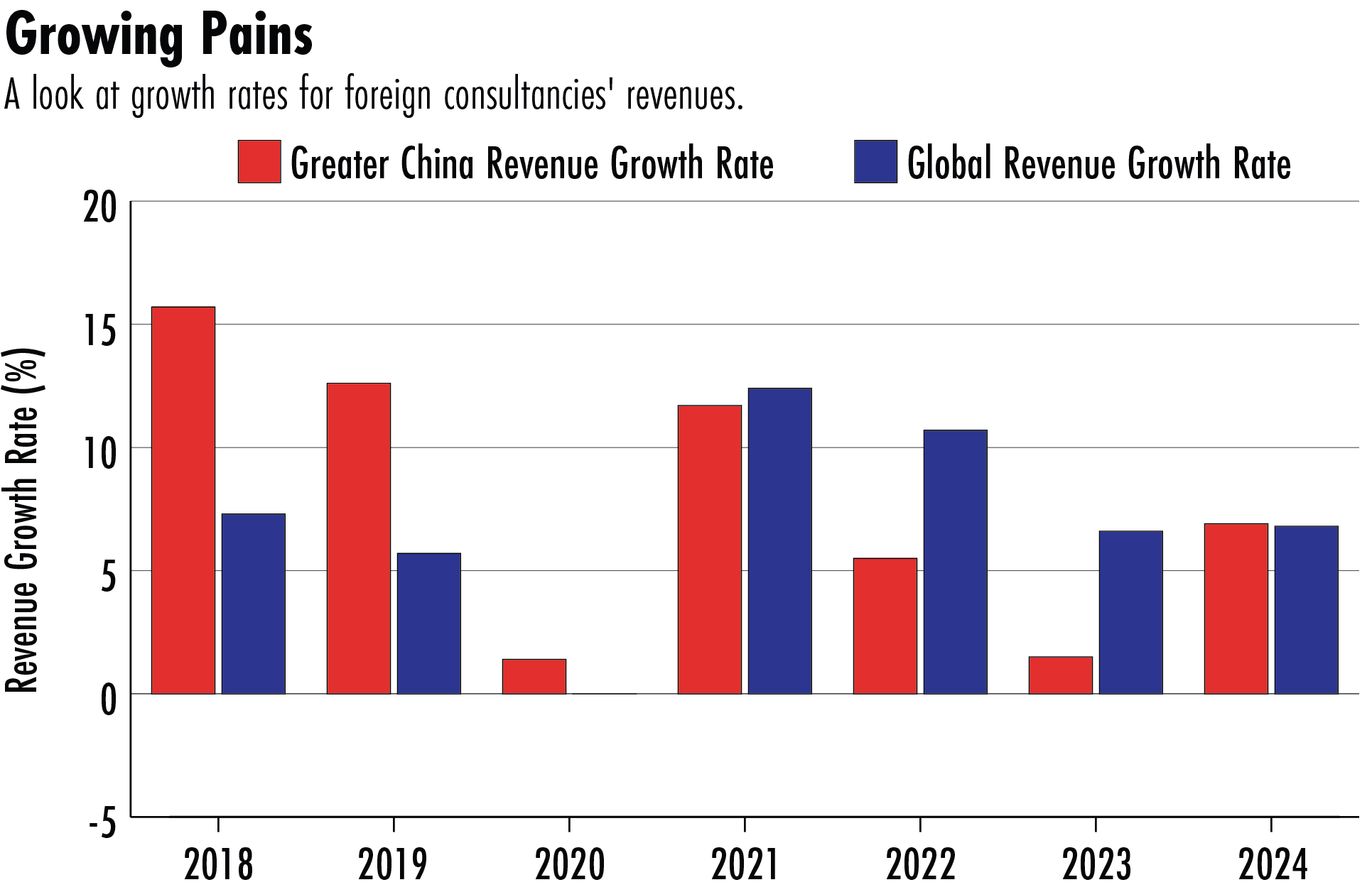

Professional Services

A series of regulatory clampdowns has hit the professional services sector in China. Chinese authorities raided the offices of American consultancies Bain and Capvision last year, and slapped a $2.2 million fine on U.S. due diligence firm Mintz. In September, Chinese regulators punished the accounting firm PwC for its alleged role in covering up fraud at Chinese property giant Evergrande with a record $62 million penalty and a six-month suspension.

Today, there are only a few sectors where multinationals still hold an absolute advantage in either technology, innovation or product experience.

Jason Yu, managing director at CTR Market Research

Analysts suggest firms are shifting their focus. “I don’t see consultancies investing as much in China,” says Tom Rodenhauser, a managing partner at Kennedy Intelligence, which advises the consulting industry. “The growth rates that we see for consulting are actually dipping in China relative to the rest of the market.”

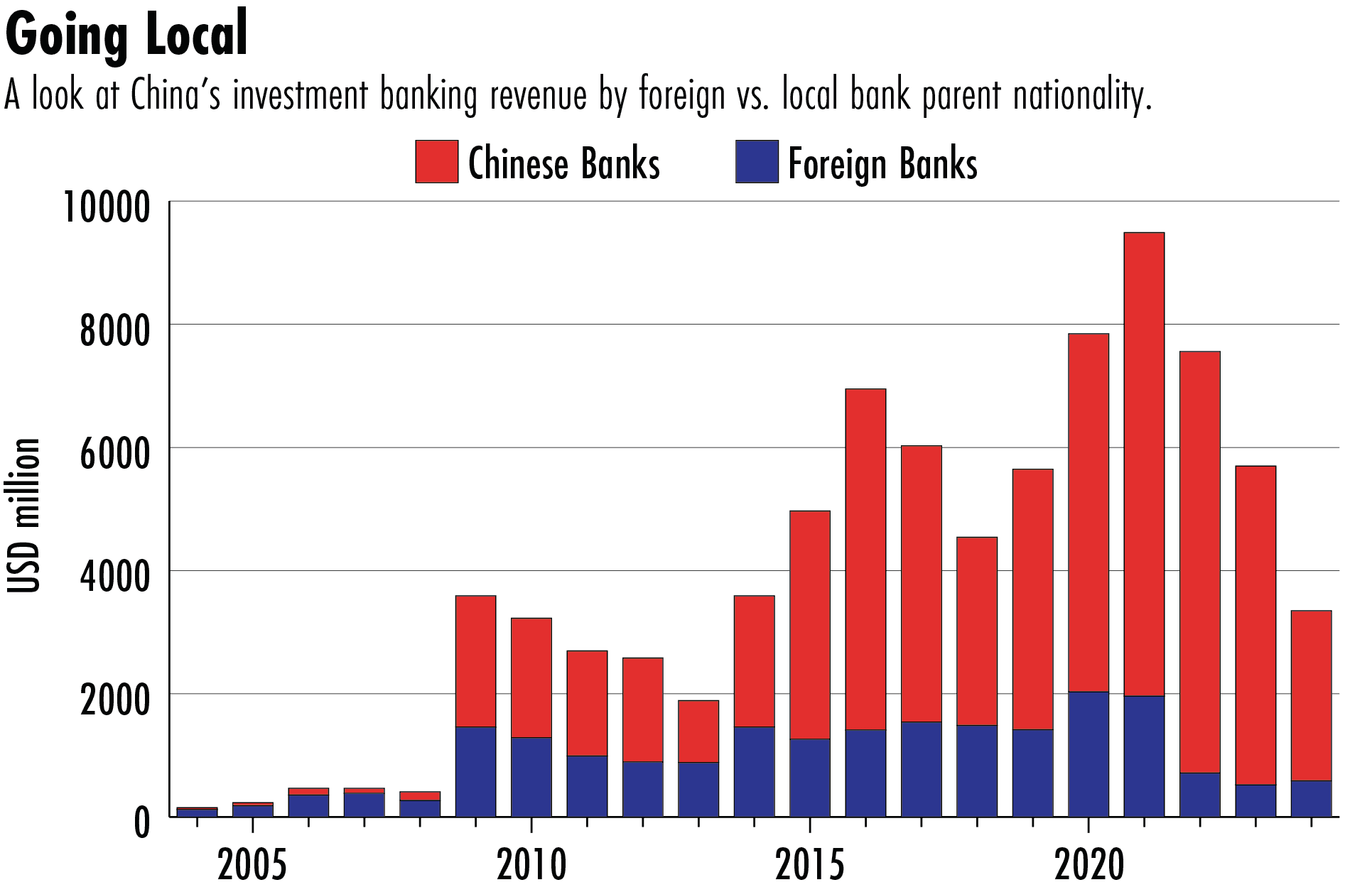

Banks

The good old days are also over for foreign investment banks in China, whose lifeblood was once helping Chinese companies go public.

“They gave credibility to these domestic state-owned companies that wanted to do initial public offerings, and they had all the relationships with the foreign mutual funds and hedge funds that wanted to bet on China’s growth,” says Rick Carew, an advisory board member at the Brandes Center of the University of California, San Diego.

But IPO and deal volumes have plummeted amid China’s capital-raising winter. And global investors have also lost interest as China’s growth prospects dimmed. On top of that, the Chinese government has soured on the finance industry in the name of ‘common prosperity’. Speaking at a conference in Shanghai in May, JPMorgan chief executive Jamie Dimon admitted that parts of its investment banking business in China had “fallen off a cliff”.

There are signs that Chinese stock markets are slowly coming back, propped up by recent stimulus efforts. But in this cycle, Carew adds, domestic investment banks are taking the lead leaving foreign banks with a diminishing role.

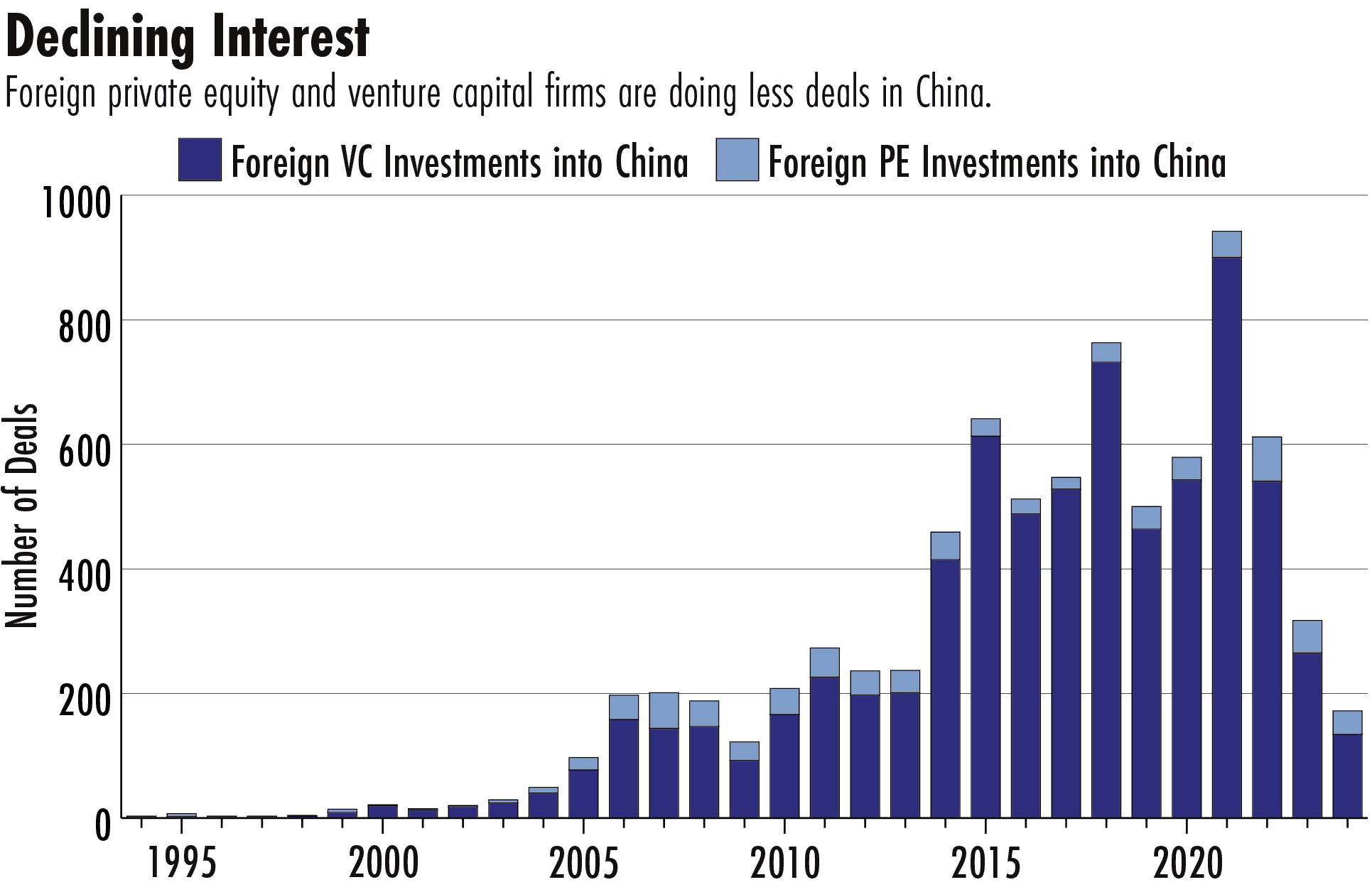

Venture Capital

Silicon Valley’s venture capitalists helped build Chinese tech behemoths like Tencent and Alibaba in the early 2000s. Today’s environment is vastly different.

China’s crackdown on industries like tech and private education has stifled entrepreneurial spirits and discouraged startups. Moreover, regulators in Washington are poring over companies’ portfolios, looking for ties to the Chinese state or investments in sensitive technologies.

“Right now, the premium [venture capitalists] can get out of the market may not be worth the risk they could face,” says APCO’s McGregor.

Some leading investment firms, such as Sequoia Capital and GGV Capital, have spun off their Chinese operations. Others have pivoted away. U.S. private equity and venture capital investments in mainland China fell from the peak of $39 billion in 2018 to $1 billion as of October this year, according to data from S&P Global.

The trickle of capital may dry up even more as the Biden administration’s ban on U.S. investments into Chinese sectors, including semiconductor and artificial intelligence, takes effect in January.

Consumer Goods

Companies peddling consumer goods have not been able to escape geopolitics either.

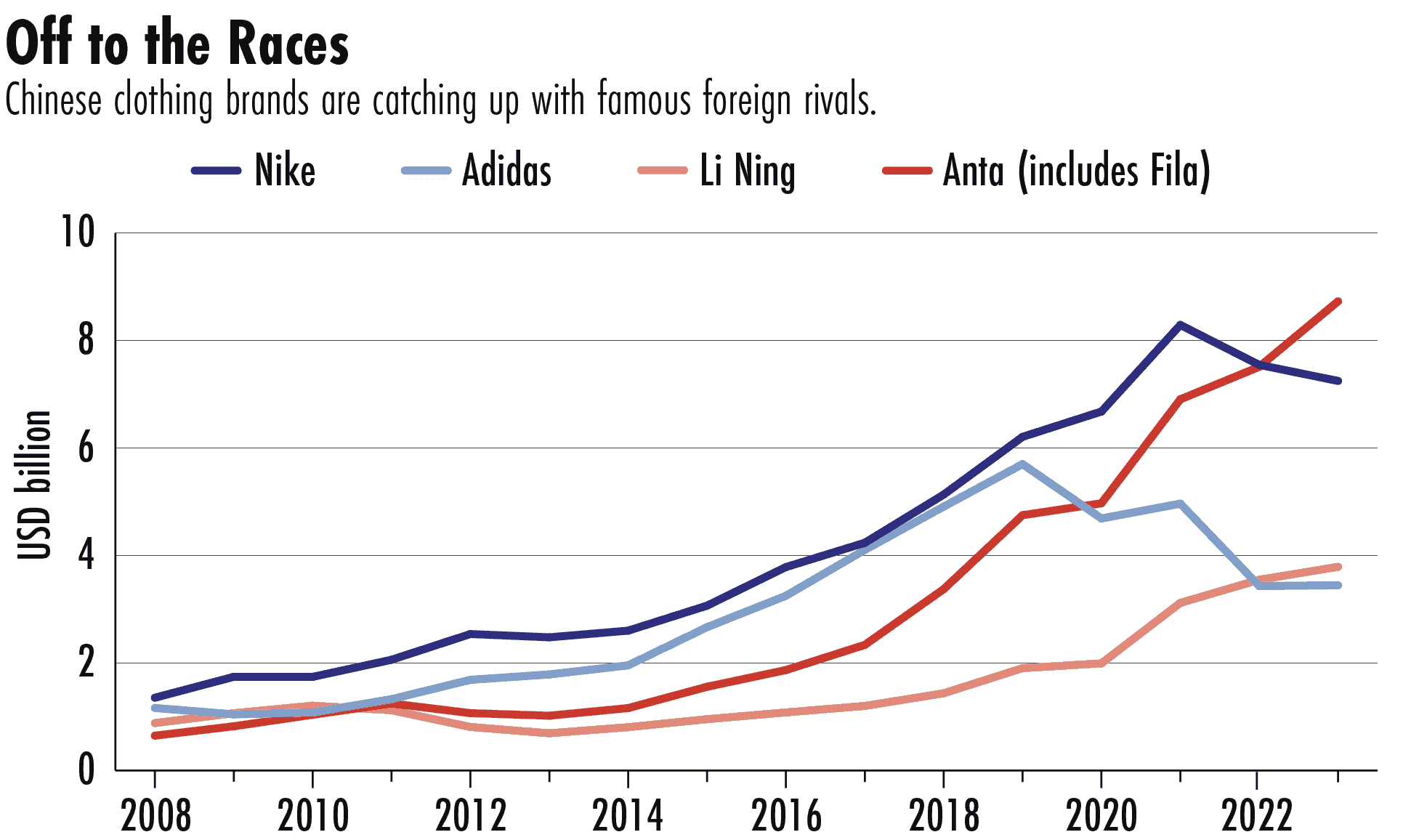

Nike, one of the U.S.’s most recognizable brands, has worked with Chinese factories and sponsored national athletes since the early 1980s. But in 2021, the sportswear brand faced a consumer backlash in China for expressing concerns about the alleged use of forced labor in Xinjiang and for removing the region’s cotton from its supply chain. Nike’s sales in China have gone downhill since the episode, before picking up this year. Nike did not respond to requests for comment.

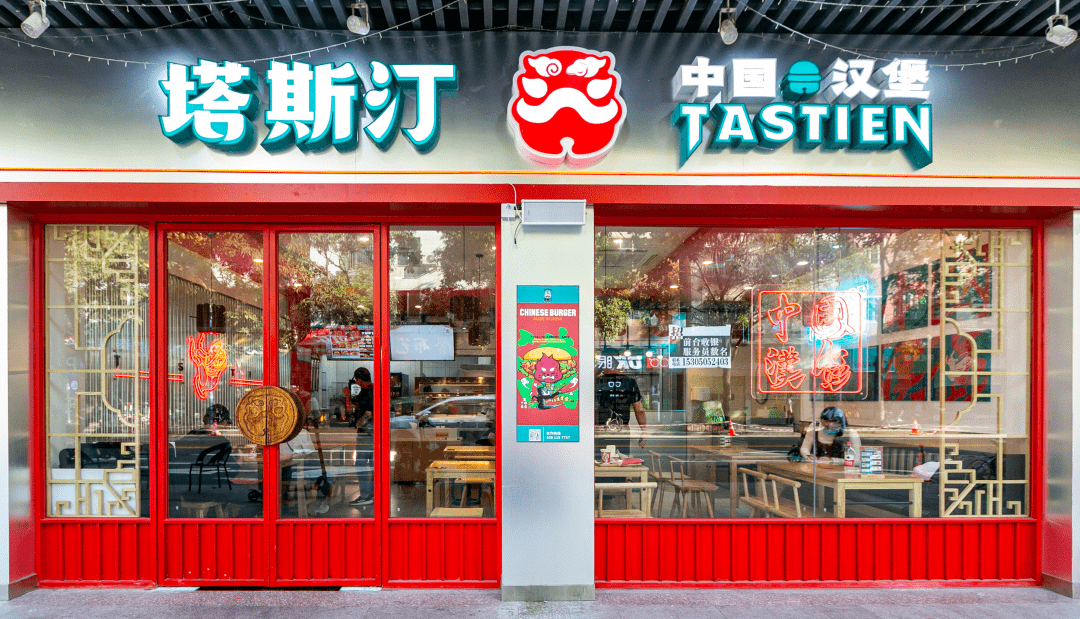

Another threat stems from nimble domestic rivals offering cheap products. Tastien, a local burger chain that took off in 2021, now operates 8,000 branches across the country, overtaking McDonald’s; another domestic player, Wallace, takes the crown with 18,000 stores.

Left: A Tastien storefront in Shenzhen, China. Right: A Wallace storefront in Beijing. Credit: Tastien, CFP

“Today, there are only a few sectors where multinationals still hold an absolute advantage in either technology, innovation or product experience,” says Jason Yu, managing director at CTR Market Research.

For instance, riding on the shift towards domestic travel, U.S. hotel chain Hilton has ambitious plans to open 100 hotels each year in the next few years.

Foreign luxury brands retain a certain cachet in China, but their reliance on the market has become a liability as consumers cut spending.

If a company can find a way to align their business strategy with the national priorities of Beijing and the Chinese Communist Party, then there might be room for it.

Dexter Roberts, a senior fellow at the Atlantic Council

Luxury groups from France’s Kering and LVMH to the U.S.’s Estée Lauder and Switzerland’s Richemont are now sounding the alarm. Kering, owners of labels such as Gucci, Balenciaga and Bottega Veneta, saw a 30 percent decline in revenues from Asia Pacific in the latest quarter, driven by weak demand in mainland China.

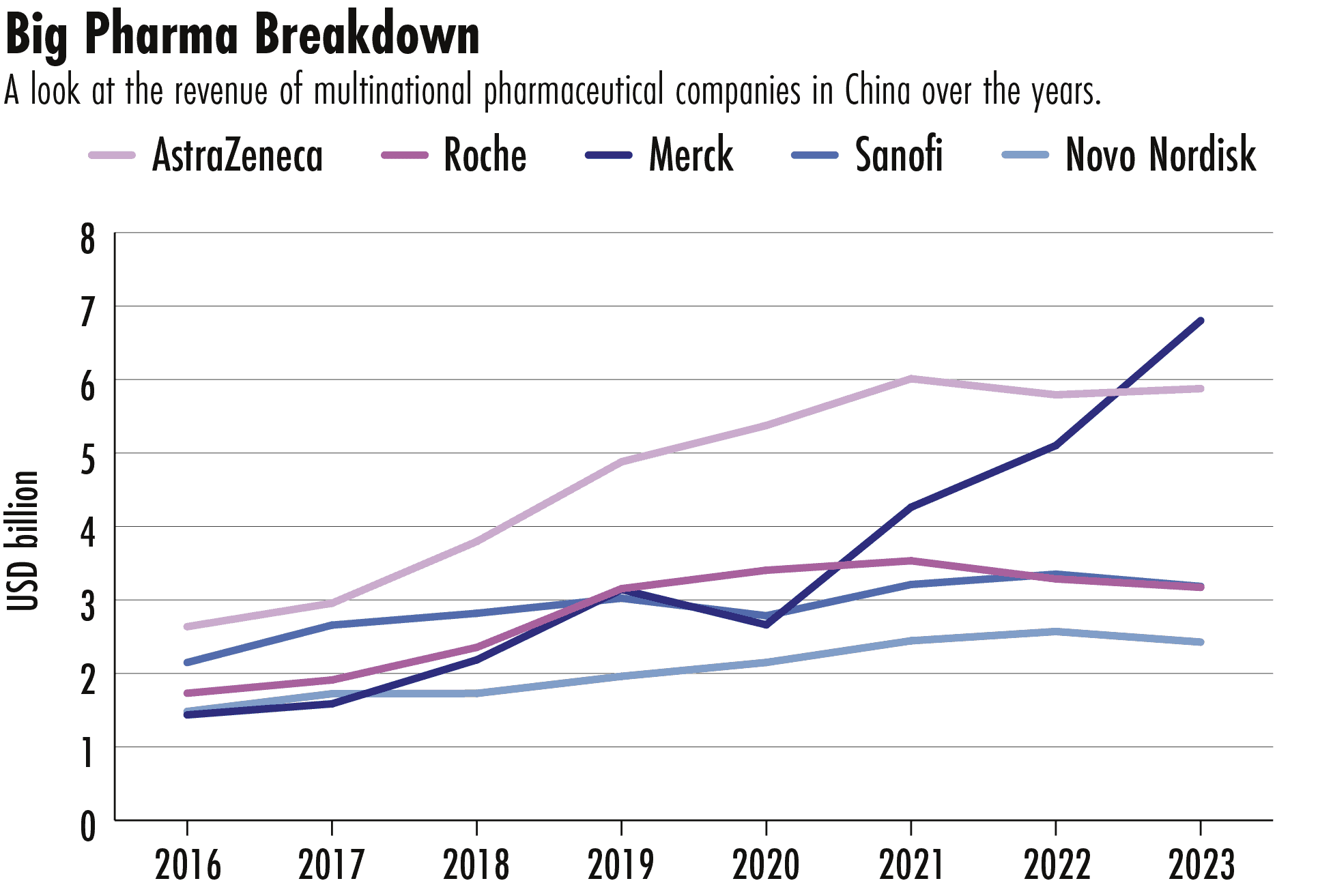

Healthcare

There are bright spots amid the gloom. “If a company can find a way to align their business strategy with the national priorities of Beijing and the Chinese Communist Party, then there might be room for it,” says the Atlantic Council’s Roberts.

One example is healthcare, where the Chinese government welcomes foreign drugmakers to cater to the medical needs of its aging population. Foreign drugs have been approved at a much faster rate since a regulatory reform in 2015. Accordingly, multinationals have dialed up their investments in the country.

Industrials

Companies have always been low key about divestment from China to avoid the ire of Beijing. Likewise, they are now avoiding publicity on new investments in the country to prevent unnecessary scrutiny at home.

“Some of them are expanding, but they are very quiet about it,” says APCO’s McGregor. Others inject new capital by taking on low-cost loans, which aren’t captured in the overall measure of foreign direct investment into China.

It is thus not always easy to gauge the scale of a company’s presence in China.

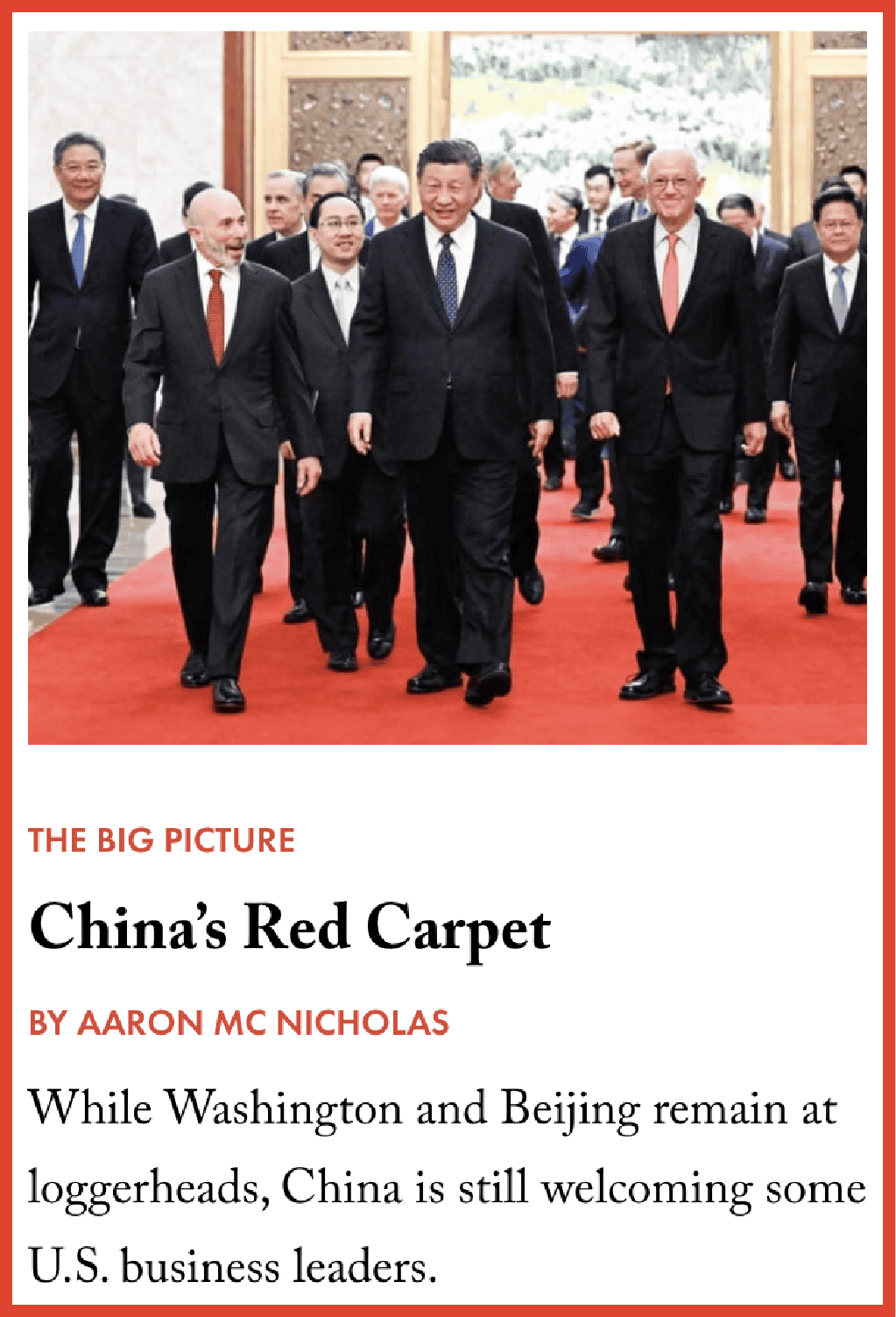

However, the U.S. executives who accepted the invite when Chinese leader Xi Jinping rolled out the red carpet in March demonstrated which companies remain committed to the Chinese market. They included familiar faces, such as Stephen Schwarzman of U.S. asset management company Blackstone and John Thornton of the Toronto-based mining giant Barrick Gold.

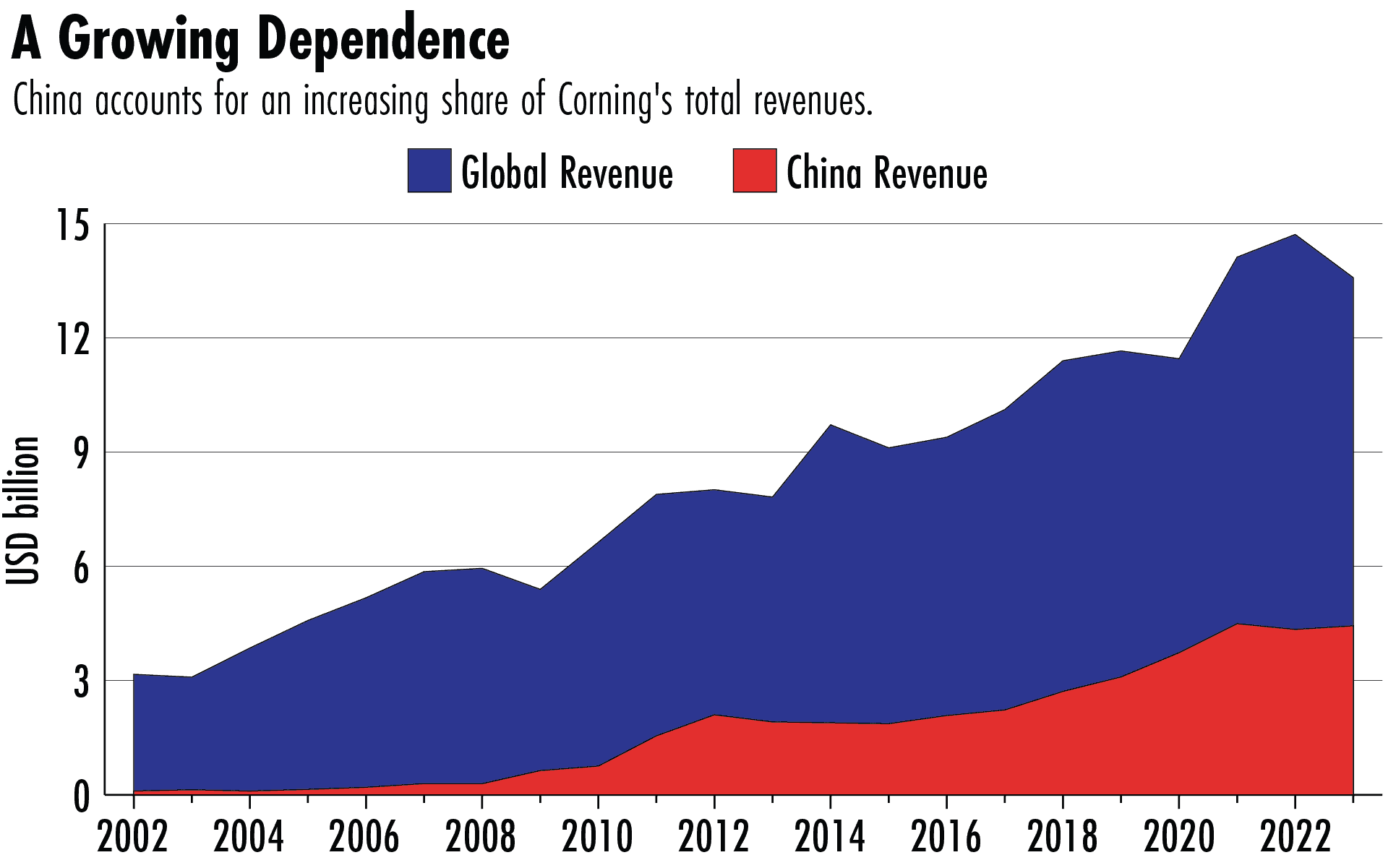

Another smiling face, right behind Xi in the group photo, belonged to Wendell Weeks of the New York-based Corning, whose operations in China stretch from glass substrates for television displays to optical fibers for telecommunication networks. And as its growing sales from the market indicates, there are still some American winners in China.

Noah Berman and Ella Apostoaie contributed to this story.

Rachel Cheung is a staff writer for The Wire China based in Hong Kong. She previously worked at VICE World News and South China Morning Post, where she won a SOPA Award for Excellence in Arts and Culture Reporting. Her work has appeared in The Washington Post, Los Angeles Times, Columbia Journalism Review and The Atlantic, among other outlets.