In May this year in Hiroshima, G-7 leaders agreed that “de-risking not decoupling” should be the basis for its member countries’ economic resilience and security when it comes to China. Yet one month later, German Chancellor Olaf Scholz strikingly declared that “de-risking…is mainly about decisions that need to be taken by companies.”

By eliding the critical role governments play in shaping the context for corporate decisions, Scholz’s words highlight a deeper truth. De-risking is about economic activity and economic relations. And in the G-7’s free-market economies, it is companies and individuals, not governments, that make most of the day-to-day decisions. Only in the most tightly defined circumstances should this change in the name of de-risking, because governments are ill-equipped to mandate, implement or finance wholesale adjustments in business operations. Success for Western countries will not come from aping the strongly interventionist, government-driven measures often seen in Chinese policy-making. Instead, governments need to figure out how to work with companies to achieve their policy goals, where to incentivize and where to constrain.

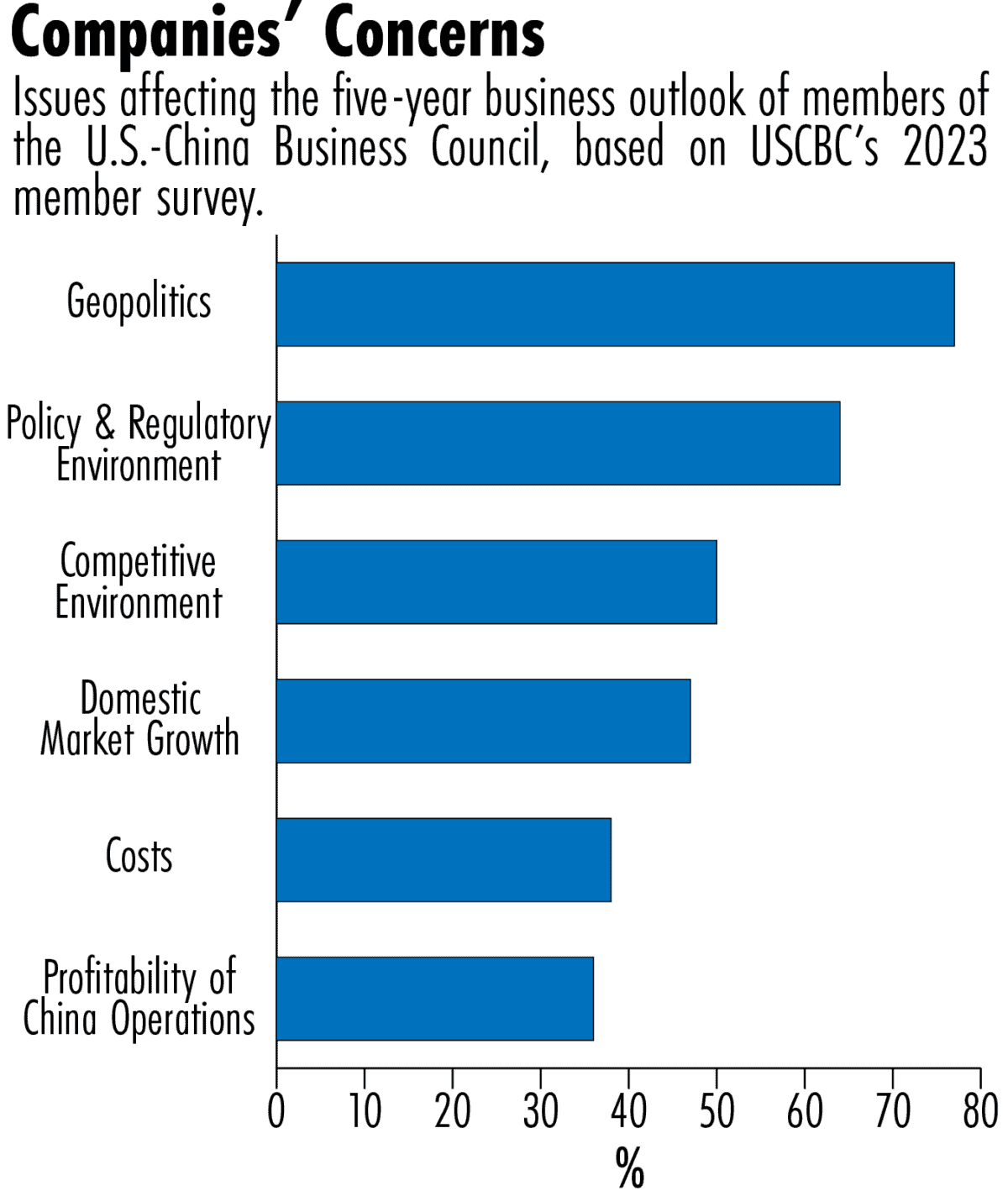

Companies are already busy pursuing their own version of de-risking. A recent U.S.-China Business Council survey found geopolitical risk topped the issues affecting the five-year business outlook for members. Shareholder pressure and the profit motive are providing strong incentives for companies to reassess the risk-return balance across their business. Leading companies excel at problem-solving and execution in pursuit of commercial objectives. They will identify novel approaches to managing risk at acceptable cost. Governments need to understand where these energies complement their own policy goals and harness them. They need also to understand where corporate efforts run at cross-purposes with their own, and intervene as needed.

For de-risking is different for companies and nations. Companies seek to reduce the risks to their revenues, costs and investments on an aggregate basis, across countries. In contrast, governments inherently want to protect their economies and societies within national boundaries against adverse influences. The EU maintains that de-risking “is not about China”. This is logically accurate — the approach addresses risks from whatever source. But, practically, most European governments will judge China to be the most important source of economic risk.

Companies are also concerned about potential economic risks from China, including Beijing’s emphasis on increased self-reliance. But they are affected too by deteriorating Western relations with China, whatever the cause. China-related policy decisions in the U.S., Europe or Japan and bilateral tensions pose risks that they need to manage.

Companies also have to be sensitive to China’s views and its stance that “de-risking is just decoupling in disguise”. They recognize that high-profile shifts away from China might signal a lack of commitment to their business there. For sure, many companies are diversifying production capacity away from China, consistent with Western government goals of reduced import dependence. Yet de-risking, from a multinational’s point of view, could also mean giving greater autonomy to its China business, so as to adapt better to local conditions. Reducing the direct interactions between its operations in the U.S. and China may be more profitable than reducing its actual presence in either market. Whatever the worst-case scenarios, it is unlikely a company will want to pull back from a profitable and competitive China business for risk reasons alone.

National security has always been the remit of governments not of companies. The pervasive nature of digital technologies, often with both commercial and defense applications, has now extended national security considerations deeper into the corporate sector. Companies are alive to the commercial risks of intellectual property theft, cyberattacks and reliance on critical infrastructure. But governments need to weigh the broader impacts on society, consider longer time horizons and assess tail risk scenarios. In Germany, the U.K., and elsewhere network operators originally chose Huawei equipment for their 5G rollouts, on commercial and technical grounds. To judge whether national security concerns should override these corporate conclusions, policymakers have faced the challenge of seeking the necessary expertise, often best obtained from the very companies affected, while retaining sufficient independence from them in order to determine the best way forward.

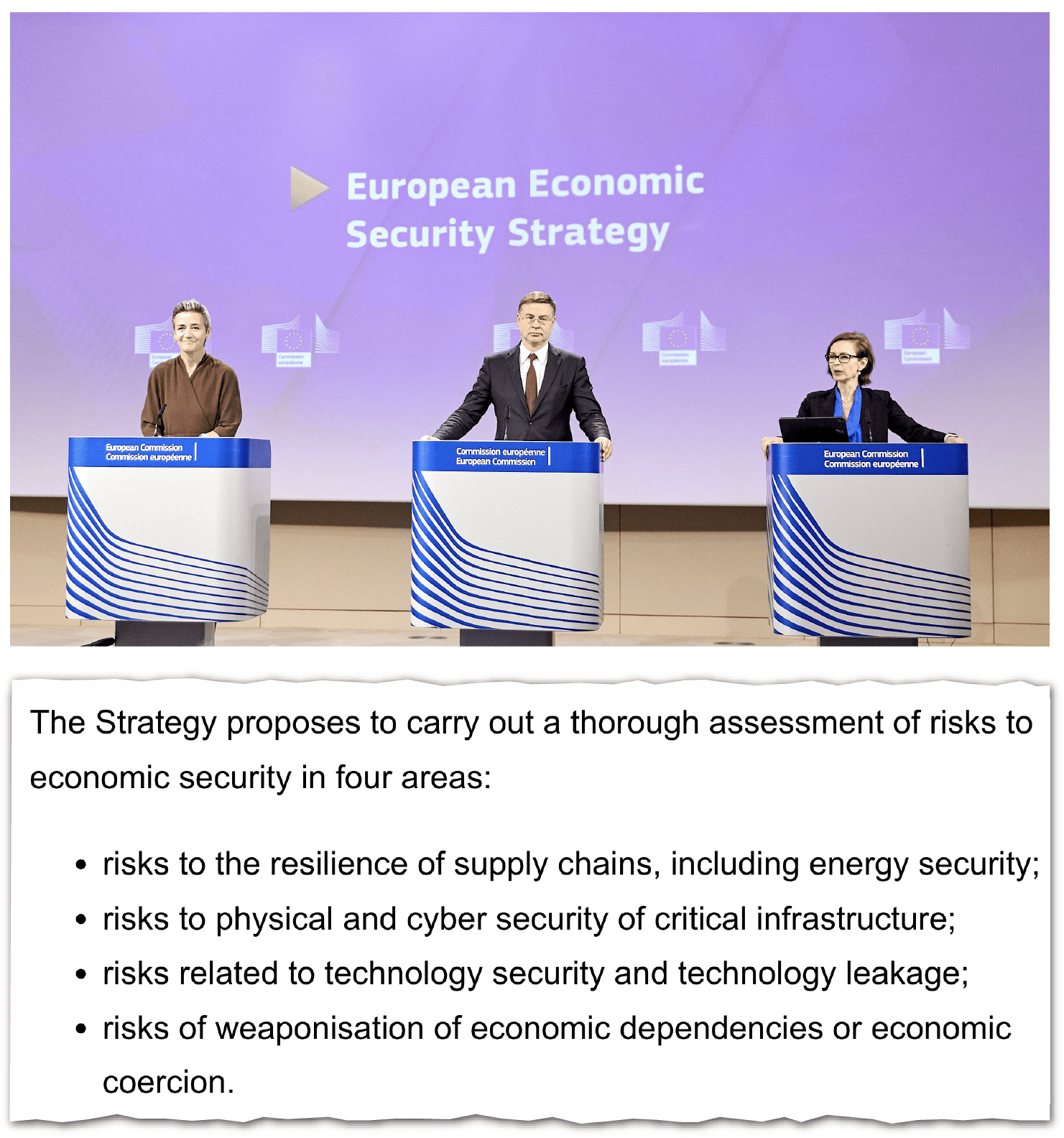

The broad corporate version of de-risking fits most closely with the EU’s current approach. Despite espousing ambitions for technology leadership, Brussels too has emphasized resilience and diversification. Any corporate leader would be familiar with three of the four areas of risk listed in the EU’s European Economic Security Strategy: supply chains, critical infrastructure, and technology and security leakage. The fourth – the risk of economic coercion – also has its business equivalent in excessive dependence on key markets, customers or suppliers.

As part of de-risking, the EU is also aiming to deepen its partnerships and trade ties with other nations and regions. This would expand the options open to companies to diversify away from China. However, it by no means ensures that companies will reshore manufacturing to Europe. Commercial decisions may thus yet leave critical supply dependencies unaddressed for individual countries. Governments still need to decide whether and where they want more resilience than companies judge profitable and, if so, who will bear the costs of, for example, mandating or financing additional capacity or holding safety stocks.

The U.S. has a different focus. Its “small yard, high fence” strategy emphasizes maintaining leadership in critical technologies. This has led both to export controls – which go against the short-term commercial interests of the affected companies – and declared ambitions to build greater domestic capacity and capability than results from market-based decisions alone. This requires government incentives and support to business. Policy success will rest on the government negotiating smart, cost-effective terms with companies that inevitably have a better understanding of industry economics, and are seeking the most favorable terms available.

…business leaders, managing their own risks, need to understand the different, sometimes conflicting de-risking priorities of governments and how they affect commercial risk and return.

De-risking also comes from deterrence. China has previously imposed restrictive trade measures on Lithuania, Australia and others. The EU’s Anti-Coercion instrument aims to deter such actions by specifying clearly how it will respond to such actions. By contrast, the U.S. priority is to deter Chinese moves on Taiwan by communicating in advance the economic consequences. In both cases, deterrence is more credible when it is clear that action can be taken at manageable cost. Companies have an important indirect role here. Both governments and companies can benefit if they work through contingency plans now on how to adjust most effectively if governments were to impose sanctions.

Chancellor Scholz is correct that de-risking is — ultimately — mainly about decisions taken by companies. But governments and often-global companies face different risks and have different priorities and incentives. The ambiguous meaning of “de-risking” is part of its appeal. But ambiguity can block effective action. Policymakers need to be clear on national priorities – and then engage fully with companies to harness corporate efforts, to forestall unintended consequences and to mitigate unaddressed risks. This requires deeper understanding of how businesses operate. And business leaders, managing their own risks, need to understand the different, sometimes conflicting de-risking priorities of governments and how they affect commercial risk and return.

Andrew Cainey is a senior associate fellow at the Royal United Services Institute, the world’s oldest defense and security think tank and a founding director of the U.K. National Committee on China. In his recently published book, Xiconomics: What China’s Dual Circulation Strategy Means for Global Business – written together with Christiane Prange – he analyzes the changing business environment for foreign business in China under Xi Jinping and the strategies that multinationals now need to pursue.