For some, the death of former premier Li Keqiang on October 27 signaled the passing of a class of Chinese leaders steeped in pragmatism rather than ideology. Among the better-known indicators of Li’s approach was his singular way of assessing the health of China’s economy.

Instead of relying on the country’s official GDP numbers, the former premier used a three-pronged proxy measurement for growth. Over time, this so-called ‘Li Keqiang index’ became widely watched by economists, investors and analysts keen for insights into how the world’s second-largest economy was really performing.

This week, The Wire asks what the index is telling us about China’s recent economic performance and assesses whether it’s still a relevant measure, 16 years after the ex-premier first proposed it.

A FRANK ADMISSION

The Li Keqiang Index’s origins lie in a State Department cable published by WikiLeaks in 2010 which told of a conversation between Li and former U.S. Ambassador to China, Clark T. Randt Jr., in 2007. At that time it was widely believed that Li, then the party secretary of Liaoning province, would eventually rise to one of the top jobs in China’s central government.

Li told Randt Jr. that China’s official GDP figures “are ‘man-made’ and therefore unreliable,” confirming that senior CCP leaders shared the widespread skepticism about the accuracy of Chinese economic data. He went on to share his own way of modeling growth in his province, based on figures less open to manipulation — measures of electricity consumption, rail cargo and bank lending.

“All other figures, especially GDP statistics, are ‘for reference only,’ [Li] said smiling,” according to the leaked cable.

“Li Keqiang was asked what he was looking at and he suggested that GDP is not the best number and that he looks at a selection of indicators, that were largely industrial in nature, to give a better sense of what the economic trajectory is,” says Frederic Neumann, chief Asia economist at HSBC. “Out of this grew the Li Keqiang Index to provide a better measure of underlying economic trends.”

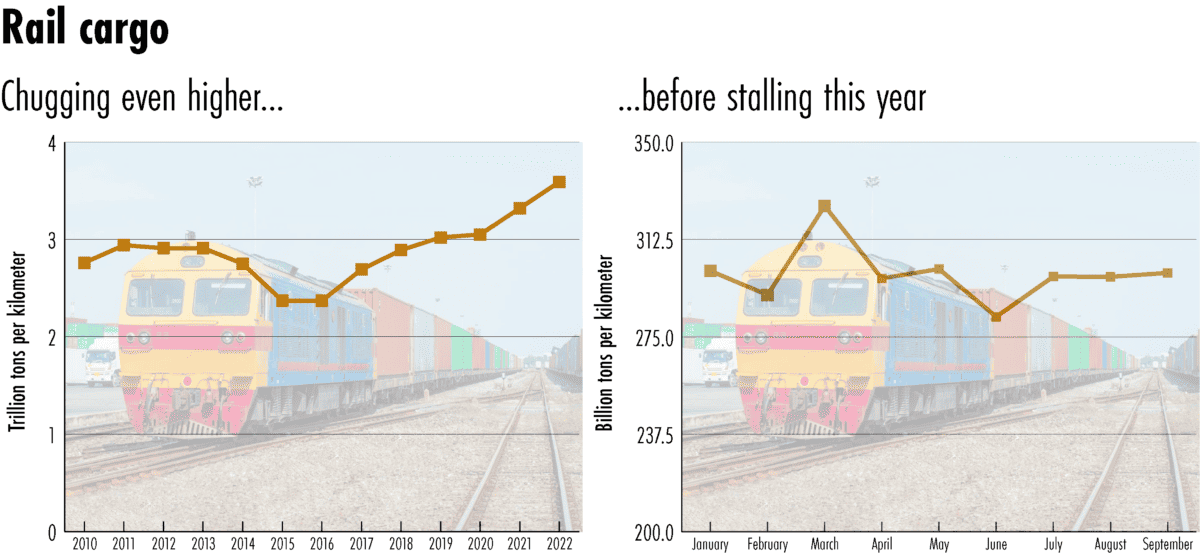

The chart below on the left measures annual rail cargo from 2010 to 2022, while the chart on the right measures cargo for the months of 2023 so far.

Li’s first indicator, the volume of cargo transported by rail, can be measured by ton–kilometers — that is, cargo weight multiplied by the distance it’s transported. Arguably, this measure is becoming less relevant: around 16 percent of goods manufactured in China were moved by trains in 2022, a steady decline in railways’ share of freight in favor of trucks.

Still, the Chinese government has recently released a series of strategies to increase railway’s share in freight transportation, according to the International Council on Clean Transportation. Figures over the last decade suggest China’s economic activity dipped around 2015-16; so far this year rail cargo volumes have remained largely flat.

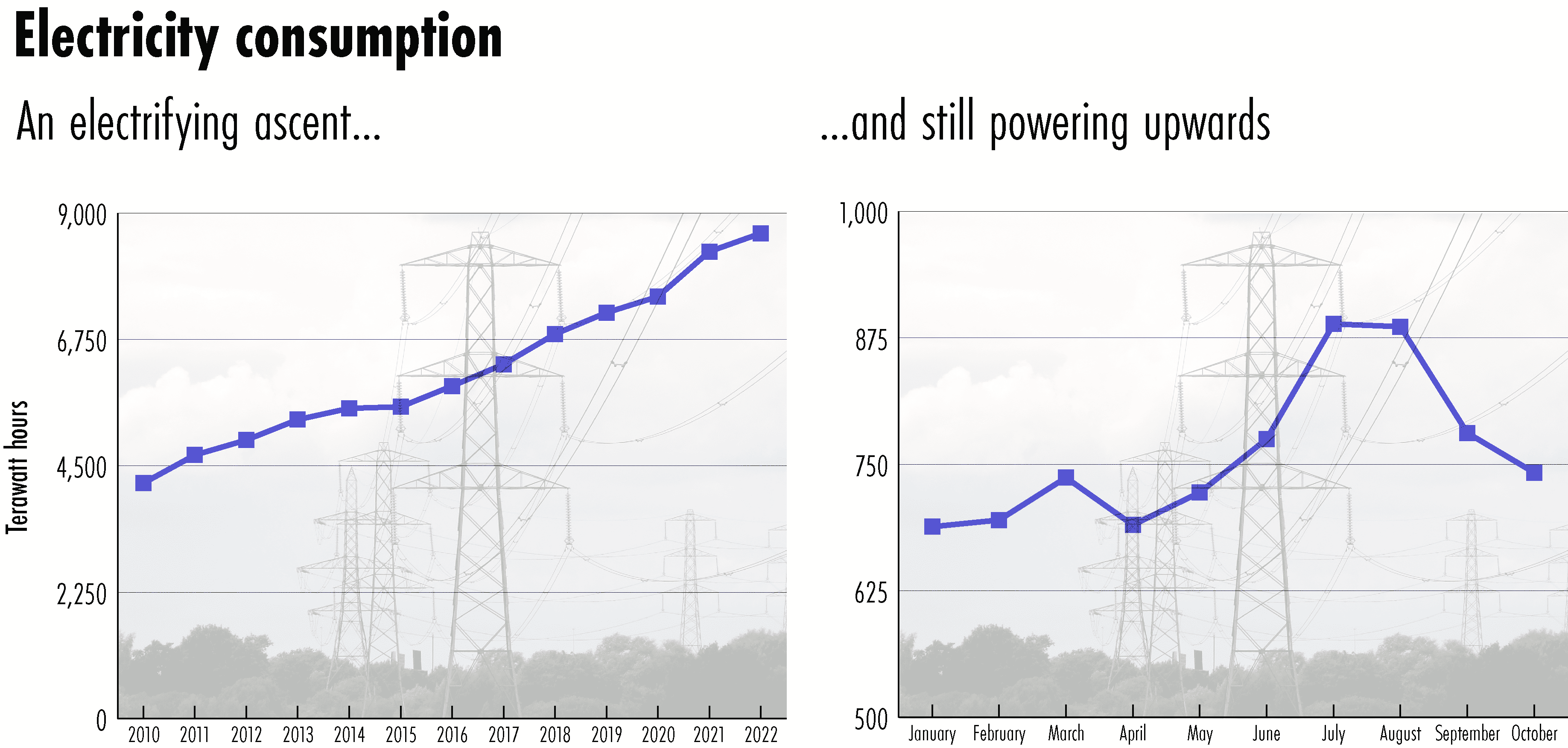

The chart below on the left measures annual electricity consumption from 2010 to 2022, while the chart on the right measures consumption for the months of 2023 so far.

Electricity consumption was seen by Li and others as a reliable indicator of growth, largely because the electricity grid’s connection to end users is constantly metered. Data shows that since 2010, electricity consumption has roughly doubled, thanks to rapidly increasing demand for industrial energy, which accounts for almost 70 percent of China’s national power consumption, according to Kevin Tu, fellow at the Center on Global Energy Policy and Columbia University. So far this year, the data shows that the upward trend looks set to continue.

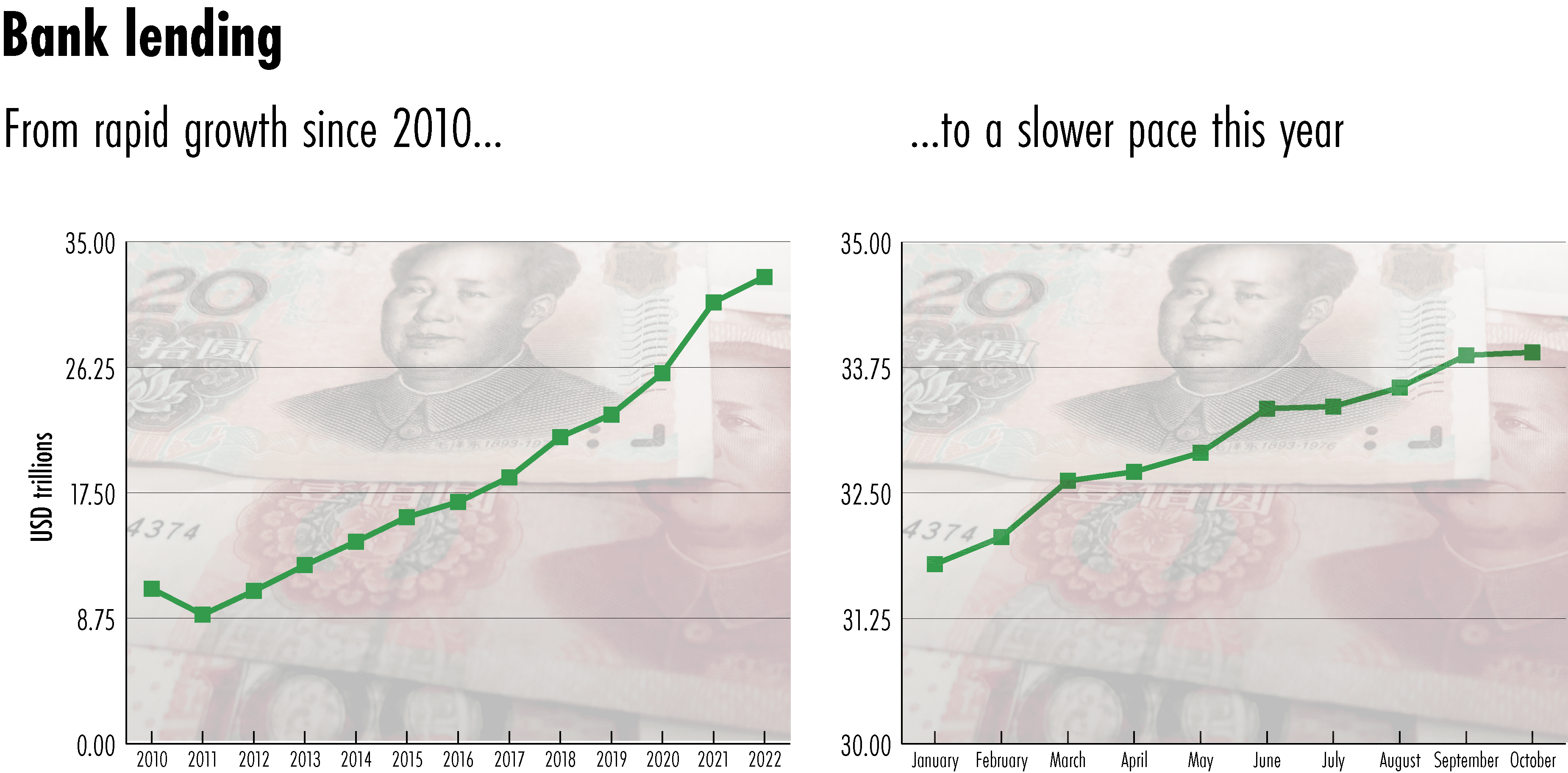

Bank lending data is a good indicator of where China’s economy is heading, given the central role banks play in funding companies: around 59 percent of corporate funding comes from loans rather than equities or bonds, according to research by the Reserve Bank of Australia.

Lending has surged since the idea of the Li index first emerged, with the amount of outstanding loans up threefold since 2010. Still, economists have repeatedly warned of risks associated with ballooning debt, particularly in China’s real estate market. China’s overall debt to GDP ratio now stands at 297 percent, according to the Congressional Research Service.

The Chinese economy is still a manufacturing economy, and this is because the Chinese government has not made any effort to rebalance its economy towards consumption.

Juan Orts, economist at Fathom Consulting

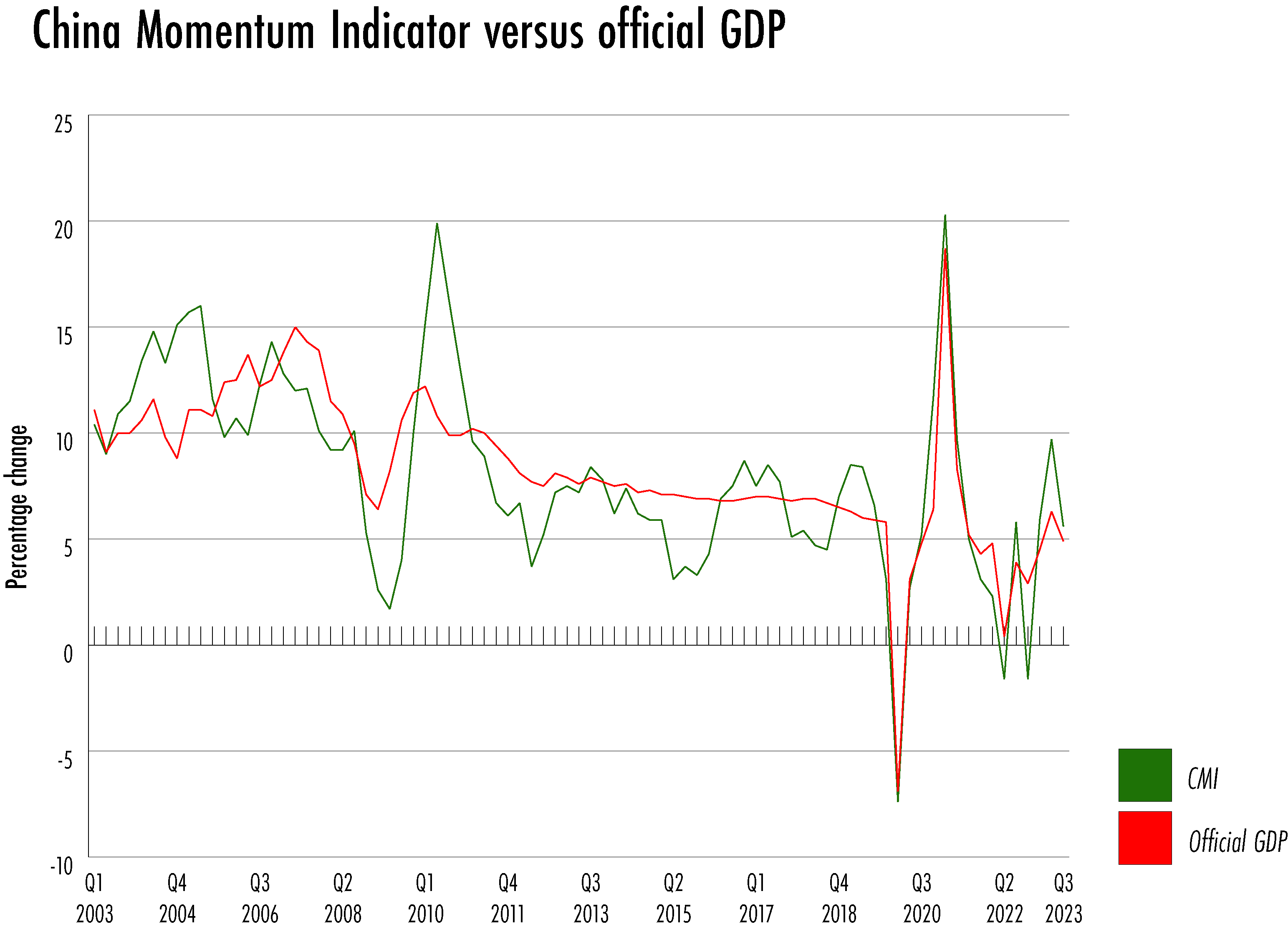

Other economists have tried to mimic and adapt Li’s alternative growth model over the years. London-based Fathom Consulting’s China Momentum Indicator is one such: the firm has added parameters to reflect private consumption, including retail sales, consumer goods imports and urban disposable incomes.

“This indicator shows you how much China is growing each month, and it’s also telling you how much of that is consumption, how much of it is investment and how much of it is net exports,” says Juan Orts, economist at Fathom Consulting. “The official statistics, they don’t give you that at all.”

Some analysts, such as HSBC’s Neumann argue that the growing contribution to growth from China’s services sector has made Li’s industry-heavy index a less reliable gauge.

“That [has] rendered the original version of the Li Keqiang index somewhat obsolete today, because of the evolution of the Chinese economy towards other sectors,” says Neumann.

But Fathom’s Orts, although agreeing that the original index is no longer reliable, adds that China’s economic reliance on manufacturing has not changed.

“The Chinese economy is still a manufacturing economy, and this is because the Chinese government has not made any effort to rebalance its economy towards consumption,” he says. “Xi Jinping does not believe in the U.S. model of growth in which consumers have most of the power.”

Fathom’s CMI fluctuated more compared to official GDP data in the years between Xi Jinping’s ascent to power and the onset of the COVID-19 pandemic. But the two indicators have matched up more closely since — a sign, Orts says, of the Chinese leadership’s shifting priorities.

“We think that the period in which GDP growth was the most important thing is over for China,” says Orts. “Now the focus has shifted to other factors, for example, national security. This is why we think that Chinese statistics have become more reliable now, because there is no need to lie.”

Aaron Mc Nicholas is a staff writer at The Wire based in Washington DC. He was previously based in Hong Kong, where he worked at Bloomberg and at Storyful, a news agency dedicated to verifying newsworthy social media content. He earned a Master of Arts in Asian Studies at Georgetown University and a Bachelor of Arts in Journalism from Dublin City University in Ireland.