Hong Kong is on its back heels. Its economy has been floundering. Its stock exchange has been mired in a wrenching bear market. There has been a major exodus of talent. It is caught in the crossfire of the U.S.-China conflict. And its political strings are under the ever tighter control of its masters in Beijing. A perfect storm shows no sign of abating.

For those of us personally attached to Hong Kong, the recent confluence of adverse developments has been especially painful to watch. I cried out recently in the editorial pages of the Financial Times and again in the South China Morning Post that Hong Kong, as we once knew it, was “over.” I will be the first to confess that this plea hasn’t gone over very well with many of my good friends in the city that I once lived in and still love. Nor has it gone over very well in Beijing; at the recent China Development Forum, where I had spoken for 24 consecutive years as the longest attending foreign participant, I was banished to the sidelines, informed that my views were too “sensitive” for public airtime.

Amid the furor, it is important not to lose sight of the crux of the problem: As the Chinese economy goes, so goes Hong Kong. It follows that any resurrection of Hong Kong would require one of two things — a significant rebound of the Chinese economy or a special strain of Hong Kong resilience.

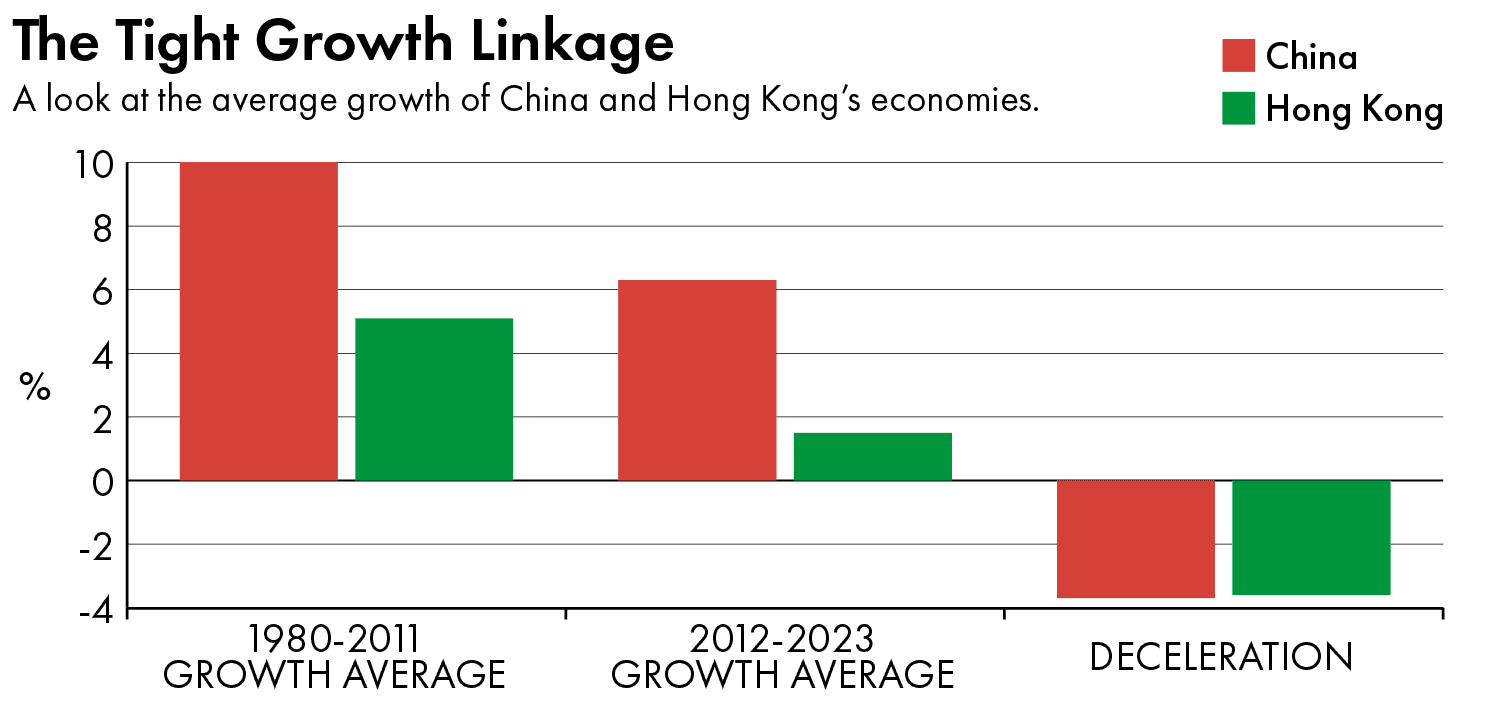

The tight linkage between the mainland and Hong Kong economies is undeniable. Over the past twelve years to 2023, the Chinese economy has grown by an average of 6.3 percent annually, a 3.7 percentage point deceleration from the spectacular 10 percent pace of the preceding thirty-two years from 1980 to 2011. Over the same recent twelve-year time frame from 2012, the Hong Kong economy has grown just 1.5 percent — a deceleration of 3.6 percentage points from the 5.1 percent pace from 1980 to 2011.

Coincidence? Not by any stretch of the imagination. The growth deceleration of both the Chinese and Hong Kong economies has been virtually identical over the past dozen years. This makes perfect sense in light of increasingly tighter cross-border integration through trade flows, financial flows, and tourism. The Hong Kong economy has effectively been swallowed up by the mainland economy — hook, line, and sinker.

A further slowdown in the Chinese economy raises the distinct possibility that there will be further downside risk to Hong Kong economic growth in the years ahead.

There is an important twist to this story: Surprisingly, the forecasting community currently believes that the future for Hong Kong will be rosier than that of the Chinese economy. The International Monetary Fund’s latest baseline forecast calls for economic growth in Hong Kong to accelerate to an average of 2.7 percent per year over the next five years to 2028. That would be a near doubling from the sluggish 1.5 percent pace of the past twelve years.

This is expected to occur despite IMF projections of a further slowing of Chinese economic growth to 3.8 percent on average over the next five years. In other words, IMF forecasters are defying the historically tight linkage, and buying the seemingly unlikely case for Hong Kong economic resilience; they are looking for a strengthening of 1.2 percentage points in GDP growth over the next five years against the backdrop of a 1.3 percentage point deceleration in Chinese economic growth.

This makes no sense. Something has to give. There will have to be either a resurgence of Chinese economic growth, or the Hong Kong economy will slow further rather than strengthen as the IMF expects. The problem is not with the IMF’s China call. The overly indebted Chinese economy is facing stiff cyclical pressures in the property sector and local government finances, that are likely to be reinforced by ongoing structural problems associated with a shrinking workforce and powerful productivity headwinds. The lack of a productivity offset to unrelenting demographic distortions stemming from the legacy effects of one-child family-planning policies is likely for two reasons: a shift in the structural growth mix to low-productivity state-owned enterprises, and ongoing regulatory restraints on the higher-productivity private sector, especially Internet platform companies. If anything, the IMF’s baseline forecast of 3.5 to 4 percent Chinese economic growth over the next five years may turn out to be too optimistic.

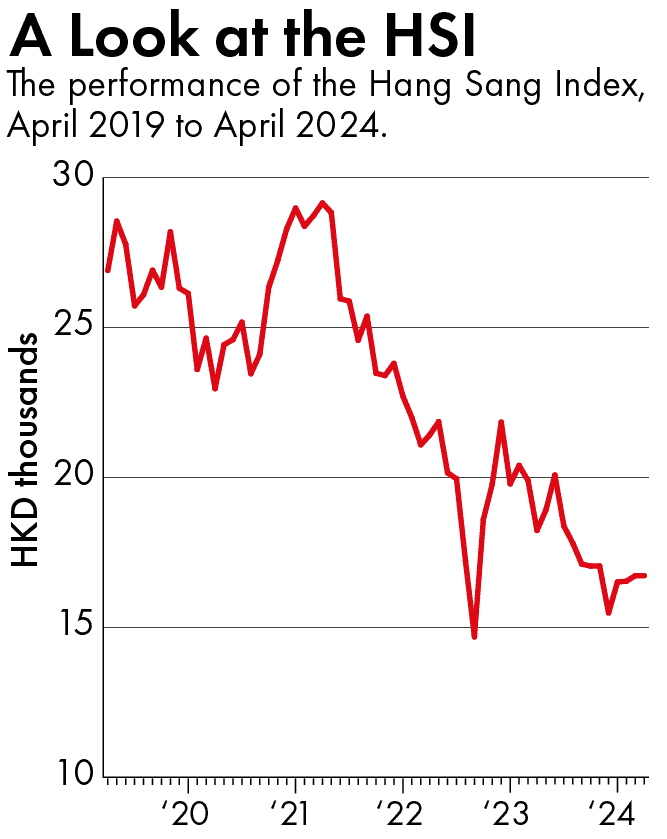

A further slowdown in the Chinese economy raises the distinct possibility that there will be further downside risk to Hong Kong economic growth in the years ahead. This has not been lost on the Hong Kong equity market, where a powerful bear market correction has already taken the Hang Seng Index (HSI) back to levels prevailing at the time of the handover from Great Britain to China in July 1997. While an oversold HSI has now bounced by 12 percent off its depressed January 2024 lows, it is still down some 45 percent from its February 2021 highs.

Of course, I could be wrong, and Hong Kong could stage another one of its legendary Phoenix-like recoveries that has long defied its most notorious doubters. This touches on the biggest pushback to my recent commentary on Hong Kong — that I am overlooking its enduring resilience. Fair point, but it is important to recognize that today’s case for resilience is much different than it was at prior testing points, such as the Asian Financial Crisis, the Global Financial Crisis, or even the outbreaks of SARS and Covid-19. In all of those earlier cases, Hong Kong was able to benefit by drafting off the strength of the mainland economy. That is not the case today.

Hong Kong’s dynamism, its energy, and its political independence are now fading quickly… The case for Hong Kong’s special resilience is in tatters.

Sure, there are other possible sources of resilience to consider, but my main table-pounding point is that they will need to be very powerful to offset the drag from sluggish Chinese economic growth in the years ahead. The math is compelling: If the historical linkage between growth in China and Hong Kong were to hold, China’s coming deceleration of 1.3 percentage points over the next five years would imply a slowing to just 0.2 percent average growth in Hong Kong over that same period. Consequently, Hong Kong would need to uncover about 2.5 percentage points of additional growth — the resilience factor — in order to hit the IMF’s optimistic 2.7 percent baseline forecast.

That is a tall order, to put it mildly. Moreover, the China slowdown is not the only headwind facing Hong Kong. The adverse consequences of the U.S.-China conflict — especially America’s friend-shoring campaign that puts pressure on Hong Kong trade with China, its largest trading partner — compounds the problem. Similarly, the recent brain drain of foreign professionals now departing Hong Kong in the aftermath of the massive demonstrations of 2019 is like a dagger in the heart of the city’s greatest asset — its talent pool.

That, of course, draws attention to yet another elephant in the room — the post-2019 shift in Hong Kong’s domestic political framework. Following the hugely disruptive demonstrations of late 2019, Beijing wasted no time with swift enactment of new national security restrictions on Hong Kong. And now, less than four years later, Hong Kong’s Legislative Council has taken unanimous action of its own to align its domestic rule of law under Article 23 of its Basic Law with Beijing’s earlier edict. Economies need political autonomy to craft policies that address tough problems such as a major slowdown in economic growth. But with powerful political winds blowing in from Beijing, Hong Kong is now further away from being able to independently exercise that optionality.

By process of elimination, that draws attention to China’s new urban agglomeration construct — the Greater Bay Area (GBA) — as Hong Kong’s greatest hope. Don’t count on it. So far, no discernible growth differential has opened up between the GBA and the rest of China. Over time, that may change. The most optimistic estimates I have seen put incremental GBA gains at one percentage point above overall growth in the Chinese economy. Additionally, these estimates usually presume that it will take considerable time — at least until 2030 — for the full extent of that incremental gain to be realized. In the meantime, with Hong Kong significantly over-shadowed by its GBA partners of Shenzhen and Guangdong, both in terms of scale and more diverse economic bases, it is hard to make the case that Hong Kong will lead the GBA in providing a new strain of resilience that will defy the broader China slowdown. If anything, with Hong Kong’s political winds shifting and its talent pool dwindling, it is quite conceivable that it lags the rest of the GBA and, as many have argued, gets increasingly marginalized as just another large Chinese city.

In the end, the very real struggles of Hong Kong are not about to vanish into thin air. Yes, the once durable resilience of this wonderful city is etched in its historical role as the major trading entrepôt of Canton. Those days are not altogether over. But Hong Kong’s dynamism, its energy, and its political independence are now fading quickly. With China unlikely to regain its once powerful economic momentum, Hong Kong should follow suit. The case for Hong Kong’s special resilience is in tatters.

Stephen Roach, senior fellow of the Paul Tsai China Center of Yale Law School, is the former chairman of Morgan Stanley Asia and author of Accidental Conflict: America, China, and the Clash of False Narratives (Yale University Press, 2022).