Gregory C. Allen is the director of the Wadhwani Center for AI and Advanced Technologies at the Center for Strategic and International Studies (CSIS). He is one of the most influential analysts in Washington on the U.S.’s export controls on high performance semiconductor technology to China. Most recently, he authored two new reports: one on the implications of Huawei’s new smartphone for the future of export controls, and another on allied perspectives on U.S. export control policy. In this lightly edited Q&A, we discuss the significance of the landmark October 7th 2022 export control policy and its shortcomings, the October 2023 update of that policy, China’s indigenous chipmaking capabilities, and the long-term prospects for America’s multilateral approach to chip controls.

Illustration by Kate Copeland

Q: You’ve previously described the October 7th, 2022 export controls as a paradigm shift for U.S. technology policy toward China. Why is that?

A: In one sense, the October 7th export controls were narrowly targeted. They limited the export to China only of semiconductors for training advanced AI models in data centers and for supercomputing applications, as well as for the equipment needed to make those chips. We’re talking about a percentage point or so of the global semiconductor market in terms of chip sales.

However, the underlying logic of the export controls and the way they were implemented represented a reversal of decades of trade and technology policy toward China. The goal of the policy was not just to slow the pace of China’s technological advancement, which has been a goal of U.S. technology policy for decades, but instead to actively seek to degrade China’s semiconductor manufacturing capability, by cutting off access to spare parts for existing equipment that is already in Chinese facilities.

| BIO AT A GLANCE | |

|---|---|

| AGE | 35 |

| BIRTHPLACE | Kansas City, Kansas, U.S. |

| CURRENT POSITION | Director of the Wadhwani Center for AI & Advanced Technologies at the Center for Strategic and International Studies (CSIS) |

In addition, many of the new export controls were applied on a China-wide basis, not on the traditional basis which had been restricting exports to companies or individuals on the Entity List, or to military end users and end uses. The new export controls on advanced AI chips applied to China as a whole, as did some of the semiconductor equipment sale restrictions. So it was a very big turning point in the U.S.-China trading relationship, even though there are some earlier antecedents you can point to.

At the same time, the intention of the October 2022 controls was to limit China’s future technological capacity, as opposed to cutting it off at the knees now, right?

Right. So the title of my original analysis of the October 7 export controls was “Choking Off China’s Access to the Future of AI,” not “crushing China immediately in AI.” I think that’s an accurate description of where the technological boundaries were drawn, at least in the original October 7th controls, which corresponded to the technological state of the art circa early 2020, thereby freezing chip sales to China at that level.

Fast forward to this September, right at the time that Commerce Secretary Gina Raimondo was in China, Huawei debuted its new flagship phone, the Mate 60, with capabilities that exceeded what many people assumed China could produce indigenously, including 5G connectivity and a 7 nanometer (nm) chip made by China’s Semiconductor Manufacturing International Corp (SMIC). How did you view that development?

| MISCELLANEA | |

|---|---|

| FAVORITE BOOK | The Dark Forest by Cixin Liu |

| FAVORITE MUSIC | Synth pop |

| MOST ADMIRED | Theodore Roosevelt |

The Huawei phone announcement really does have to be understood as a deliberate slap in the face to Secretary Raimondo. Huawei is the head of a Chinese public-private team. And so Huawei is not going to take actions like this without the full backing of the Chinese government. And indeed, Chinese state-owned media was effusive in its praise of Huawei for doing this.

In terms of what it meant for U.S. export controls, there is one assumption in the October 7th controls that was explicitly challenged by Huawei and SMIC’s success in producing this phone. SMIC had already been able to produce 7nm chips in July 2022. They already had all of the equipment in China working inside their fabs prior to October 7th 2022. However, the October 7th controls were designed to cut off SMIC’s access to spare parts and maintenance services — all of the post-sales support that you need.

Credit: 微机分WekiHome

The fact that SMIC was able to not only keep the fab running, but make technological progress, really challenged the assumption underlying the policy that loss of access to spare parts was going to force SMIC to shut down or radically scale back its production capacity. That’s actually still the working assumption of leadership in the Biden administration. Undersecretary of Commerce Alan Estevez restated his confidence in this happening just a few weeks ago. And I will say, if that’s going to work, it’s going to depend upon making these export controls considerably more multilateral.

You would need Korea, especially, to come on board, because Korea has been an important source of spare parts for these machines. And you would also need third party distributors to crack down on diversion of spare parts to prohibited companies and facilities. It’s reasonably easy to know which facility your massive semiconductor manufacturing equipment goes to. It’s considerably harder to know whether spare parts and components actually end up at the facility that they were contractually obligated to go to. That’s going to require additional tracking and enforcement of distribution networks in China, and China is obviously not incentivized to make that easy.

It sounds like in your view the October 7th policies were not stringent enough to realize the U.S.’s goals.

The first thing to understand is that you can have a relatively consistent, logical policy of selling most everything to China. The logic of that policy is that it maximizes U.S. firms’ revenue, and it maximizes the extent to which those profits can then be plowed back into companies in order to maintain U.S. technological leadership.

To the extent that China is seeking to eliminate U.S. firms from their supply chain, we should not assist them in that endeavor by selling them some technology and restricting others.

There’s also the opposite approach which is to sell very little, almost nothing to China, in order to deny China the tools with which to de-Americanize their supply chain. To the extent that China is seeking to eliminate U.S. firms from their supply chain, we should not assist them in that endeavor by selling them some technology and restricting others.

Both of those policies, although very different, have an internally consistent logic. The policy for which there is no internally consistent logic is to constantly signal to China an intent to prevent it from advancing technologically without actually denying them the tools to succeed in their de-Americanization strategy. That policy is the worst of all possible worlds. You incur all the costs in terms of incentivizing China to de-Americanize without actually incurring the benefits of preventing China from de-Americanizing.

I think the original October 7 export controls — and much of what the Trump administration did before that — had that de facto effect. Much of the equipment that the U.S. government didn’t want China to access ended up getting sold to China anyway, while the signaling was plenty scary enough to persuade China to accelerate their already extensive de-Americanization effort.

I do want to emphasize that much of that criticism is especially true of the Trump administration. Much of the de-Americanization effort in China was already fully underway, to the tune of tens of billions of dollars, in 2018 and 2019. Just to give one example, YMTC [Yangtze Memory Technologies Corp], which is the most advanced Chinese flash memory provider, had 800 employees working full time on de-Americanizing their supply chain in 2019, three years before the October 7th 2022 export controls. The point is, if you’re going to try and plug the leaks in an extensive export control policy, it really matters that you get that right and that you respond quickly to identify gaps.

Some critics charge that the reason China has managed to stay on the cutting edge is because the Commerce Department has been too permissive about approving licenses for the sale of export controlled technology. What do you think?

The rebuttal that folks at Commerce would give is that there’s not much point in restricting the sales of U.S. equipment if there are foreign companies also making that equipment located in countries where the government does not intend to restrict their sales. One explanation the Commerce Department could make is they were waiting for the multilateral deal with the Netherlands and Japan as the appropriate moment to actually start putting that kind of pressure upon China.

Commerce Secretary Gina Raimondo discusses the recent export controls at the Reagan National Defense Forum, December 2, 2023. Credit: Reagan Foundation

At the same time, it can also be true that the Commerce Department has in previous years designed regulations that are leaky and also has been permissive in granting licenses. But it doesn’t inherently follow that if the U.S. had simply been much more restrictive in granting licenses, then it would have achieved the strategic impact that these individuals want. In order to achieve those strategic impacts, the export controls do need to be multilateral in nature.

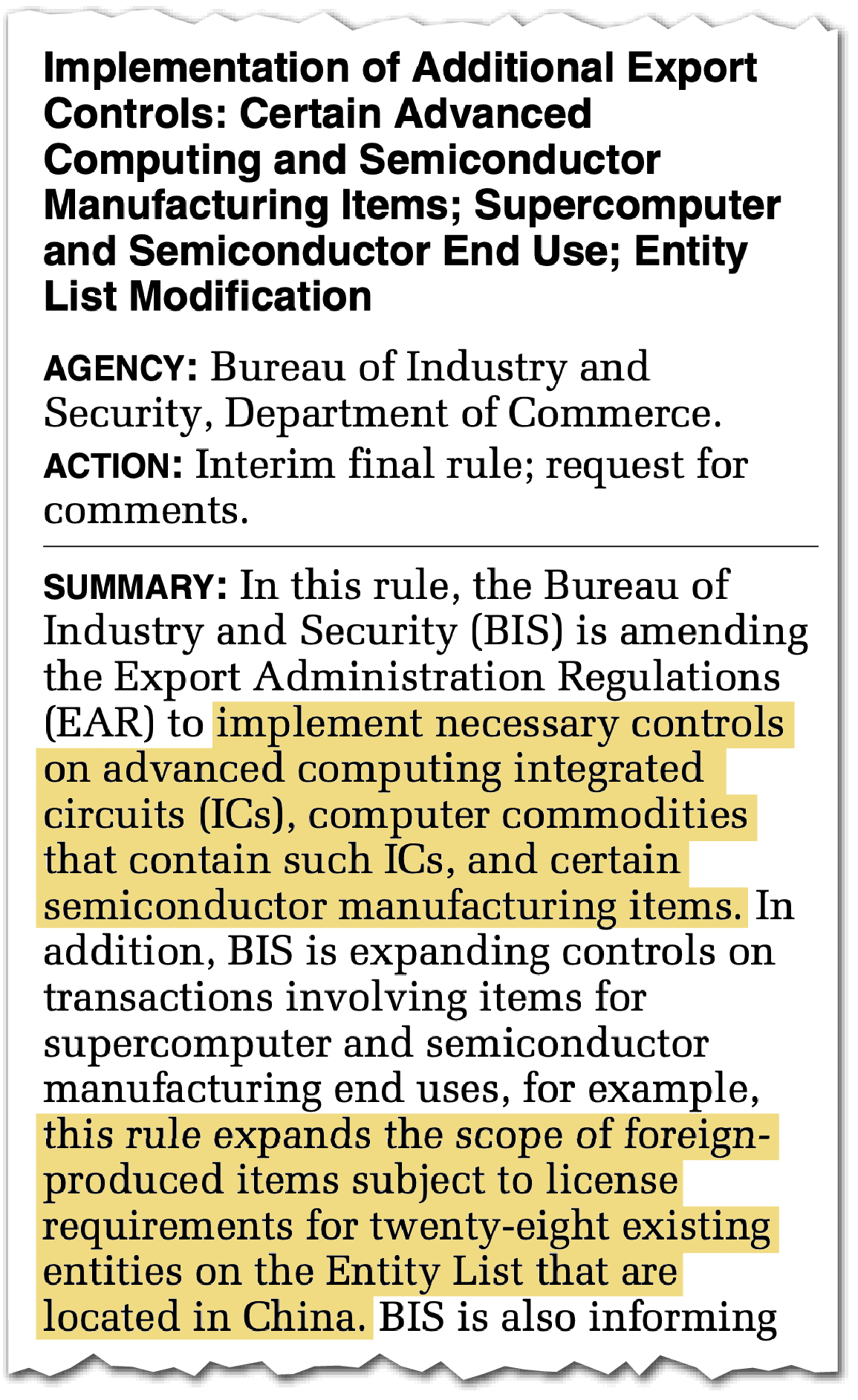

Do the strengthened export control rules that were released on October 17th this year plug the holes that have been uncovered in the last year?

The October 17th rules provide a couple of updates related to the sale of AI chips to China. Previously, the performance thresholds [that determined whether a chip was export restricted] were based on two specifications: absolute processor speed and interconnect speed, which is roughly a measure of how fast the chip can collaborate with other chips and access memory.

That was a problem because Nvidia was successfully marketing chips [to China] that were at the state of the art in processing power, but just below the interconnect speed threshold, and that did not appear to be imposing an especially large cost upon Chinese AI developers. The new policy is based on absolute processing power, which is now by itself enough of a criteria to lead to the prohibition on exporting the chip. The interconnect speed threshold has also been replaced with a measure called “processing power per square millimeter of silicon,” that is intended to make it difficult to put a lot of little chips together so that they can collaborate in a way that makes them as effective as one big chip.

In addition to having a “black zone” of absolute prohibition on certain chips of certain performance, there’s also a “gray zone” where the Department of Commerce gets the opportunity to review a chip export proposal and decide whether it is worthy of restriction. So the Commerce Department did a lot to plug the hole on the chips side of the equation.

Lastly, with regard to chip manufacturing equipment, there were important new restrictions imposed including a new standard for U.S. content that effectively blocks Dutch sales of immersion deep ultraviolet (DUV) lithography equipment. That is a big deal because it directly impacts SMIC’s ability to expand advanced manufacturing capacity. This new lithography rule won’t shut down the SMIC facility that is already in operation, but it will make it harder for SMIC to double or triple or 10x their production capacity at the seven nanometer node.

By expanding the scope of export controlled chips and equipment to encompass even more technology, it seems like the government has altered its philosophy from degrading China’s future capabilities to limiting what they can do now. Why the shift?

One potential reason for the change in desire is that the original controls were not a good fit for the original goal. I have described the policy as “choking off China’s access to the future of AI,” but perhaps there are people in the [Biden] administration who are saying: No, we really want China to miss the large language model revolution that really hit its stride after ChatGPT launched in October of 2022. That’s one interpretation.

Another is that the ChatGPT moment may also have changed what the administration wanted. They might have thought they had more time to slow China down, but now it turns out that the critical AI moment is much closer than they previously understood to be the case. And so it really matters to degrade [China’s capabilities] more urgently.

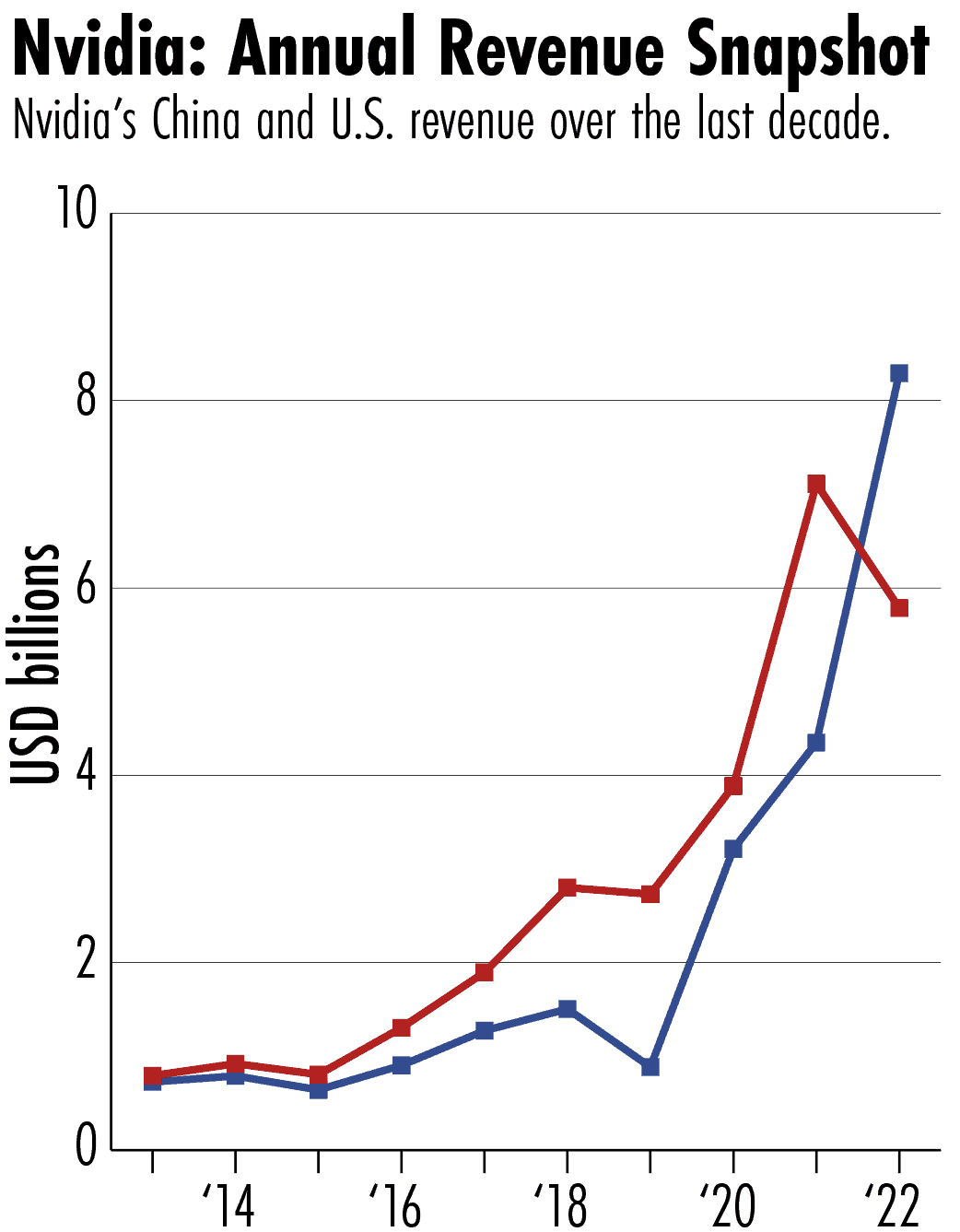

Nvidia has emerged over the last year as an indispensable supplier to the AI revolution. It responded very quickly to last year’s export controls by developing custom chips — the A800 and H800 — to comply with the controls while preserving their China sales. Then, after the updated rules were introduced, Nvidia again announced new chips — the H20 and L20 — for the Chinese market. Isn’t this starting to feel like a game of whack-a-mole?

I’m not aware of anybody who’s arguing that the H20 chips are as good as the H800. Those chips are at the absolute, best performance allowable under the gray zone restrictions of the updated export controls. But the gray zone means that the U.S. government can still block those sales. They’re going to be reviewed on a case by case basis, so maybe those chips will be allowed to be sold to China if they’re going to a Chinese university in quantities of the hundreds, but perhaps they will still be blocked if they are going to Baidu in the quantities of thousands or tens of thousands. Reportedly, Nvidia is delaying the launch of the H20, which may or may not be related to concerns about the U.S. government preventing sales.

We don’t really know yet how Commerce is going to wield this new restrictive authority they’ve given themselves. But even if Commerce does wield its authority permissively, these chips are still inferior to what Nvidia was previously selling to China. Just because Nvidia has not given up on all sales to China forever, does not necessarily mean that no cost has been imposed on China.

Chipmakers and chipmaking equipment suppliers like Nvidia and ASML draw a huge proportion of their sales from China. What are these companies supposed to do if the U.S. government cuts off their ability to export there?

For both chips and chip making equipment, it’s appropriate to understand what China has done in the last few years as stockpiling. You have to separate the sales that U.S. companies have lost from the sales that U.S. companies have pulled forward. They might have made those sales next year or the year after, but instead they’re making those sales this year. I heard from multiple companies that they refer to Chinese demand for semiconductor manufacturing equipment as “non-market demand,” which is to say they are buying equipment divorced from any kind of economic reality for how this is going to be a productive and profitable purchase. Rather, it is a Chinese strategic purchase made because it is backed by massive subsidization. They’re buying the equipment before they have a clear business case for how they’re going to profitably sell the chips that that equipment is going to make.

The same is true for Nvidia’s sales. Tencent recently stated that they have what they anticipate to be enough A800s and H800s to last them for the next several years. So one thing that the U.S. government could say is that those sales reduce the economic pain that companies can legitimately complain about, because even if it eliminated all restrictions, we would expect companies’ revenue from China to plummet in the future because all of those sales have already been moved forward.

You wrote in a recent report that Chinese companies are learning from foreign equipment and training domestic manufacturers, and moving at a rate that is faster than people expect. Could you say more about that?

…what can China make domestically by reverse engineering, and for any technological components that are too difficult to make, can they persuade, for example, a Korean company or a German company to do that?

There’s two different types of reverse engineering. One is learning about a viable engineering approach or scientific discovery. For example, if we were in the 1800s: I see a steam engine, I learn about the possibility of using coal to boil steam to move a piston, and using that insight, I go and design my own steam engine. Then there’s a different kind of reverse engineering, where you say: I don’t know much about steam and boilers and pistons, but I do know about machining parts that are millimeter for millimeter identical to the ones in this machine. Chinese semiconductor equipment manufacturers have demonstrated that they are perfectly happy to make millimeter for millimeter copies of American, Japanese and, where possible, Dutch semiconductor manufacturing equipment.

In addition to seeking to replicate all aspects of the machine and put a Chinese corporate logo on it, they’re also benefiting from many chipmaking firms’ international supply chains. A machine may be an American machine, but that doesn’t necessarily mean that 100 percent of its components were made in America. What Chinese equipment manufacturers have taken to doing is looking up all the foreign suppliers of U.S. equipment companies, and trying to cut a deal to procure those parts separate from the integrated machine. Sometimes there are contracts that state exclusivity [which prevent that]. For example, my understanding is that Zeiss — which makes a lot of the optical system for ASML’s lithography machines — has an exclusivity arrangement so it is not legally allowed to make lenses for Chinese lithography machines. But not all suppliers have those kinds of exclusivity arrangements, allowing Chinese companies to buy parts abroad that are not tied to export controls.

So the question is: what can China make domestically by reverse engineering, and for any technological components that are too difficult to make, can they persuade, for example, a Korean company or a German company to do that? That is the game that these Chinese companies are playing.

Do you have a ballpark estimate of what proportion of key chipmaking equipment China can produce domestically on its own?

It depends on a machine by machine basis. The four big categories of semiconductor manufacturing equipment are lithography, deposition, etching and inspection and metrology. At least one Chinese company, AMEC [Advanced Micro-Fabrication Equipment Inc.], is claiming that they will have machines that are domestically produced, potentially with foreign parts, for all of the deposition and etching that is required to manufacture memory chips. They won’t be at the current state of the art, but pretty close to the performance threshold specified in the October 7 export controls. That is years away, but not decades away.

By contrast, for something like extreme ultraviolet (EUV) lithography, where there has never been an EUV machine sold to China, and many of the critical components suppliers are locked up in exclusivity arrangements — that might be a decade away or more. And Dutch, U.S. and German industry aren’t going to be standing still for that decade either.

In a recent report, you made an interesting point about how the drop off in international customers for Chinese chipmakers removes a check against corruption for the country’s highly subsidized chip industry. Could you say more about that?

Chip companies of all kinds need customers as part of their technological progress and development. Customers put pressure on their suppliers to be better and in some cases, customers will directly assist you in becoming better. So if you are a government bureaucrat, offering subsidies to Chinese chip companies, it’s very difficult to know who you should be giving subsidies to. One source of reliable data of who you should be giving subsidies to is which companies are favored suppliers of large, sophisticated international customers.

Taiwan, Japan, South Korea did not initially have bureaucrats who were qualified to assess which semiconductor firms were well managed and technologically sophisticated, but foreign companies were qualified to do that. By allocating subsidies based on success in exporting, that minimized the burden on government officials to assess which companies were going to make the best use of their subsidy. The challenge for China is that that road is much more closed off to them because of geopolitics and the fact that China is often seen as an untrustworthy supplier, either by politicians or in many cases by companies themselves. And so China is going to have to mature its technology stack without the benefit of subsidies tied to exporting prowess.

Now, China does have one advantage that South Korea and Taiwan did not have, which is a colossal domestic market. The Chinese market is large enough without exports to reach reasonable economies of scale in a way that was never true for Taiwan or South Korea.

[But] China has the very real problem of corruption, with a hugely problematic record of wasted billions or tens of billions of dollars of government subsidies, but they don’t have that problem of insufficient economies of scale. Xi Jinping is hoping that simple crackdowns and the jailing of relevant government and corporate officials is going to be enough to reduce corruption, but that’s not a proven success story.

How do you see the longevity of the export controls — can they succeed under a potential second Trump administration?

I don’t expect that a Republican administration in 2025 would be looking to walk back this agreement. There aren’t many Republican leaders who are advocating for a loosened technology export control policy toward China. In terms of international politics, the Dutch don’t have the same prime minister anymore, but at the same time, if you look at the European Union, their political momentum appears to be headed towards more restrictions on technology exports to China.

Take Germany for example: German politics might be in for a sea change in their relations with China, driven not so much by the semiconductor industry but by the car industry, but that might change the political calculus within Germany’s government. If you look at the EU economic security strategy or the German China strategy, it appears that momentum is headed more in this direction, not less. I think the same is probably true in Japan.

Eliot Chen is a Toronto-based staff writer at The Wire. Previously, he was a researcher at the Center for Strategic and International Studies’ Human Rights Initiative and MacroPolo. @eliotcxchen