Angela Huyue Zhang is an associate professor of law at the University of Hong Kong, and a leading expert on Chinese tech regulation. She is the author of High Wire: How China Regulates Big Tech and Governs Its Economy, a highly acclaimed book that absorbs all that happened during China’s 2020–2022 tech crackdown to explain how the government there regulates its tech sector. In this lightly edited Q&A, we spoke about when and why Beijing’s attitude towards China’s big tech darlings changed, how the relationship between regulators and companies has developed in the aftermath of the crackdown, and what all this means for China’s artificial intelligence industry.

Illustration by Kate Copeland

Q: Your book provides a model for thinking about the crackdown on consumer tech companies. Could you introduce it briefly?

A: Chinese regulators are organized through an upward accountability system, in contrast to their democratic counterparts, which are held accountable to the people. So they are very sensitive to the shifting of the policy winds because they want to make absolutely sure that their policy mandates will not be deemed in contravention with the top’s initiatives.

During the early days of China’s consumer tech development, agencies were very averse to imposing very strict regulations on Chinese consumer tech firms like Alibaba, which actually faced a lot of complaints from their competitors, like JD.com. A lack of checks and balances in the regulatory system gives agencies wide latitude in deciding how to regulate these companies. The agencies tended to take a lenient stance in tackling these issues in the old days so as not to be seen as contravening the top leadership’s initiatives.

| BIO AT A GLANCE | |

|---|---|

| AGE | 42 |

| BIRTHPLACE | Zhanjiang, Guangdong, People’s Republic of China |

| CURRENT POSITION | Associate Professor of Law, University of Hong Kong |

| FUTURE POSITION | Professor of Law, University of Southern California, starting Fall 2024 |

When the government started to send a signal in late-2020 that they were going to mobilize a massive enforcement campaign against big tech companies, agencies then tended to err on the side of doing too much, because they had to demonstrate loyalty. Moreover, from an agency standpoint, it was especially important to protect one’s turf because everybody else was working very hard to expand their turf during this period. It was a golden opportunity for agencies to expand their policy control, which is their main asset. So they tended to do too much, enabled by a lack of checks and balances, which allowed them to go ahead with very aggressive actions with very little resistance from firms. In fact, because firms in China exhibit an unusual level of cooperation you don’t see in many other jurisdictions, that tends to lead to overreach.

So we can observe this paradox of regulators both doing too little and too much. In fact, this is a pattern you can see consistently in China’s regulatory governance, whether with the pandemic measures or the property crackdown. Consumer tech presents us with a perfect case study, in the sense that we can observe the whole regulatory cycle, from early lack of regulation, to strict crackdown and then regulatory easing. You observe the whole life cycle in a rich story.

Let’s start at the beginning of this life cycle. What were some of the regulatory features that enabled the consumer tech sector’s incredible growth?

Starting in the early 2010s, China’s policy priorities were overwhelmingly supportive of the consumer tech business. Because of that, these agencies took quite lenient action towards these companies, or in some cases complete inaction over mergers involving the VIE structure. [“Variable interest entities” are a corporate structure that allows Chinese companies to get around rules that forbid foreign investors from buying stakes in Chinese internet firms, by setting up an offshore company into which the Chinese company pledges to consolidate its profits.]

The Chinese government sent a very strong policy signal in 2015, when it introduced the Internet Plus initiative, [a five-year plan to upgrade traditional manufacturing and service industries by integrating them with big data, cloud computing and other ‘internet of things’ technologies]. In fact, this initiative was first proposed by [Tencent founder and CEO] Pony Ma. This shows how Chinese tech firms are actually very active participants in the policymaking process. They understood the government’s priorities, so they lobbied very hard to win policy support, touting the fact that the growth of the consumer tech business was crucial for upgrading the Chinese economy and could solve a lot of unemployment problems. That’s why from 2015 to the tech crackdown in 2020, this period really was a boom period for China’s consumer tech business with such strong policy support from the government.

How do tech firms like Tencent and Alibaba conduct their lobbying activities and influence government policy in China?

Companies rely on both formal and informal institutions to lobby the government. Formally, some of their leaders are Chinese Communist Party members, like Jack Ma. A lot of them are active participants in Chinese political events like the National People’s Congress or the Chinese People’s Political Consultative Conference. For example, Pony Ma has submitted more than 50 proposals to the NPC over the years. This is a channel to influence and shape policy initiatives at the very top.

They also have very strong informal channels to influence government policy. One is through their investors, which could be state-owned funds or state-owned firms, which have strong backing within the ministries or local governments. They could have political elites such as princelings that invest in the business — a lot of them do. That also aligns their interest with political elites in China. This is another informal way of lobbying. If something bad happens, they know they have a protective shield.

At this point, regulators will be more averse to taking action precisely because of the painful memory of the previous cycle, which has severely battered all these tech entrepreneurs and spooked investors.

They also need to understand the mindset of the regulators, given the whole system is quite opaque. Here they rely on a very large network of what I call “information intermediaries.” These tend to be academics, who are often consulted by the regulators and also work very closely with tech firms. Academics play a very important role in facilitating information exchange, in essence brokering information. Over the years, you’ve seen more and more of a revolving door between the big tech firms and the regulators. This is another way for tech firms to better understand the mindset of the regulators.

Your book brings up the influence of large institutional investors like Sequoia Capital China (now HongShan), noting how they often invest in multiple competitors within the same industry and encourage consolidation, potentially leading to uncompetitive outcomes for consumers. Could you say more about that?

It just shows how concentrated China’s tech sector is. Neil Shen from Sequoia is often regarded as the man who owns half of China’s internet sector. So even though he is not as well-known as Jack Ma or Pony Ma, in a way his influence and power is not any less than these two men. By the end of 2020, Sequoia owned over 300 Chinese tech companies and had stakes in the largest of them. For example, it invests in Alibaba, JD.com and Pinduoduo, which all compete with each other.

If you look at Sequoia’s track record, it seems to have played an important role in facilitating the mergers between some of the firms that he invested in, such as [food delivery platforms] Meituan and Dianping, a merger which really solidified Meituan’s market position. Also, Uber China and DiDi. You can see the common owners of these firms are actually the matchmakers behind these big tech mergers.

In the U.S., the common ownership of companies by financial investors [such as BlackRock and Fidelity] has drawn controversy, even though these investors only take a passive role in investing in these firms. So far in China, there hasn’t been a similar discussion, but it’s obvious that this common ownership by the same financial investors is already working to facilitate concentration in the industry.

Let’s move along the life cycle to the “crackdown” phase. You wrote in your book that even before the fateful Jack Ma speech in October 2020, and the cancellation of Ant Group’s IPO, there was already momentum building in Beijing to rein in fintech companies. How did that momentum begin?

One of the very common assumptions I want to challenge with this book is that the Chinese government did this as a deliberate assault on private businesses and that the Chinese Communist Party just wants to expand its control over the private economy. That’s an overly simplistic view. If you look at all the regulatory crackdowns, in each case the government had very strong, legitimate reasons to go after these firms.

In order to understand the regulatory tensions between Ant and the [People’s Bank of China, China’s central bank], we need to go back earlier to the financial scandals involving Anbang Group and the Tomorrow Group. These two companies taught the PBOC a lesson, that private firms providing financial services, with very high ownership concentrations and opaque corporate governance structures, are going to lead to massive misconduct. Ant was controlled by Jack Ma.

The failures of these two institutions demonstrated to the regulator they needed to take a much tougher stance in regulating companies that are providing similar services. Why was the PBOC particularly concerned? Because the PBOC’s mission is not just as a central bank, but to maintain financial stability. If something bad happens to Ant like what happened to Baoshang Bank (controlled by the Tomorrow Group), the PBOC would need to step in to rescue them.

Then PBOC governor Yi Gang delivers a keynote speech on “China’s Experience with Regulating Big Tech,” at a Bank for International Settlements conference, October 7, 2021. Credit: BIS

Starting in 2018, the PBOC had already issued regulations to increase oversight of fintech companies. It also wanted to impose stricter capital reserve requirements [how much capital a financial institution must hold] to make sure companies like Ant had skin in the game. This would ensure they wouldn’t just borrow from state owned banks and then leverage them to lend to consumers while encouraging wanton consumption and massive borrowing without incurring any risk. In the summer of 2020, the PBOC had already issued draft regulations and notices in order to curb excessive risk from digital finance. Even after Ant filed for its IPO, the regulator was still chasing after Ant and indicating it would regulate it.

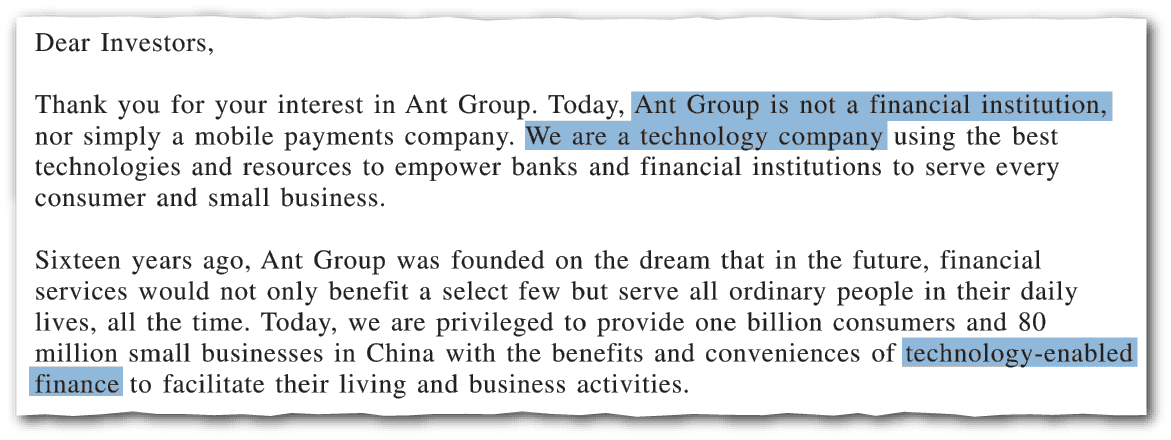

The thing is, Ant was very smart. It pushed forward its IPO at lightning speed. Note that Ant was initially called Ant Financial. It changed its name to Ant Group [in July 2020] to avoid scrutiny as a financial holding company. In the IPO prospectus, they dressed up their company not as a fintech company, but as a tech-fin company, claiming they were not a financial institution but a technology company, which helped them to get a much higher valuation. On the verge of Ant’s IPO, it had a $320 billion valuation, making this Alibaba spinoff bigger than J.P. Morgan, the biggest bank in the world. The scale of Ant really made the PBOC very nervous that this would be the next big bubble that was going to pop.

That also explains the subsequent regulatory actions you’ve seen. Now, Jack Ma has had to surrender control, and Alipay has no controller. Ant has become a company that no single shareholder can exert control. The whole goal of the corporate restructuring was to try to inject more transparency into the governance structure and ensure that no single person can exert excessive control over the firm, which makes it easier for the bank to monetize risk.

This may be a good point to turn to golden shares, which have gotten a lot of attention in the West. How much control do golden shares give the government? And are there any reciprocal benefits for Chinese firms?

The concept of golden shares dates back before the crackdown to the rise of video apps. Because these companies offer online media services, they need to obtain a video license from the [Cyberspace Administration of China, China’s top internet watchdog]. Having a government investor on the board helped them to obtain the necessary licenses to operate in the sector. So the golden shares don’t apply universally to all kinds of firms, as is speculated in Western media. It only applies so far to social media companies, particularly those that provide short video apps, although the crackdown did facilitate the CAC and its affiliated funds purchasing more golden shares in these companies.

By investing in a nominal number of shares in these companies, the companies now all have government representatives on the board, mostly to maintain content moderation and help appoint an editor overseeing content.

I think this is the biggest priority of the golden share initiative. But golden share investments also allow the government representative to veto certain company decisions, including [mergers and acquisitions] or IPOs. That goes back to what happened to DiDi after it went public. [In 2021, the ride-sharing company pushed ahead with its IPO on the New York Stock Exchange against the advice of Chinese regulators. The CAC retaliated by initiating a cybersecurity review of the firm and ordering mobile app stores to take down DiDi’s app. By year’s end, the company announced it would delist its shares from the NYSE.] The idea was that if we have a government representative on the board, they could potentially veto a transaction like that and prevent the IPO from happening in the first place.

As to how effective these representatives are at really exercising oversight over these firms, so far they’ve had a very targeted approach. I wouldn’t overstate their power and influence over the tech firms.

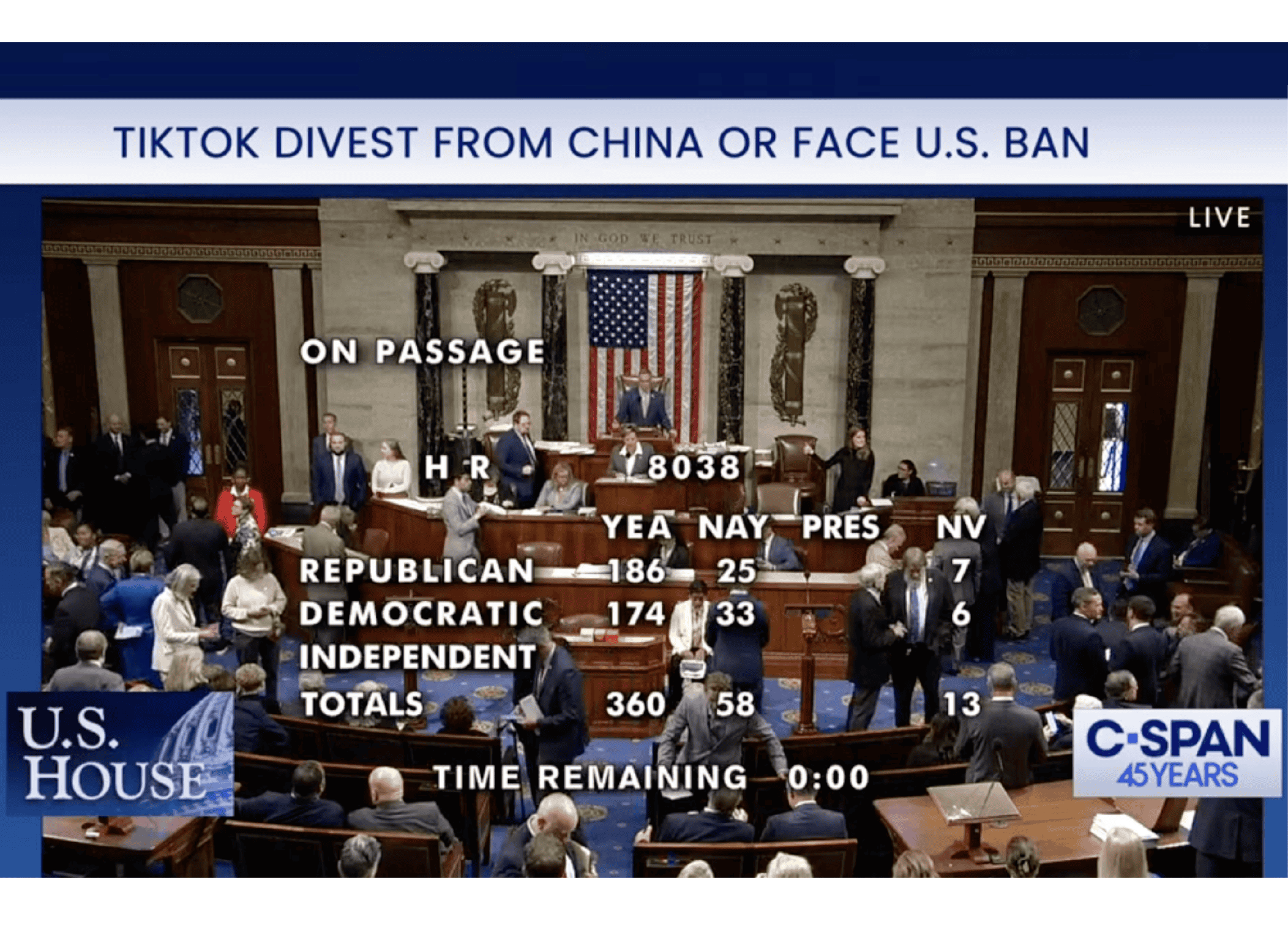

Does this kind of control have implications for ByteDance’s willingness to divest TikTok?1This interview took place before President Biden signed the TikTok sell-or-ban bill into law last week.

| MISCELLANEA | |

|---|---|

| FAVORITE BOOK | A Treasury of 8 Books by Tomi Ungerer. This classic children’s book is a favorite that I often read to my kids. Its simplicity is beautifully intertwined with profound messages that resonate with me. |

| FAVORITE FILM | Forrest Gump |

| FAVORITE MUSIC | Jazz |

| MOST ADMIRED | Richard A. Posner |

The main concern about TikTok is the Chinese government’s access to U.S. data and also the manipulation of TikTok’s recommendation algorithm. The company has gone to great lengths to address this problem and firewall itself from its parent company. The golden share investment only invests in the Chinese subsidiary of ByteDance that holds the operating license for short video companies. So it’s completely separate from TikTok. However, this kind of Chinese government influence over the firm casts a very long shadow over the independence of ByteDance. So despite the fact that legally, you don’t see any direct influence, it does make outsiders suspicious about the true independence of TikTok.

The Chinese government has the power to restrict ByteDance from selling TikTok’s technology to U.S. investors through export controls using restrictions introduced in 2020. It’s almost certain the Chinese government will insist on that for a variety of reasons, but mostly as a matter of national pride.

One thing I don’t see people talk about is how this actually benefits TikTok. The House of Representatives’ bill gives TikTok two options: either you divest or you disappear. So if the Chinese government makes it absolutely certain that they won’t allow ByteDance to divest, that bill effectively becomes a ban. And if Congress passes this bill and TikTok appeals in court, it will say this is a de facto ban that violates the First Amendment rights of its millions of users. U.S. courts have been very reluctant to support similar cases where legislation has limited freedom of speech. So in a way the Chinese government is doing ByteDance a favor by not allowing it to divest, because if it does allow it, then TikTok will not have a very strong argument in court.

All things considered, are consumers better off, following the regulatory crackdown?

For the most part, the competitive landscape has hardly changed. Companies like Alibaba and DiDi have lost a little bit of market share. Some very strict laws have been introduced, particularly the data regulations, which have significantly increased regulatory burdens for a lot of firms, big and small. That disproportionately punishes the smaller firms by making operating costs more expensive.

These heavy-handed interventions have really spooked investors and undermined investor sentiment. Investment has significantly plummeted. We haven’t really seen any new entries. To the extent that you want to give the consumer more choices, that hasn’t really happened.

What about the regulators? An important feature you describe in your book is how the crackdown has paradoxically created more volatility in the system, forcing government ministries to act more cautiously.

Absolutely. At this point, regulators will be more averse to taking action precisely because of the painful memory of the previous cycle, which has severely battered all these tech entrepreneurs and spooked investors. The market is very fragile, and that fragile outcome will lead to more volatility. At this point anything the government does, so long as it’s perceived as negative, will be viewed by the market very negatively.

Just look at the example of the video gaming regulations last December. The gaming regulators did not anticipate that the introduction of the draft rule would cause such huge repercussions in the market, because previous draft regulations had already been circulated among the lawyers. It was not something completely unanticipated by the community, except for certain provisions that need more clarity. Unlike during the tech crackdown, it was an isolated regulatory move done before the end of the year because the agency wanted to just tick a box and have an end-of-year accomplishment. But the market reacted so badly. If you’re a government agency right now, you have to be extremely cautious in what you do.

How does this “life cycle” model apply to the AI industry?

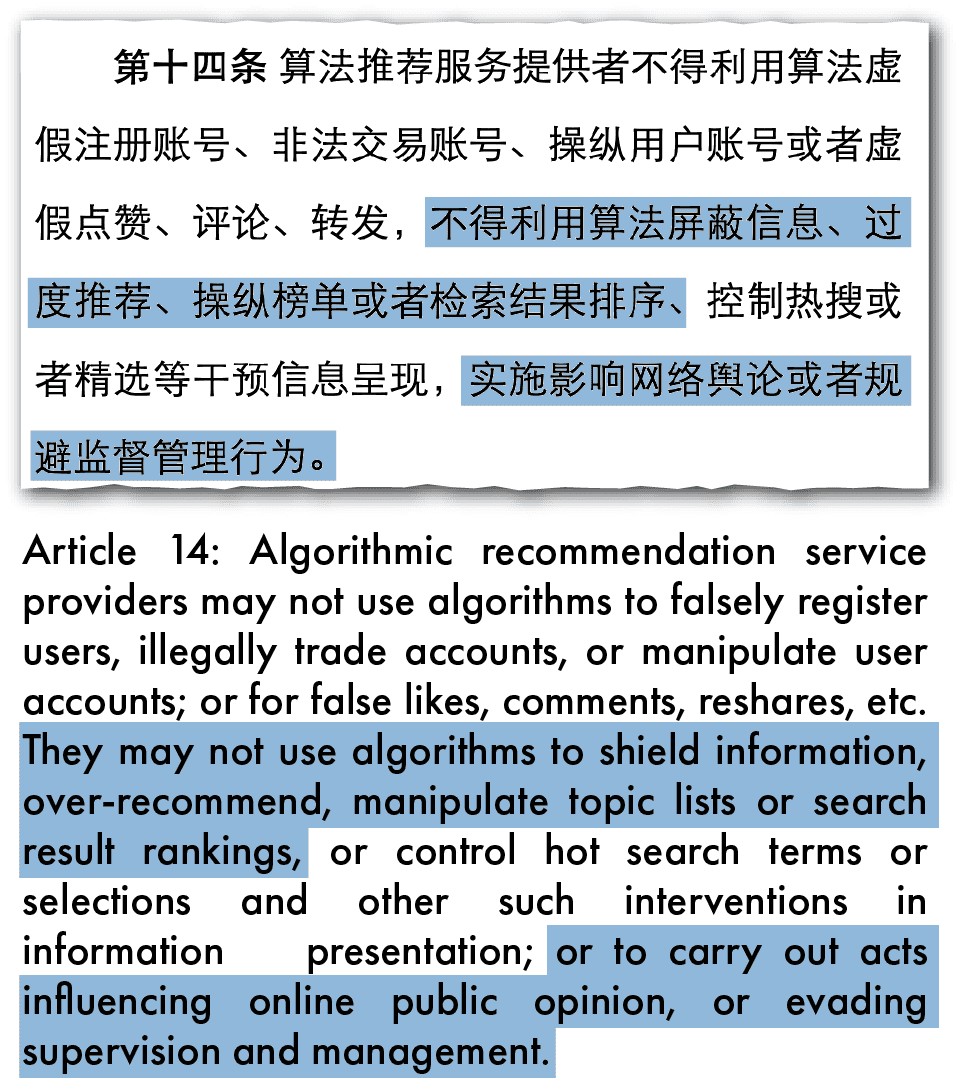

With AI, we’re just at the very beginning of the cycle. Around 2018, Chinese regulators started to get nervous about AI after seeing what happened with the Cambridge Analytica scandal and how the manipulation of public discourse by a large platform like Facebook could have huge political implications. That was the beginning of the inquiry and investigation into firms like ByteDance, which at the time had some of its apps suspended. That was the starting point, and why the CAC was the first agency to roll out legislation to regulate recommendation algorithms in 2021.

A year later, they introduced deep fake regulation, and in 2023 they were the first to introduce legislation to regulate generative AI. Consistently you see this pattern of the CAC being inherently insecure about information control and being very proactive in regulating this technology. That’s consistent with its own bureaucratic mission as an internet watchdog for content moderation.

…generative AI could pose a threat to political stability, but it could also bring enormous potential for economic growth, which China desperately needs.

At the same time, generative AI could pose a threat to political stability, but it could also bring enormous potential for economic growth, which China desperately needs. It’s also at the center of the China-U.S. tech rivalry. So the government is trying to balance competing interests, and within the bureaucracy itself, different factions are competing to exert their bureaucratic interests. The CAC was very aggressive in imposing content regulations, but then you had other departments, like the MIIT, the Ministry of Science and Technology, and NDRC, factions that are more pro-growth, and tasked with achieving the self-sufficiency initiative.

So you have a pro-growth faction, and then a pro-regulation faction, and during the legislative process you can see this very clear dynamic between two factions. When CAC introduced the first draft of the rules governing generative AI, it was really strict, causing a lot of complaints from industry. Then, the final draft was significantly watered down, sending a very strong policy signal that the pro-growth faction has prevailed over the pro-regulation faction.

That policy signal is very important, not just for boosting investor sentiment and industry growth. It’s also a very strong signal to regulators that the policy winds are in the direction of growing this technology and that you should support and enable it. We see that very clearly with enforcement records since the law became effective. Within two weeks of the law coming into effect last year, 11 firms were greenlit. No firm has been investigated for data violations. Have they conducted any sort of investigation of IP infringement? No.

From the first draft to the finalized version, the law [regulating generative AI] was finished in only three months — lightning speed. They did it quickly to assure investors that the regulation is meant to enable the industry.

My prediction is that, exactly like what we saw with consumer tech regulation, regulators are highly unlikely to take very aggressive action against any of the large AI firms. Individuals producing deep fakes may be prosecuted, but big tech firms like Baidu, ByteDance, MiniMax will be protected. We are at a stage where the regulators will tend to do too little.

Is there an example that comes to mind where you think regulators are doing less than they should on AI?

A good example is the interim measure to regulate generative AI. The final measure has a very big carve out — it only applies to publicly available AI services. In other words, if you were working on this AI technology and then you only provide the services for internal use and it’s not available to the public, you’re not subject to this law at all. If you’re creating generative AI within the lab, it’s also not subject to this law and you don’t need to go through this licensing regime. Of course, generative AI services can still infringe IP rights and data and privacy regulation. But the priority of enforcement is content moderation.

Another example is a highly controversial IP case last November. A Chinese court decided to grant copyright to an AI generative image, making China the first jurisdiction to do so, in sharp contrast to what you see in the U.S. where the courts and the regulators consistently deny giving this kind of copyright protection. One important reason behind it was because the judge thinks that the copyright will help incentivize people to use AI services and in turn boost its development. So regulators got the message, and they will enforce the law in accordance with Beijing’s policy mandate.

Eliot Chen is a Toronto-based staff writer at The Wire. Previously, he was a researcher at the Center for Strategic and International Studies’ Human Rights Initiative and MacroPolo. @eliotcxchen