An avalanche of cheap minerals originating from Chinese producers is thwarting Western governments’ hopes of fighting back against China’s dominance over the electric vehicle supply chain.

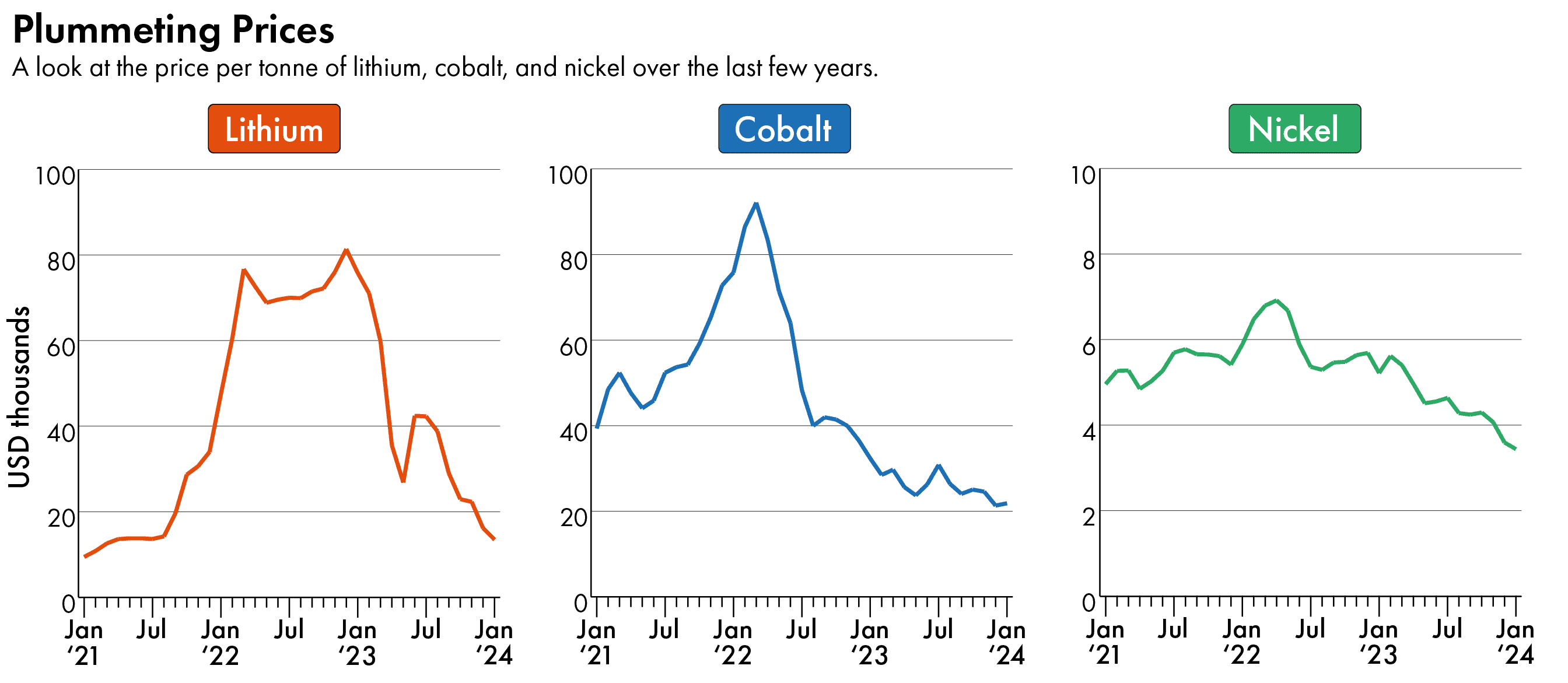

Since last year, the prices of metals vital to battery making have slumped: lithium is down by more than 80 percent, while nickel and cobalt have both tumbled over 40 percent. In response, miners from Canada to Australia have been forced to pull back on investment plans, cut production and initiate layoffs.

At a time when Beijing has shown its willingness to wield the country’s dominance over metals for political leverage — it imposed controls on the export of germanium, gallium and graphite last year in retaliation against U.S. export controls on high-end semiconductors — this pull back is alarming Western government officials.

Last week, Ashley Zumwalt-Forbes, deputy director for batteries and critical minerals at the U.S. Department of Energy, described the situation in the nickel market as “dire” and “an extreme threat to national [and] international security as well as the environment.”

“We as an industry and as governments need to strategize how we can prevent these kinds of mass closures both now and in the future as a matter of national and international security. We urgently need supply chain diversity,” she wrote in a post on LinkedIn.

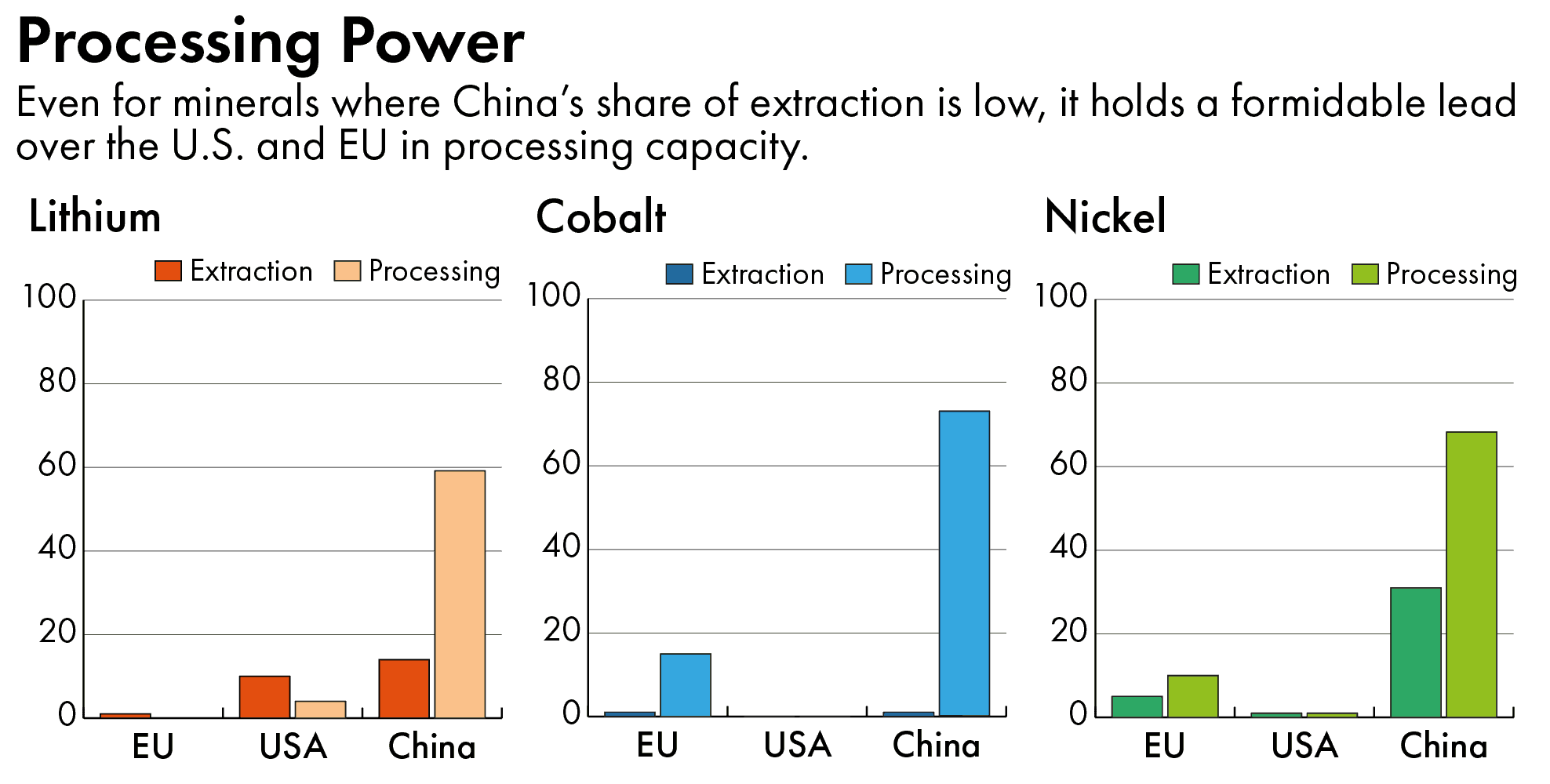

Slowing global EV sales are partially to blame for the surplus, but experts say a much larger issue is overproduction by Chinese companies. Chinese producers account for about one-fifth of global lithium production, but more than half of lithium processing. With nickel, much of the extraction and processing takes place in Indonesia but is managed by Chinese-owned firms.

Recently, Chinese producers have been flooding the lithium market with lepidolite, a low-grade lithium ore few miners outside China have historically considered worth pursuing due to its low yield. A wave of nickel supply from Indonesia is driving down prices for the metal used in EV batteries and stainless steel. Cobalt has also plunged on the back of accelerating production in Indonesia and the Democratic Republic of the Congo (DRC), where China’s CMOC Group dominates.

“Chinese investors have a very different attitude to their mining investments compared to Western investors,” says Martin Jackson, head of battery raw materials at CRU Group, a mining intelligence provider. “The Chinese investors don’t seem to be backing down even in a low price environment, even those that own quite high-cost production facilities.”

Exuberance may be one factor leading Chinese companies to over-produce: “There are many examples where investor frenzy has resulted in overcapacity, and sometimes the Chinese government has had to weigh in,” says Jackson. There are also strategic considerations: by forcing down prices, large Chinese firms are able to squeeze smaller competitors out of the market.

…there are a lot of clever lawyers telling people about workarounds and mineral laundering schemes. And the rules do have some loopholes.

Todd Malan, chief external affairs officer for Talon Metals, an American nickel miner

Meanwhile, a long list of Western mining firms have announced cutbacks. Earlier this month, Wyloo Metals, owned by Australia’s second richest man Andrew Forrest, announced it was shutting down its nickel operations. Also this month, First Quantum, a Canadian miner, told investors it would cease production at its Australian nickel and cobalt mine and cut a third of its workforce. Even U.S.-headquartered Albemarle, the world’s largest lithium producer, laid off about 300 people this month, as first reported by The Information.

Chinese companies are feeling the heat from lower prices as well. Tianqi Lithium and Ganfeng Lithium, two of the world’s largest lithium producers, issued profit warnings earlier this week; their shares have fallen by more than 50 and 70 percent, respectively, over the last year. That has not deterred Ganfeng from seeking to top up its reserves: it reached an agreement earlier this month with Australia’s Pilbara Minerals to double its purchase of lithium ore over the next three years.

For U.S. officials, the cuts in Australia are worrying because the country is one of the most promising sources of raw materials from both an environmental and trade standpoint. EVs that use battery metals sourced from Australia are more likely to be eligible for tax credits under the 2022 U.S. Inflation Reduction Act (IRA), thanks to a free trade agreement between the two nations.

The IRA was supposed to be a shot in the arm for Western miners, encouraging more investment both in the U.S. and in friendly jurisdictions. Ramping up production in countries like Australia and Canada remains vital if countries are to hit their zero emission vehicles targets over the next decade. But the current level of prices is discouraging long-term investments: a lithium mine can take up to three to seven years to build and bring to full production.

“If we look at the pipeline for both mines and refineries, even in a fairly optimistic scenario we’re going to be entering a pretty severe deficit from the late 2020s onwards,” says Will Talbot, principal analyst for nickel and cobalt at Benchmark Mineral Intelligence. “Based on that outlook, you could certainly ask why there isn’t more investment. But for western investors, they see the price now as the most important thing.”

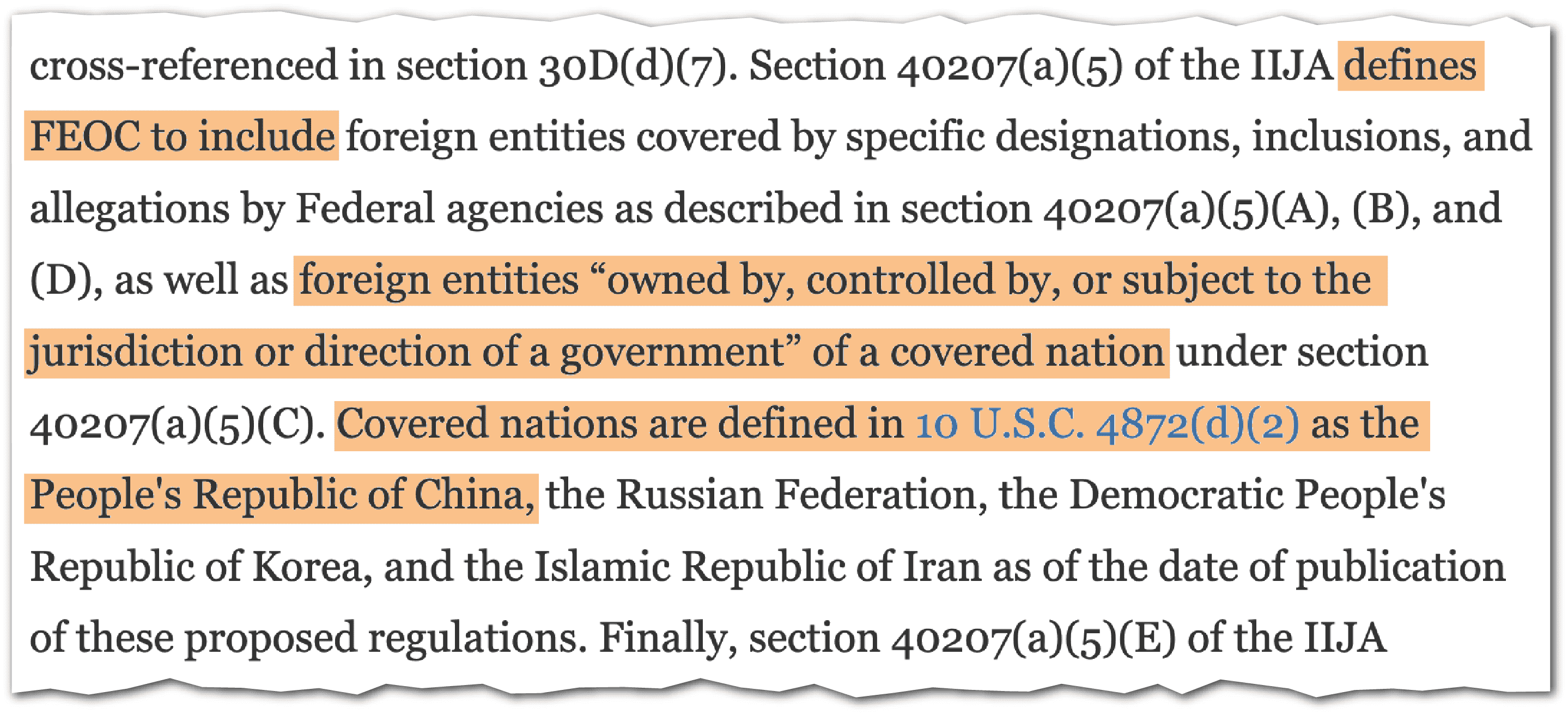

Experts point to lingering doubt about how strictly the IRA will be enforced as one issue for miners. Starting in 2025, the IRA will prohibit EVs containing critical minerals extracted, processed, or recycled by “foreign entities of concern” (FEOCs) from qualifying for tax credits of up to $7,500, a condition intended to keep Chinese suppliers out of the U.S. EV supply chain.

The Treasury Department clarified its FEOC definition in draft guidance in December, but some loopholes remain. It’s not fully clear, for example, whether the new rules will end up excluding metals extracted by privately-owned Chinese companies involved in joint ventures overseas — a common arrangement for nickel miners in Indonesia.

Some Chinese companies have sought to get around the restrictions by setting up joint ventures in countries with free trade agreements with the U.S.. China’s Huayou Cobalt has partnered with South Korea’s LG Chem on a lithium refinery and cathode material plant in Morocco. Shenzhen-based GEM Co., a leading battery recycler, is working with South Korean firms SK On and EcoPro Materials on a $900 million battery ingredient factory in Korea.

“To be brutally honest, there are a lot of clever lawyers telling people about workarounds and mineral laundering schemes. And the rules do have some loopholes,” says Todd Malan, chief external affairs officer for Talon Metals, an American nickel miner.

Left: Executives from LG and Huayou Group at an MOU signing ceremony marking plans to build a lithium phosphate iron cathode materials plant in Morocco, September 22, 2023. Credit: LG

Right: Executives from SK On, GEM Co., and EcoPro at a signing ceremony for a battery core material production facility in Saemangeum, South Korea, March 24, 2023. Credit: SK On

Some in the industry envisage that protectionist legislation like the IRA could eventually carve the global market for key metals into two: one which prices in the extra costs of IRA compliance and meeting certain ESG criteria, and one for the rest.

Right now, “the minerals industry is somewhat hampered by a global price,” says Malan. A higher price for IRA-compliant materials could incentivize Western miners to invest more in extraction and downstream processing.

With stricter IRA enforcement… we may start to see a bifurcation in the nickel market. But in the short term there’s no real evidence of that…

Will Talbot, principal analyst for nickel and cobalt at Benchmark Mineral Intelligence

“What the industry needs to do is a little self help, and start to say we’re going to price in these qualitative factors,” Malan adds.

To get there, however, analysts say regulators will need to do more to ringfence the market, including by addressing some of the loopholes in the FEOC definition.

“With stricter IRA enforcement… we may start to see a bifurcation in the nickel market,” says Talbot. “But in the short term there’s no real evidence of that; the shutdowns of these Australian sites, which are arguably better from an ESG perspective, show the market is not ready yet for that premium, it just cares about the price.”

Eliot Chen is a Toronto-based staff writer at The Wire. Previously, he was a researcher at the Center for Strategic and International Studies’ Human Rights Initiative and MacroPolo. @eliotcxchen