For a man whose cherished company is in the process of sinking tens of billions of dollars to produce some of the world’s most advanced semiconductor chips in the United States, Morris Chang seems remarkably unimpressed with the country’s approach.

|

|

| Illustration by Nate Kitch | |

| More in this series: | |

| The Japan Model |  |

| Rare Earth Reshore |  |

| Out of Bounds |  |

| Tomorrowland |  |

Two years ago, the founder and former long-serving chief executive and chairman of Taiwan Semiconductor Manufacturing Corp. — better known as TSMC — described the U.S. government’s plans to reinvigorate the country’s chipmaking capacity as “a very expensive exercise in futility.”

The 92-year-old Chang turned TSMC into the world’s largest and most advanced semiconductor maker after starting the company in 1987. But he does not see a bright future for the CHIPS Act, the Biden administration’s signature legislation to build up U.S. chip production, saying that the $52.7 billion put aside for subsidies and other support will simply “not be enough.”

The way TSMC’s investments have since panned out suggests Chang’s skepticism may have been justified.

Long-running disputes with local employees, along with TSMC’s struggles with navigating how to secure government funding, have caused crucial delays to the company’s plans to invest $40 billion building two fabs near Phoenix, Arizona. TSMC’s current chairman Mark Liu recently said the first fab, initially announced in 2020, will not begin production until 2025, a year later than originally planned.

Liu blamed the delay on shortages of skilled workers needed to install sophisticated chip making tools and equipment. Indeed, like his predecessor, he believes that American workers need an attitude adjustment, if the U.S. is to compete in the fast-developing semiconductor chip industry.

While Chang has expressed perplexity at the notion of “work-life balance,” Liu has recommended that U.S. employees who can’t handle long shifts should find another industry in which to work.

Naturally, such sentiments have not gone down well with local unions. TSMC was simply making excuses to bring in lower cost Taiwanese replacements, Aaron Butler, the president of the Arizona Building and Construction Trades Council, has argued.

Other criticisms thrown at the company include its early decision to not sign a project labor agreement, underpaying its workers, and giving little heed to U.S. regulation and safety codes. Relations between TSMC and its disgruntled workers became so bad that U.S. tech giant Intel scooped up some of them to work on a fab it is constructing in a nearby town.

“One constituency that is very important to the current administration is organized labor,” says Willy Shih, a professor of management practice at Harvard Business School.

With very few investments overseas compared to Samsung, Toyota, and other globalized Asian companies, experts argue that the Taiwanese chipmaker is still grappling with the many risks of operating abroad.

Brian Harrison speaks to the Arizona Board of Regents on TSMC and Arizona’s ‘New Economy Initiative’, designed to bring new high-wage jobs to Arizona. Credit: @AZRegents via X

“TSMC is a culturally non-dexterous company. It hasn’t yet figured out how to do advanced manufacturing in the U.S.,” says Douglas Fuller, associate professor at the Copenhagen Business School (CBS).

“We do have some international experience and we continue to learn as we grow,” TSMC Arizona President Brian Harrison has said in response to criticism. The company did not respond to requests for comment for this article.

At the same time, U.S. government demands for subsidized projects to disclose confidential business information and share profits when cash flows significantly exceed projections have unnerved TSMC.

TSMC has been here before, as one of its only other foreign investments, into a chip facility in Washington state, never took off as planned. Albeit still profitable, Chang viewed the late 1990s venture as a “series of ugly surprises” due to mounting costs and disputes with business partners and local authorities.

And yet, despite the agonies it has undergone there and in Arizona, TSMC appears to be doubling down on its U.S. bet.

This month the Taiwanese company announced plans to raise its investment in the state — likely to be a fiercely contested battleground in this year’s elections — to $65 billion. Not only will it build a third plant at its site outside Phoenix by the end of this decade, but it will also produce what are currently the most cutting-edge chips measured at 2 nanometers or even smaller, next-generation processes (the lower the nanometer, or nm, count for a chip, the more advanced it is). The U.S. government has said it would provide $11.6 billion in direct grants and loans to support the massive, high-tech venture.

Clearly, the chip leader has a lot to offer American officials keen on diversification in advanced technologies.

But why is TSMC upping its bet on the U.S. — a country which, in Chang’s words, may only ever be able to produce “high-cost” and uncompetitive chips — when other advanced economies, from Japan to Germany, are also clamoring for semiconductor-related investment?

Taiwan’s mighty economic neighbor, China is key to the answer. The geopolitical threat created by Beijing’s recent actions and threats have created a confluence of interests between the U.S. and TSMC. In turn, they have done much to upend decades of economic thinking in Washington on the primacy of free markets, leading policy makers to once again embrace government-led industrial strategy.

Commerce Secretary Gina Raimondo responds to a question posed by Rep. Rich McCormick on chip production being concentrated in Taiwan, during her testimony to the House Committee on Science, Space, and Technology, September 19, 2023. Credit: C-SPAN

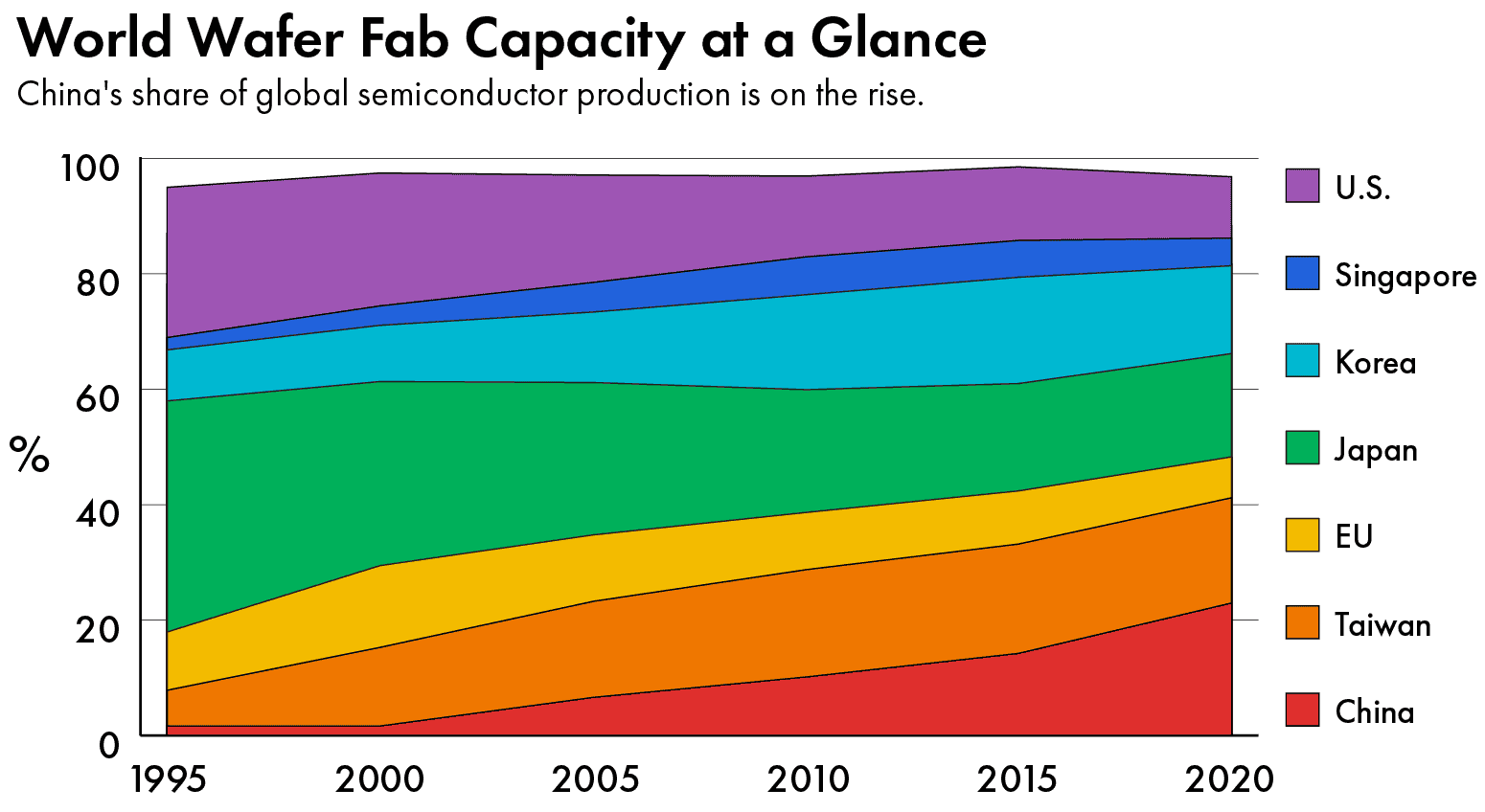

The Covid pandemic, which began in the Chinese city of Wuhan, brought home to chip suppliers and consumers just how risky the global supply chain had become, with its over-dependence on TSMC and Taiwan, now home to four-fifths of the world’s most advanced semiconductor production (7 nm and below). The U.S. Department of Commerce estimates that the global chip shortage knocked $240 billion off American GDP in 2021 alone.

China’s possible future military blockade or invasion of Taiwan, has propelled global policy-makers to attract investment for their domestic chip industries. TSMC and its Taiwanese peers have meanwhile been looking for places to diversify their manufacturing sites.

The hyper-concentration of high-end chip production in a single country means any military confrontation over Taiwan could seize up global manufacturing in digital and green technologies, such as smartphones and electric vehicles, which depend on integrated circuits to function. The disruption could cause a more than $2 trillion hit to the global economy, the Rhodium Group estimates.

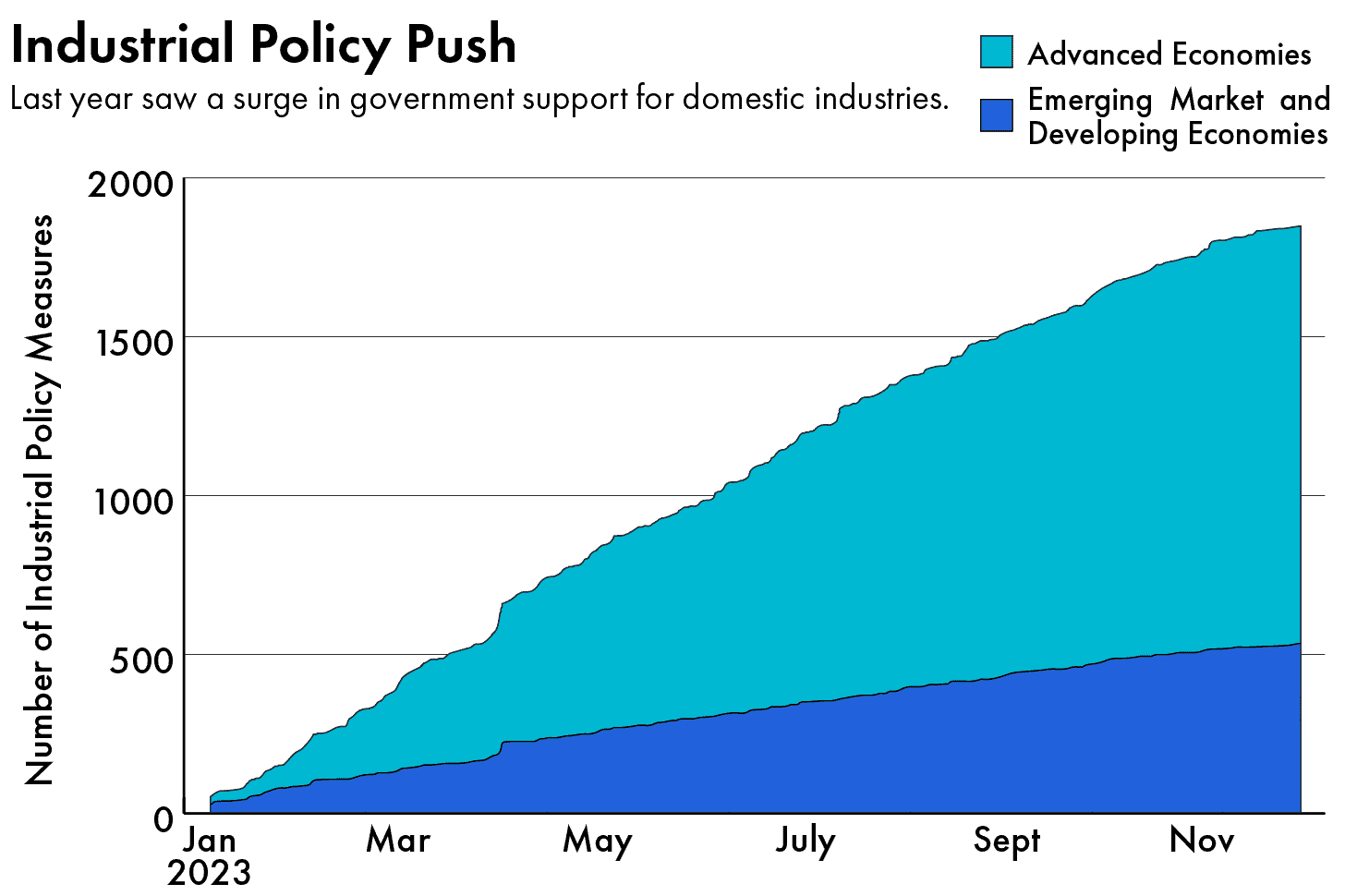

All this has focused views in major countries and regions, that large-scale industrial strategies are necessary. Even the International Monetary Fund, which has long espoused liberal market policies, and still warns governments to hand out subsidies with extreme caution, sees industrial strategy as justified in digital and green industries when it is well-designed, transparent and competition-enhancing, according to research published this month.

In the U.S. such thinking lies behind the CHIPS Act, which according to the Biden administration, attracted $166 billion in chip and electronics investment announcements in its first year.

One big question then is which country can best implement its policies to lower their dependencies on others and advance manufacturing in critical industries like semiconductors, which for years many were willing to cede to places like Taiwan.

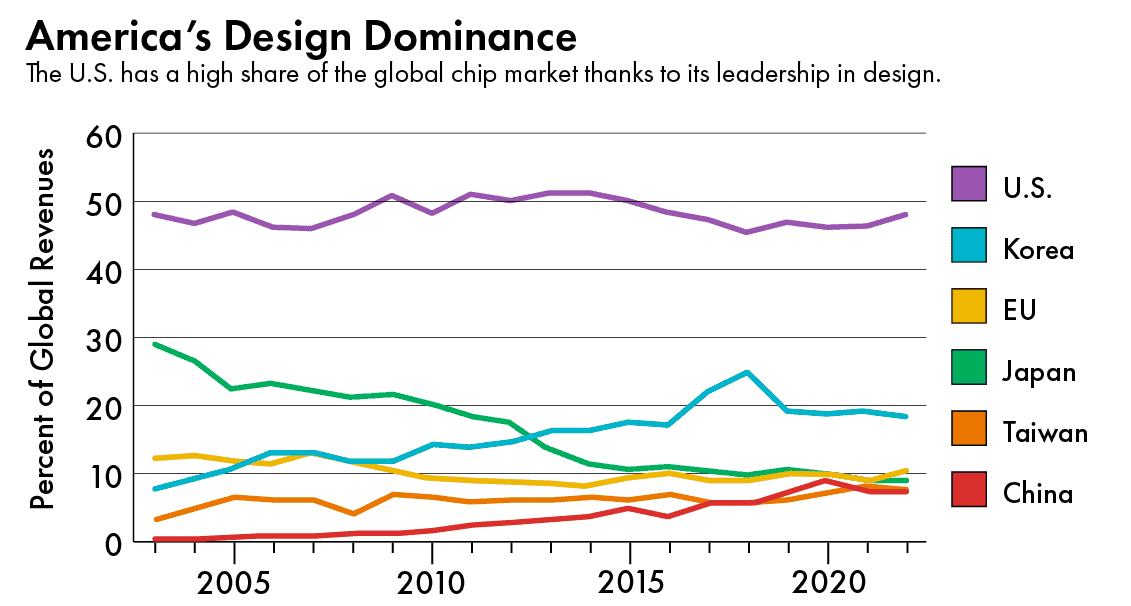

For sure, thanks to its leadership in areas like design, the U.S. chip industry still maintained nearly half of the global revenue market share by 2022, according to the Semiconductor Industry Association.

But despite the company’s recent announcements, the problems and delays at TSMC’s new Arizona plants show how the U.S. risks falling further behind its competitors in chip manufacturing. The country’s share of global capacity has fallen precipitously to around 12 percent. While Korean giant Samsung and Intel have been awarded billions in U.S. government support, they have also announced delays to their new fabs in Texas and Ohio respectively. They fault slow market growth, rising materials costs, and the drawn-out rollout of U.S. government subsidies.

What, then, is still proving so hard about making chips in America — and how can the U.S. fix it? For answers, the country can turn both to lessons from its past — and from the last country to threaten its mantle as the world’s leading economy.

SILICON SHOWDOWN

The current struggle for a slice of the global chip manufacturing cake has some echoes of the 1980s. This time around, the U.S. is using both state support and technology export bans to outcompete China and slow its advances.

Four decades ago, Washington’s target was Japan. By the end of its era of rapid economic growth, the East Asian country generated over half of global chip revenues. Led by companies such as NEC, Toshiba and Hitachi, Japan’s chipmakers dominated the market for memory chips in particular. In 1987, Toshiba engineer Fujio Masuoka invented the NAND flash memory chip, which could store large amounts of data long-term.

The Japanese semiconductor industry thrived due to its high productivity and strident quality control measures underpinned by a culture of continuous improvement.

Hideki Tomoshige, associate fellow at the Center for Strategic and International Studies (CSIS)

Japan’s dramatic economic and technological rise spooked the American establishment.

“We’ve seen the future, and it isn’t us,” a member of a U.S. congressional delegation to Japan warned after visiting a Toyota assembly plant in 1981. Lawmakers feared Japan was rapidly surpassing the United States in “high technology industries.”

American executives, such as Intel’s co-founder Robert Noyce, saw Tokyo’s industrial policies as empowering their Japanese rivals to engage in dumping in the U.S., while blocking American chipmakers from succeeding in Japan. But there was more at play.

“The Japanese semiconductor industry thrived due to its high productivity and strident quality control measures underpinned by a culture of continuous improvement,” says Hideki Tomoshige, associate fellow at the Center for Strategic and International Studies (CSIS).

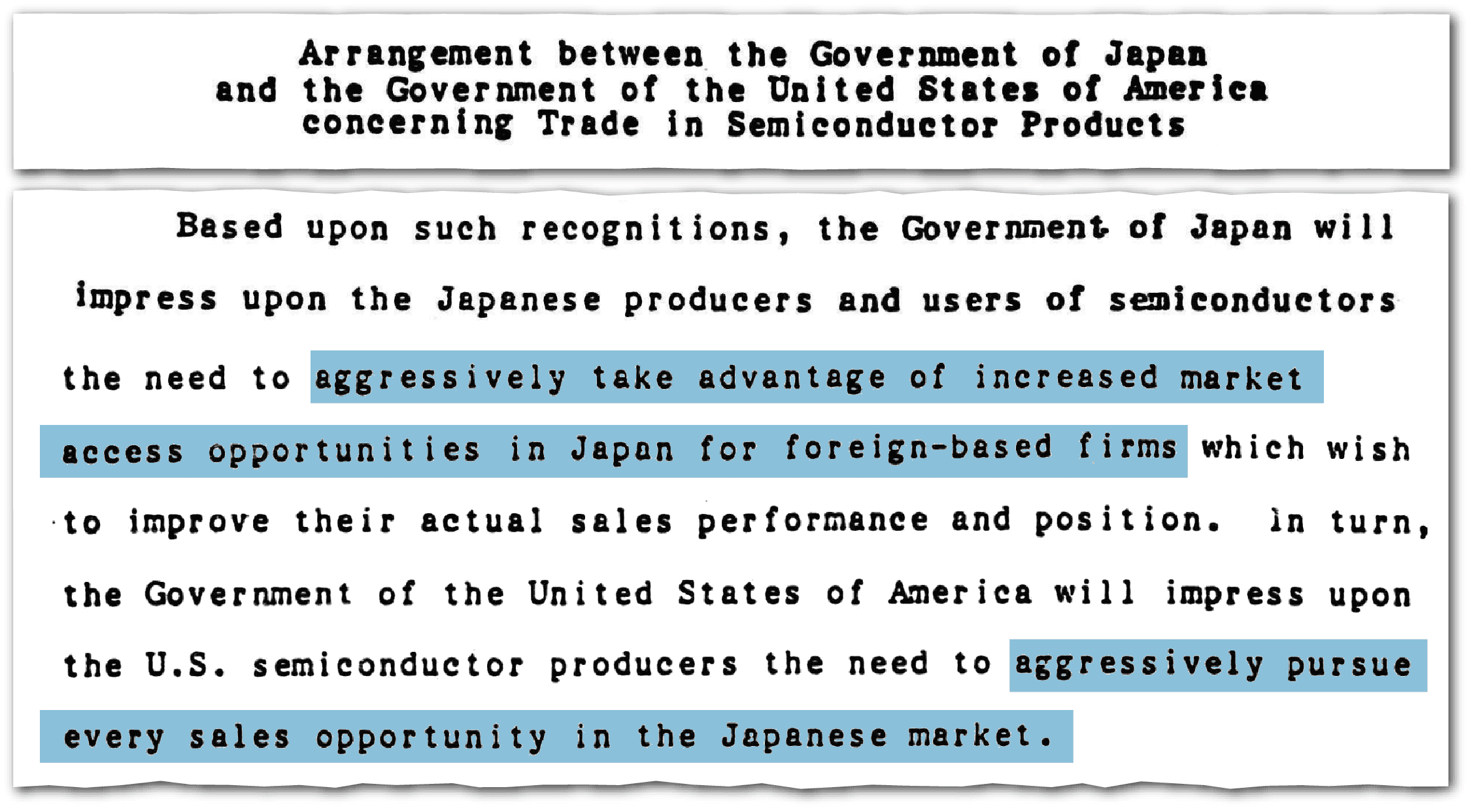

In response, Washington pressed Tokyo into the 1986 U.S.-Japan Semiconductor Agreement, which allowed the U.S. to set minimum prices for chips in the American market and compelled Japan to raise the domestic market share of foreign chipmakers. A year earlier, the Plaza Accord between the world’s leading economies had pushed Tokyo to revalue its currency, the yen.

Japanese chip industry veterans look back at U.S. pressure as a major trigger in their industry’s decline. However, Washington’s actions weren’t entirely responsible.

“Japan geared up its whole semiconductor industry to go after memory chips, but guess what? Wrong war. It was all about microprocessors and logic chips, then and now,” says Harvard’s Shih.

American rivals like Intel pivoted from memory to logic chips — essential inputs into personal computers, where sales were soaring.

Technological advances meanwhile kicked-off the so-called ‘fabless’ revolution. American start-ups, such as Qualcomm, Broadcom, and Nvidia, focused on chip design alone, while ‘pure-play’ specialized manufacturers, such as TSMC, emerged to direct the industry away from vertical integration. All the while, Korean memory chipmakers Samsung and SK Hynix beat the Japanese at their own game by producing more competitively-priced memory chips.

Japan remains a leader in chip-making lithography equipment and materials, but since 1995 its share of global chip manufacturing capacity has steadily declined by more than half to 18.5 percent (mainly in NAND memory and sensors), according to the European Semiconductor Industry Association. Neighboring Taiwan, South Korea, and most recently China, have taken hold over sizable portions of international production.

And after losing over 40 percent in global revenue market share since the late 1980s, Japanese policy makers now hope to exploit the country’s past to accelerate its future chip production.

The comeback is based in the southern region of Kyushu, which became known as ‘Silicon Island’ in the eighties. Back then, the area trailed only California’s Silicon Valley and Dallas, Texas as a regional chipmaking hub, taking advantage of its cheap electricity, skilled labor, and plentiful clean waters, an essential resource for chip production.

This February, TSMC opened its first fab on Japanese soil, near the rural town of Kikuyo in Kumamoto Prefecture, next to fields where farmers now grow rows of cabbages that are a vital ingredient in okonomiyaki, a popular Japanese pancake.

By the end of this year, the company will begin large-scale production at the $8.6 billion site, churning out mid-range chips between 12 and 40 nanometers, commonly used in consumer electronics and automotive applications.

“Japan’s semiconductor legacy from the twentieth century accelerated TSMC’s Kyushu investments,” says Kazumi Nishikawa, head of the Economic Security Office at the Ministry of Economy, Trade, and Industry (METI), a key figure in designing Japan’s semiconductor chip strategy. “We have the necessary infrastructure, human resources, education, and supply chains, but it is all getting older. We have one last chance to revitalize it.”

As Japan seeks to seize that chance, TSMC has already greenlit a second, $13 billion facility nearby that, beginning in 2027, will produce smaller, high-performance 6 and 7-nm chips used in higher-tech products like smartphones and 5G mobile networks. Discussions are underway over a third TSMC fabrication that could bring 3-nm chip production to Japan.

Other chip industry leaders are keen to enter the country.

U.S.-based Western Digital is partnering with Japanese memory chipmaker Kioxia on a new production line for advanced memory chips outside the industrial city of Nagoya. Idaho-based Micron Technology plans to open a memory chip fab in Hiroshima in the next few years, while TSMC’s Taiwanese counterpart, the Powerchip Semiconductor Manufacturing, will establish a chip plant in the northern Tohoku region. Over the coming five years, Samsung has said it will build out a packaging R&D facility in Yokohama.

Like the U.S., Japan’s government is providing billions of dollars to boost domestic chip production. Since establishing a special fund for its chips industry in 2021, it has set aside a total of $38 billion in strategic support. With government approval, chip projects in Japan can receive funds to cover up to half of their costs. TSMC’s fab was the first project to receive such backing in late 2021.

“There is a sense of urgency to secure the semiconductor supply chain,” says Nishikawa from METI.

Although it is smaller and less advanced than TSMC’s planned first fab in Arizona, with the Kumamoto fab already finished, Japan has pulled off an early victory in outpacing American reshoring efforts.

Standing shoulder-to-shoulder with Japanese industrialists and ministers at the February christening ceremony of its new facility, TSMC’s nonagenarian founder Chang said the moment marked “the start of a renaissance of semiconductor manufacturing in Japan.”

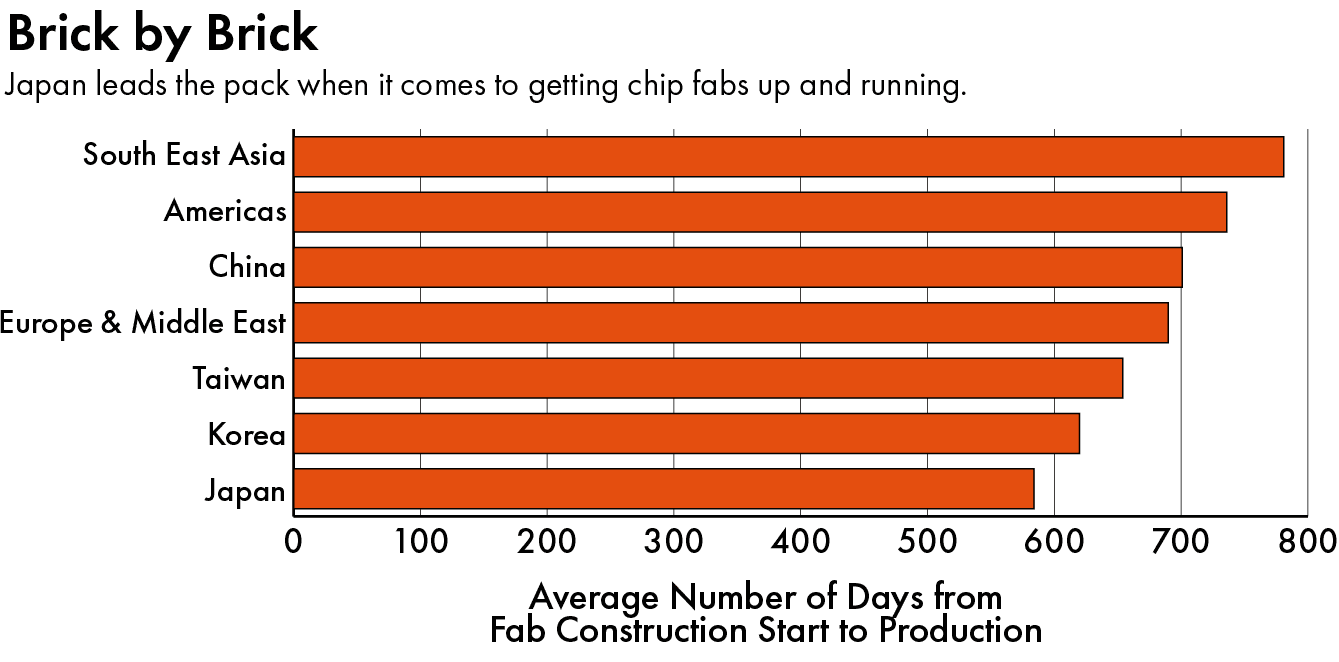

Certainly, Japan’s approach to building chip facilities stands out. A study by the Center for Security and Emerging Technology found that for new fabs constructed between 1990 and 2020, Japan led the way at 584 days on average compared to 736 days in the U.S. and the Americas.

For Chang-Tai Hsieh, professor at the University of Chicago Booth School of Business, the difference in construction speed comes down to contrasting work ethics and approaches.

“Did you notice what day of the week TSMC held its opening ceremony for the Kumamoto plant?” asks Hsieh. “It was a Saturday. And I suspect it was a deliberate effort by TSMC to send a message to the U.S. that they work 7 days a week, 24 hours a day.”

“Japan even took care of the minor details,” says Hsieh, relating how in Kumamoto local grocery stores started stocking Taiwanese food and Japanese schools began hiring Taiwanese teachers as TSMC workers arrived. “There’s been nothing like that thoughtfulness in the U.S.”

Others point to a more integrated approach in Japan between chip producers like TSMC and customers.

Japan was once the kingdom of the semiconductor. The Japanese government and industry felt they were out of the game in a technology that is essential for growth in the fourth industrial revolution,

Kazuto Suzuki, director of the Institute for Geoeconomics at the International House of Japan

Prominent American multinationals, such as Apple, have indicated — but not guaranteed — they will buy future U.S.-made chips from TSMC’s Arizona fab. But TSMC’s Japanese buyers such as auto giant Toyota, auto-part supplier Denso, and the Sony Group, are minority investors in the Kumamoto fab, and are integrating their operations with TSMC’s. Sony, for example, is building a camera image sensor facility next door to the new fab.

“In Japan, chipmakers like TSMC have more potential industrial customers to cultivate by expanding production facilities,” says METI’s Nishikawa.

To capture future semiconductor industry growth, a long line of major Japanese industrial companies and banks established the Rapidus Corporation in 2022. Backed initially by over $2 billion in subsidies from Tokyo, and led by two chip industry veterans, Rapidus aims to provide next-generation chip technology for AI and quantum computing. Set to open in 2027, it has already started constructing a 2-nm fab in Japan’s northern region of Hokkaido.

“Japan was once the kingdom of the semiconductor,” explains Kazuto Suzuki, director of the Institute for Geoeconomics at the International House of Japan. “The Japanese government and industry felt they were out of the game in a technology that is essential for growth in the fourth industrial revolution,” he says.

“This is a complete reshaping of the Japanese semiconductor industry,” Suzuki adds, describing the fast-paced developments underway across the country. “Investing in TSMC is just the beginning.”

MAKING INDUSTRIAL STRATEGY WORK IN AMERICA

The U.S. may not need to look as far as Japan for models of how governments can successfully promote important industries.

“When we think of industrial policy, we tend to look to the East Asian miracle. But for western economies there is a lot more to be learned from our own experience,” says Réka Juhász, assistant professor of economics at the University of British Columbia and co-founder of The Industrial Policy Group.

Juhász points to the Defense Advanced Research Projects Agency, or DARPA — established by the Eisenhower administration in the late 1950s — as a “textbook example” of industrial policy working in the U.S. political and economic context.

Best known for its impact on missile defense and stealth technology, the program also spurred the development of consumer technologies, such as GPS, personal computers, and the Internet.

Later, in the 1980s, then-U.S. President Ronald Reagan preached the gospel of free markets. But in practice his administration combined an assertive trade policy towards Japan with actively promoting the U.S.’s domestic chip industry. Antitrust laws were relaxed and the government provided hundreds of millions of dollars to fund a public-private research consortium called SEMATECH, to advance chip manufacturing.

Experts broadly agree SEMATECH succeeded in helping industry speed up innovation by fostering closer ties between chip device makers and equipment and material suppliers.

“At the time, the American semiconductor sector had a “throw it over the wall” problem where the people designing the chips didn’t really communicate with the people manufacturing them,” says Fuller from CBS.

“In its initial years, SEMATECH did a lot to improve manufacturing efficiency and make capital equipment makers more competitive with the Japanese ones,” he says. “It’s hard to imagine a U.S. comeback [then] without it.”

The U.S. chip industry regained the lead. And the debate on industrial strategy fizzled out, as free market orthodoxy became dominant through the 1990s and early 2000s.

“There was a mainstream idea that markets left to their own devices were the best way to ensure productivity and the government shouldn’t be trying to pick sectors and technologies to bet on,” says Juhász.

Yet most of America’s competitors have been more than happy to pursue industrial strategies, often going back many years. As a result, for U.S. policymakers, in chip manufacturing and a line of digital and green industries, it’s become a case of ‘if you can’t beat them, join them.’

“In a context where all the major players in the industry are willing to subsidize, if you decide not to, then you’re just going to lose relative market share,” says Fuller. “Industrial policy is warranted precisely because there are large externalities to overcome.”

Incumbent industry giant Taiwan recently passed a ‘Statute for Industrial Innovation’ to provide large tax deductions for its chip industry on top of its long-standing support. South Korea is providing renewed support to incentivize the reshoring of chip production through generous tax breaks in its so-called K-Chips Act. Even the European Union is mobilizing close to $50 billion to reinvigorate its chip supply chain.

Then, there is China, which has extended state support to its domestic chip industry for decades. In 2014, well before the Trump administration started targeting its chip industry, the Chinese government launched its so-called Big Fund, which over three phases has provided tens of billions in subsidies. Local governments have also provided firms with tax breaks, equity investments, and low-interest loans.

Chinese efforts are reshaping the industry. Almost half of the over 40 new fabs that will start operating this year globally are in China. Together, they will produce over 1 million wafers per month, according to research firm Gavekal Dragonomics.

The U.S. has attempted to crimp Chinese advances, in part by cajoling allies in Europe and Japan to help limit the export of technologies that are key to chip making processes, such as the extreme ultraviolet (EUV) lithography machines which produce the world’s most advanced microchips.

Still, Chinese firms have been able to overcome many of these obstacles. So-called “loose licensing” by the U.S. Commerce Department has allowed some exports to continue flowing. Combined with the resourcefulness of China’s chipmakers, this has opened up avenues for Chinese tech companies to produce advanced chips. Last year, telecoms giant Huawei stunned observers by producing a new smartphone, the Huawei Mate 60, that contains advanced 7-nm chips manufactured domestically.

“U.S. export controls are the most comprehensive in the whole world, but the enforcement mechanism is weak,” says Xiaomeng Lu, director of geo-technology at the Eurasia Group. “If the U.S. can’t do it effectively, what chance do Japan or the Netherlands have?”

Many Chinese chipmakers have focused on producing less advanced chips, measured at 28 nm or higher, which aren’t covered by U.S. trade restrictions. Such chips are still used widely in automobiles, consumer electronics, and industrial machines. China’s electric vehicle-makers, in particular, are plowing ahead with in-house chipmaking.

“Chinese companies are increasingly willing to switch to local suppliers,” says Gavekal’s Tilly Zhang. “This poses a challenge to foreign chipmakers of mature nodes.”

With other countries pushing ahead, the need for the U.S. to address flaws in its industrial strategy has become pressing. Critics of the CHIPS Act argue that its high costs and red tape, alongside workforce issues in the U.S., will continue to impede Washington’s reshoring efforts. In the short-run, TSMC still needs to finalize terms for the recently announced, but still “non-binding and preliminary,” agreement with the Commerce Department.

“The regulation system has so many veto points that both Republicans and Democrats, and even progressives, realize it is a problem,” says Fuller.

Steven Vogel, a professor at the University of California, Berkeley acknowledges that American industrial policy faces the constraints of a fragmented political system. “There is no METI in the United States,” referring to the power Japan’s powerful ministry wields.

…it’s a very complicated game. It is not just competition against China. It is one between friends in the U.S., EU, Japan, and Korea. How can we coordinate in the supply chain?

Shigeaki Shiraishi, a senior research fellow at the Nakasone Peace Institute in Tokyo

“But the U.S. is not incapable of a coherent and effective industrial policy,” Vogel adds: Operation Warp Speed, the effort to accelerate Covid-19 vaccine development and deployment, provides a recent example of a highly successful U.S. industrial policy.

Washington must act as a coordinator of investment efforts that fulfill public interests, such as the clean energy shift and supply chain resilience, that the private sector will not meet alone, he argues.

Others see specific ways that tweaking the CHIPS Act could help ramp up U.S. chipmaking.

Harvard’s Shih, who is also an advisor to the Commerce Department on the CHIPS Act, says the legislation helps on the so-called ‘supply side’ — providing grants and loans to manufacturers. But he adds that the U.S. could do more on the ‘demand side’ — which might involve tax credits for consumers and government procurement plans for domestically produced chips.

“If you look at TSMC in Kumamoto, and its partnership with Sony, Denso, and Toyota, those are customers that are going to take the chips,” he says. “If chipmakers are going to put so much money in the ground in the U.S., they need some way to assure high utilization. We need one side pushing and one side pulling.”

Despite U.S. plans to provide the Taiwanese chipmaker with billions in support, TSMC’s chief executive, C.C. Wei, nonetheless recently commented that the company expects its customers to share the higher cost of operating fabs overseas.

A further step the U.S. could take is to increase cooperation with like-minded countries. A strategic partnership with IBM is a big part of Japan’s Rapidus plans to develop new semiconductor technology.

Still, says Shigeaki Shiraishi, a senior research fellow at the Nakasone Peace Institute in Tokyo, “it’s a very complicated game. It is not just competition against China. It is one between friends in the U.S., EU, Japan, and Korea. How can we coordinate in the supply chain? Which country should do what?”

Even if the United States and Japan successfully reshore sizable chipmaking activities, the semiconductor industry will likely remain one of complex global supply networks criss-crossing multiple continents. From design and development to the raw materials and lithographic equipment necessary for chip fabrication, a long line of countries play active roles in the industry.

Whether American political and corporate leaders like it or not, the global economy has entered a new stage where industrial strategy will matter more in determining progress and competitiveness. The effectiveness of government intervention in leveraging resources for strategic sectors will shape the future contours of global business and new technologies.

To many, industrial policy may remain an enigma. But the global semiconductor industry has rarely been guided by the market alone. Western policymakers may bemoan entering subsidy races with one another. But they cannot turn away from the stark reality that the use of industrial policy is well-entrenched in their own national histories and a near-permanent feature of the international political economy.

“The idealized version of free trade only works when everybody is playing by the same set of rules,” says Shih. “But the problem is people aren’t.”

Luke Patey is a senior researcher at the Danish Institute for International Studies. He is author of How China Loses: The Pushback Against China’s Global Ambitions. His work has been published in The New York Times, Financial Times, The Guardian, The Hindu, Foreign Affairs and Foreign Policy. @LukePatey

{kind=link}