Barry Naughton, the So Kwan Lok Chair of Chinese International Affairs at UC San Diego, is one of the world’s leading experts on China’s economy and its transformation over the last half century. His textbook The Chinese Economy: Transitions and Growth, has long been a must-read for students of China; more recently he has coined the term ‘Grand Steerage’ to describe how Xi Jinping’s government is trying to shape the country’s development. In this lightly edited transcript of a recent interview, we discussed Beijing’s current stimulus efforts before going on to talk about the strengths and weaknesses of Xi’s vision for China.

Illustration by Lauren Crow

Q: We’re speaking after an autumn during which Beijing has announced various stimulus measures, and just after the Central Economic Work Conference where they talked about looser policy to support the economy next year. How do you assess the action they’ve taken?

A: Clearly, the December Economic Work Conference represents the culmination of a policy turn that dates back a couple of months. It puts significantly more stress on increasing aggregate demand, and especially consumption. It’s an important shift, but it comes in the context of difficult economic challenges that they’ve really only begun to grapple with. I would look at this more as a necessary precondition for putting together an effective set of policies, rather than the actual policies needed themselves. We should wait and see if they put more meat on the bones this time.

There’s been plenty of criticism of Beijing’s economic policy in recent years, and alarm about whether China is entering a period of so-called ‘Japanification’, where it experiences years of sluggish growth. How do you think we should characterize the ‘Xi Jinping economy’ right now?

| BIO AT A GLANCE | |

|---|---|

| BIRTH YEAR | 1951 |

| BIRTHPLACE | Chicago, USA |

| CURRENT POSITION | So Kwanlok Professor at the School of Global Policy and Strategy at the University of California, San Diego |

We definitely need to ask what Xi Jinping is trying to achieve with his economic policy. Xi Jinping probably feels that the economy’s performance, in terms of his needs and demands, is actually pretty good.

Of course, we don’t know for sure what goes on in Xi Jinping’s mind. But I think we can characterize his approach as this: ‘Billions for tech, but not one cent for bailouts.’

Now, that’s oversimplified. But it captures two elements of what Xi Jinping wants. The first is, high tech and secure development, or what Xi would call high quality growth. And the other is that he’s very averse to bailing out failing businesses or failing local governments, even when they could potentially be put back on their feet with a bit of a financial helping hand.

| MISCELLANEA | |

|---|---|

| BEST BOOKS OF 2024 | The Blue Machine: How the Ocean Works, by Helen Czerski, and A Swim in a Pond in the Rain, by George Saunders |

| MOST ADMIRED | Those people who try to stick with their ideals in a very complex and imperfect world. |

Xi Jinping has essentially imposed these constraints on the economy: This is the framework within which policy making has to take place. These constraints explain a lot about what’s going on, and why they haven’t done things that outside economists might be urging.

Where does this come from in terms of Xi Jinping’s political and economic philosophy? Why does he want to steer China in this direction?

In some senses, it’s very natural. Xi has, from an early stage of his administration, insisted that China’s not just looking for GDP growth. They’re looking for growth and security; later, he added that they’re looking for high quality growth. They have a set of developmental desirables that are quite different from just maximizing GDP.

The funny thing is that there’s a long list of these desirables. There’s actually a project at the National Bureau of Statistics, in line with Xi Jinping’s directives, to measure how high quality China’s growth is on a year to year basis. They have set up indices for efficient, innovative, harmonious, green, open and inclusive growth. And you’ll be happy to know that, according to the NBS, China’s urban development was of a 1.3 percent higher quality in 2023 than it was in 2022.

So there are a lot of things that Xi Jinping is asking for. But of course, among those, by far the most important is high technology development — and the corresponding development of economic, strategic and scientific self-sufficiency that allows China to be a global power, unconstrained by what he sees as hostile powers, including the United States.

In a way, that means that Xi Jinping doesn’t really care about what Chinese people want to buy and want to make, because that would be just ordinary GDP. He’s asserting that there’s something more fundamental than that: high quality GDP, which is determined, at the end of the day, by Xi Jinping himself. That’s a very strong, deeply rooted tendency of his.

And it’s really very similar to the impulse that drives a planned economy. Of course, China now has a much more efficient set of institutions, and so the government is steering the economy through mostly market compatible instruments. That doesn’t mean they work well, but at least it means they are compatible.

If, by some miracle, Xi Jinping was to join this conversation, he would probably say the strategy’s working: that China is the global leader in areas like batteries and electric vehicles, and may be catching up in chips. Would he be right to say that?

Well, it would be reasonable for him to say that. There certainly are areas, in multiple related green sectors, where China has established a dominant position, in terms of the efficiency with which they can produce things. And I’m sure that when Xi Jinping gets up in the morning, and has his first cup of tea, he’s feeling very optimistic. He’s looking at these intersecting green sectors — solar power, wind power, batteries, electric storage, electric vehicles, maybe hydrogen production — and in all of these, the big Chinese commitment to development has led to very dramatic cost reductions that are still ongoing.

Even though we’ve adjusted to this dynamic cost performance, it still exceeds our ability to understand the implications. This green energy complex might have reached the point where it becomes economically cheaper than the old fossil fuel complex. That’s going to have huge implications. Even if we’re suspicious of Chinese policy, even if we’re worried about Chinese behavior and the way they manipulate economic success, we’re still not going to be able to stop an economic and technical transformation of this magnitude.

He’s also probably feeling pretty happy because he can argue that his policies have prepared China reasonably well to respond to whatever is coming down the road with the new Trump administration. The ironic thing is, they’ve carried out their de-risking and decoupling program, even while they rail against other countries de-risking and decoupling. They’ve actually done a somewhat effective job of insulating their economy and identifying the areas where other economies are dependent on them. I bet he feels pretty self satisfied much of the time.

Do you see it as realistic that China will become self-reliant in chips, in the way that Xi might also want?

No, not in a reasonable, foreseeable time frame, five to 10 years. But China is making major investments in each link of the entire semiconductor industrial chain, and they’re making progress. That’s not saying as much as it could, because in many of these links, they started with nothing. Making progress means that they’re creating embryonic structures that might develop into cutting edge facilities in a decade. Of course, in a decade, the semiconductor industry will have moved on. I don’t think anybody could say that that has been a successful industrial policy so far, and it’s been very costly.

Left: Chinese Premier Li Qiang visits Shanghai Super Silicon Semiconductor Co., August 28, 2020. Right: Xi Jinping visits HGLaser, a laser equipment supplier, June 30, 2022. Credit: Shanghai Government, HGTECH

To turn to the second half your formulation: no bailouts. How has that manifested itself in the last two or three years?

Before we talk about the last couple years, let’s again link this to deep seated elements of Xi Jinping’s world view. Of course, anti-corruption is the linchpin of Xi Jinping’s consolidation of power. The fact that the anti-corruption campaign is still ongoing shows that he has a certain suspicion of the motives and the ethics of a lot of people in the power system, and that he wants a much more disciplined society — especially a much more disciplined Communist Party. That’s a big part of his fundamental world view.

And so when he comes to look at how to resolve an economic situation like the housing bust, and the crisis in local government finance, he’s very averse to the idea that you’re going to reward anybody who either failed to manage their local jurisdiction effectively, or who made reckless investments. He just does not want to bail any of those people out, because it would create a bad precedent.

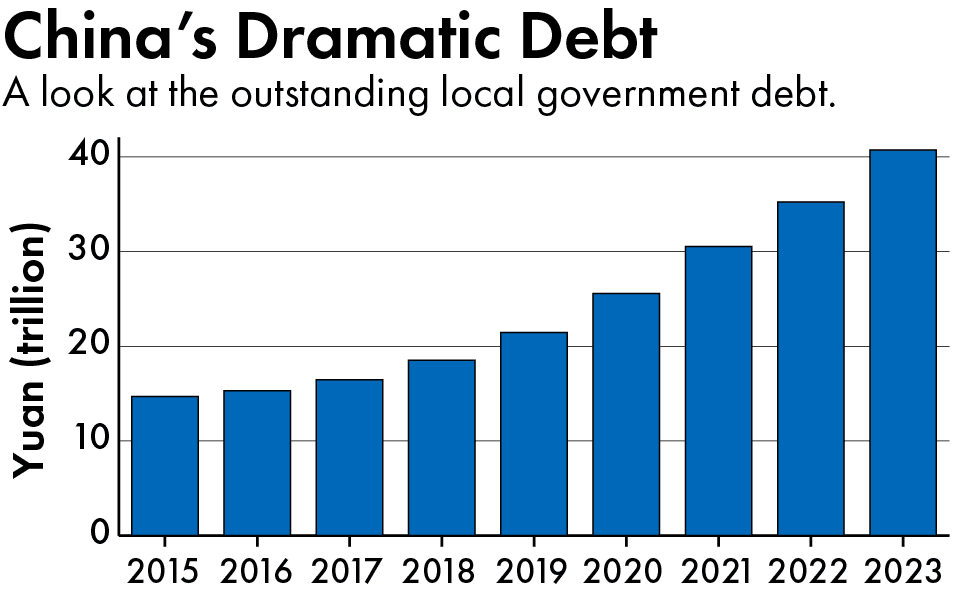

This also means that none of the things that we’ve seen to prop up demand and keep institutional structures intact have yet involved a substantial resolution of large amounts of debt. He keeps refinancing, kicking the can down the road, injecting some funds into the system to keep anybody from failing, but without resolving any of the problems.

Xi Jinping is making a gamble that all these technologies will at some point come together and produce a sudden surge of productivity. And he might be right. We can’t say for sure that he’s not. But thus far, he’s very much not.

That’s really a problem, because at a certain point you have to clean up the mess. You mentioned earlier whether China was becoming Japan-like: this is one respect in which it certainly is. Japan spent almost a decade trying to painlessly restructure a financial system that had suffered a huge reduction in the value of its assets. It was the fundamental problem that lay behind the so-called ‘Lost Decade’ in Japan; and now China seems to be repeating some parts of that.

Any attempt to fully restore the financial system to health is going to imply recognizing and apportioning losses though, right? For example, you either say to investors that bought local government debt that has gone bad that they are going to take the hit, or you apportion the cost to the central government. There seems to be an ongoing reluctance to make those sorts of choices.

I like the way you put it. It’s a question, in financial slang, of deciding who gets a haircut and how much — and China hasn’t done that. The only thing they’ve done is try to say, no haircuts for people who prepaid for their housing units, we should try and guarantee delivery for them. That’s politically a good idea, but it’s also the politically easy policy.

Xiao Yuanqi, Vice Minister of the National Financial Regulatory Administration, discusses the “white list” mechanism, October 17, 2024. Credit: CCTV

What is much harder is deciding who gets forced into bankruptcy, who gets bailed out, and who pays what costs in the process. The best practice is to force some of the early, worst case, bad actors into bankruptcy, but then in order to restore confidence, provide financial support to the better firms. China had the chance to do this with [collapsed real estate developer] Evergrande, but it never did put it decisively into bankruptcy, and instead just let it bleed to death. And despite the supposed existence of a “white list,” it’s never provided believable support to private real estate firms. As a result, nobody’s expectations in the real estate sector can be stabilized, and there’s a huge overhang of unsold property, especially outside the biggest cities, Beijing, Shanghai and Shenzhen. Although there’s been some stabilization recently, it’s hard to believe that the housing sector is anywhere near returning to health.

Why won’t the ‘billions for tech, no bailouts’ approach work longer term?

There are two fundamental problems. The first is it leads to a massive misallocation of resources, so that the underlying productivity of the economy is basically not improving. When we look at total factor productivity growth, which is the economists’ attempt to figure out what you’re getting from pure efficiency gains, China’s not really experiencing significant productivity growth. That is astonishing, because if we look at this economy that’s implementing all these new technologies, we think, wow, that’s gotta produce some kind of explosive growth in productivity. But we don’t see it.

And it’s fundamentally because, for example, China is investing in lots of semiconductor equipment plants that are losing immense amounts of money; it’s investing in thousands of miles of high speed rail that go where nobody wants to go. There are just these huge, long run implicit costs from not improving the efficiency of your society.

Now, of course, on some level, Xi Jinping is making a gamble that all these technologies will at some point come together and produce a sudden surge of productivity. And he might be right. We can’t say for sure that he’s not. But thus far, he’s very much not.

So that’s one problem, and something economists worry about, although maybe ordinary people can’t be expected to take this that seriously. The second problem is something that ordinary people do have to take very seriously: and that is that China hasn’t been able to put together an effective macro economic policy.

In a way, it’s almost comic. For almost three years now, the global investment banks have been saying China needs more stimulus. Then they look at each policy that comes out and they say, it’s not enough. So we need to ask what’s driving this, systemically?

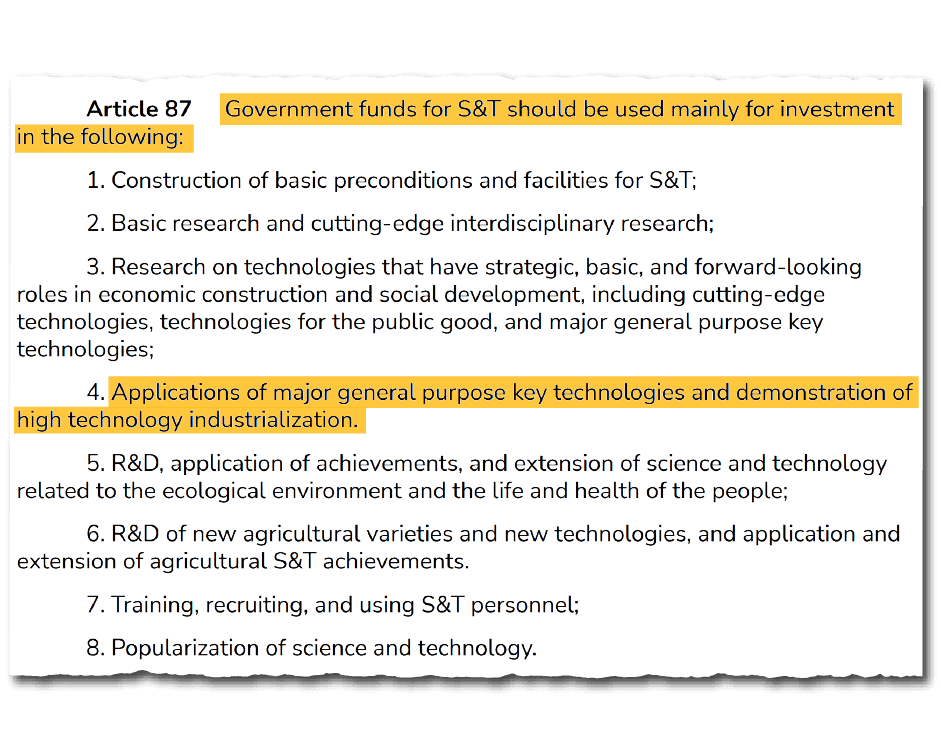

on the Progress of Science and Technology”, covering “high technology industrialization”. Source: CSET

I think the answer is, there is a stimulus policy, hiding in plain sight. It’s one that is constrained to be a high-tech industrialization investment program. That may or may not work in terms of developing these industries, but it doesn’t provide a very effective stimulus — because it doesn’t create much employment, it doesn’t create much profit, it doesn’t create many new income streams, and so it doesn’t have stimulus multiplier effects. It creates a certain amount of demand for the immediate product that gets the investment put into it. After that, it’s a sort of a wet thud in terms of its impact on the rest of the economy.

But there it is, that’s the stimulus. We can see it when we try to track investment, which is not easy to do in China. What we see is a big decline in housing investment, with most of that slack taken up by an increase in industrial investment. Between 2019 and 2024, total fixed asset investment cumulatively has only grown by about 20 percent, so that’s 3-4 percent per year: but investment in some of the big high tech sectors has more than doubled during that time. There’s been a big shift in the composition of investment, towards high tech industry. And if you maintain a certain limit on the amount of deficit the government is willing to bear, and if you say that credit has to be allocated first and foremost to high-tech industries, there’s not that much left over for other kinds of stimulus that would be more effective.

There is a constant refrain about China’s economy, that there needs to be more emphasis on consumer demand and less on investment. The view of the ‘Xi Jinping economy’ that you’re expressing seems to explain why the reluctance to unlock the power of the Chinese consumer persists.

Certainly, although I would just caution on one thing. Outsiders are much too prone to hear Chinese policy makers say we want to increase domestic demand, and interpret that as being them wanting to rebalance the structure of the economy towards consumption. As far as I can determine, China has never, since 2008, said we’re going to rebalance the economy away from investment, towards consumption.

One of the interesting things about the economic work conference that finished a couple days ago is that the first priority for 2025 is to vigorously increase consumption demand. That’s new. But then the next clause is, to improve the efficiency of investment. One thing it doesn’t say is ‘rebalance’. It doesn’t say shift resources away from investment towards consumption. You could say, well, it’s implicit. But it’s only implicit, it’s not explicit. Do they really want to do that rebalancing, or do they enjoy sitting atop an economy that can invest trillions of dollars? I think they rather like it.

Do you see unemployment being a structural problem for China? Put simply, is the Xi Jinping economy going to provide enough jobs for the Chinese people to do in future?

It’s really a serious question. Economists are so programmed to believe that labor markets adjust, and you don’t want to be a Luddite. Every new technology creates disruption, and then people adapt, markets adapt. And I do kind of believe that.

But on the other hand, China seems to be rushing so fast into so many of these technologies, without really worrying about what their impact on employment will be, that it seems, at a minimum, to be reckless.

China, the country that benefited the most from globalization, chose to turn against it, and to say, ‘Oh, that was okay, but we can do much better’. That was ultimately very destabilizing for the whole world.

There’s two different labor markets, too. There’s the market for newly minted college grads, who compose a whole spectrum of skill levels, but which certainly includes very highly skilled and very bright, capable young people. And there’s a whole other labor market of mostly migrant workers.

Both these markets are in crisis. The data that China releases are basically all about the first one: the urban, relatively high-skilled market. But the migrant market also seems to be in some kind of crisis. Millions of migrants have probably returned home and don’t have very much to do: Scott Rozelle has written very movingly and convincingly about this. I think these twin labor market problems are serious and long term, and it’s hard to see what they’re doing to deal with them.

Why doesn’t China introduce a more progressive tax system, to redistribute wealth somewhat, and also improve the welfare system?

That’s a great question. And to be honest, I don’t know. They have backed themselves into a corner. Their primary constituency is really a couple of hundred million urban people. They care a lot about what those people think, and not so much about rural people and migrants. They seem to be committed to protecting the full value of the pensions and health care benefits for all the urban residents, and not subjecting them to additional taxation.

Here’s this government that, in many ways, is not at all responsive to public opinion. But on four or five crucial economic issues that impact state workers, government employees and urban full time employees of other kinds, they’re very, very cautious.

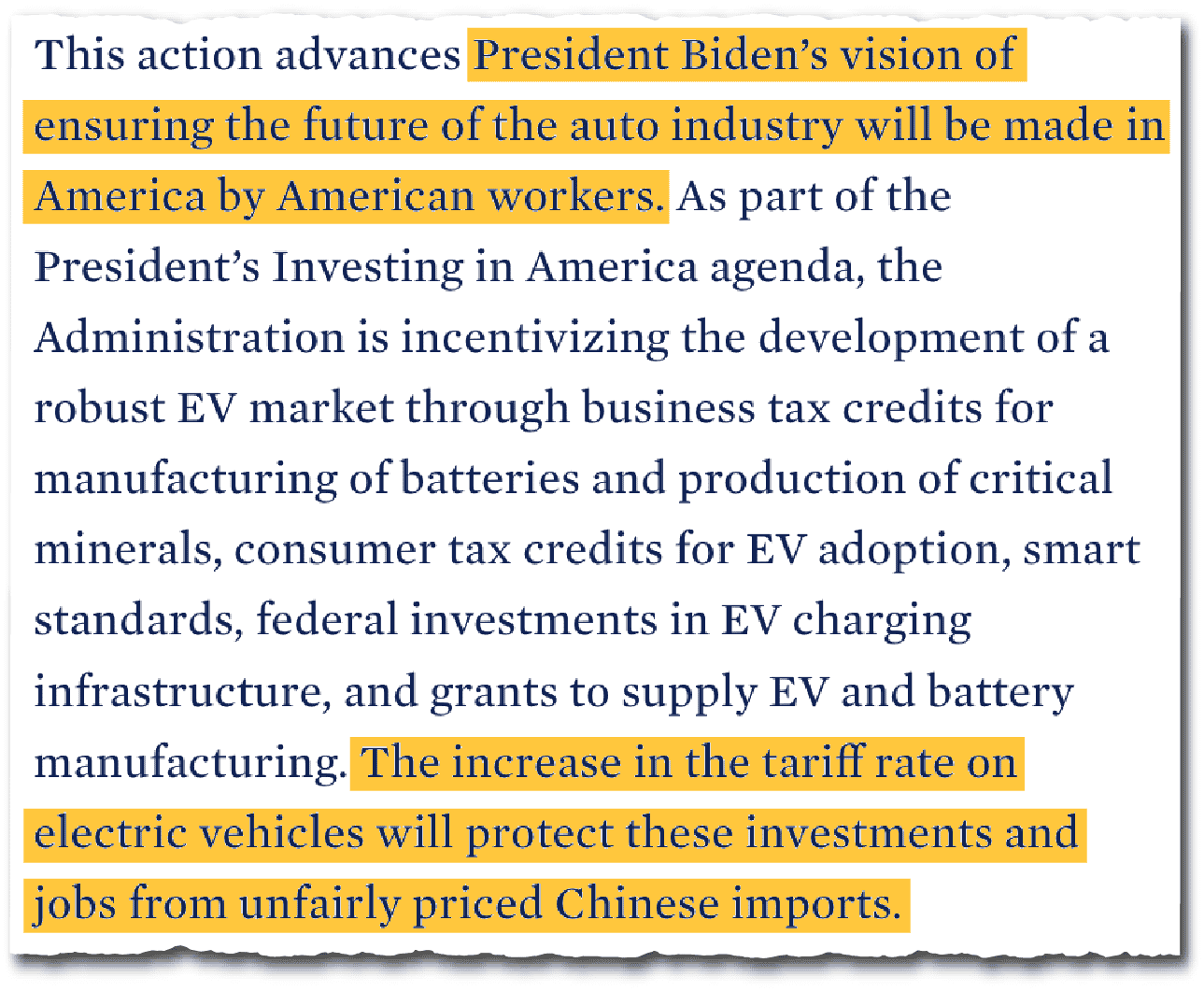

The response of the Trump and Biden administrations to all this has to some extent mirrored the Chinese approach, in terms of protectionism through tariffs, and in trying to steer the U.S. economy to produce more in certain high tech sectors. The alternative route could be to say, if China’s building a load of cheap electric vehicles for example, let’s just buy them: we can benefit from low-cost Chinese goods.

That makes sense for certain products, and it doesn’t make sense for others. We need to get beyond the sort of ‘protectionism good, protectionism bad’ argument, and try to craft a set of policies that amounts to reasonably efficient protectionism, that works in the American interest.

There’s two parts of that which we can lay out pretty simply. One is, let’s decide what are the sectors that we want to protect, and what are the sectors where we can benefit from opening up in the way that you suggest. EVs is a sector that we’re going to want to protect, because we have a big automobile industry that employs a lot of people. It’s behind the Chinese industry in terms of electric vehicles, but it clearly is capable of catching up.

By contrast, solar panels or batteries are areas where we don’t really have a significant industry. Chinese producers have meanwhile become very good, and very low cost. We should encourage Chinese investment in the United States to produce these products, both to create jobs and so that we can learn how to produce at that kind of scale and efficiency. We’re going to need a more explicit industrial policy.

The second thing is, we don’t want to trigger a chaotic scramble for protectionism among all the different countries in the world. We want to signal that we have certain interests, but they’re reasonably limited, and we are also interested in reaching a mutually beneficial equilibrium, especially with our allies, but also with China.

That’s difficult to do, but not impossible. We should keep our minds open to the idea that the U.S. will move towards more protectionist policy, but that it will be articulated in a way that is less disruptive, and benefits the United States’s interests.

Oddly enough, that’s probably more acceptable to China. We will essentially be saying to China, we’re just doing what you did, we’re protecting our interests. Their reaction could be: How come you didn’t do this a long time ago? This might, with a little bit of luck and wisdom on both sides, lead us to a new equilibrium that’s not terrible.

Do you worry, though, that people look at China’s economic policies and say, this is just a nationalistic country pursuing their nationalistic aims, we should resist all manner of Chinese trade. And that the logical extension is a full decoupling and a splitting of the world into different economic spheres?

Yes, I worry about it very much. I think some parts of it are inevitable. We don’t trust each other. We don’t want the Chinese inside our data systems, and they certainly don’t want us inside theirs. So there already is, and will continue to be, a decoupling in that respect.

That’s one of the reasons why EVs should probably not be a leading sector in terms of inviting Chinese investment — because they are computers on wheels, with massive sensor arrays.

But I completely agree with the spirit of your question, that we want to really try to resist all the pointless costs that would come from decoupling in the majority of sectors where there are no security issues, and nothing but shared benefit.

When you look back over your career, do you feel depressed about the way things have played out?

Of course, I feel sad that one of the things I devoted my career to was trying to explain to Americans why what was happening in China was important, and positive — and more potentially beneficial than a lot of people realized.

I was very disappointed at two things. One was the very gradual change in Chinese policy after about 2006. It’s a fundamental challenge to our understanding, not just of China, but of the world: China, the country that benefited the most from globalization, chose to turn against it, and to say, ‘Oh, that was okay, but we can do much better’. That was ultimately very destabilizing for the whole world.

The second thing is that China then abandoned the peaceful rise policy that it had in the first part of the century, and adopted a set of policies to play a greater role on a global stage — while essentially eroding the basis of the American system, and pre-positioning themselves to be in some kind of alternative leadership position. To be sure, the U.S. also contributed to this, especially by going to war in Iraq [in 2003], in violation of our own principles about international order. These changes were also deeply destabilizing.

So I feel quite surprised, and sad. But, it is what it is. You can’t predict the whole world.

Andrew Peaple is a UK-based editor at The Wire. Previously, Andrew was a reporter and editor at The Wall Street Journal, including stints in Beijing from 2007 to 2010 and in Hong Kong from 2015 to 2019. Among other roles, Andrew was Asia editor for the Heard on the Street column, and the Asia markets editor. @andypeaps