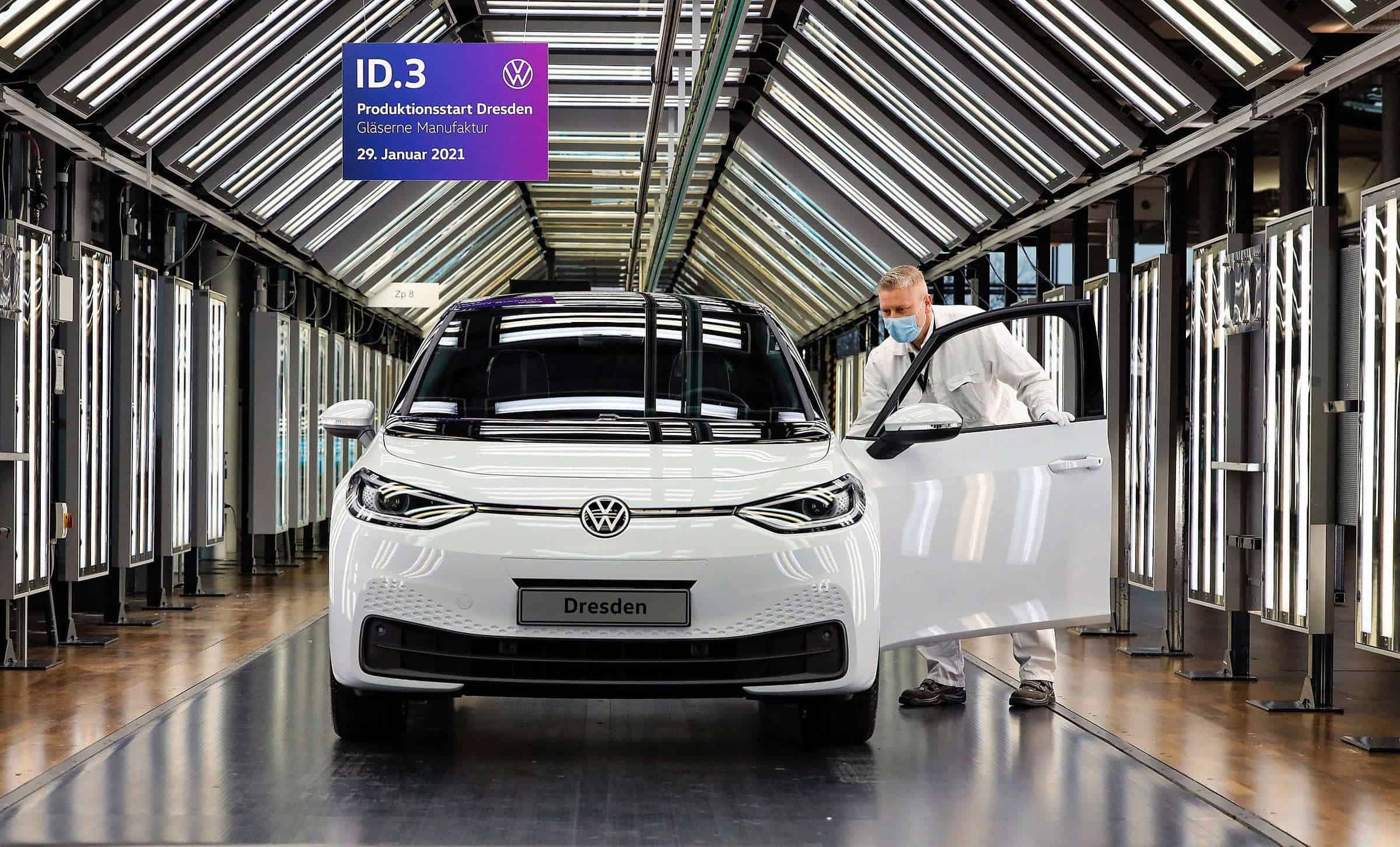

Volkswagen’s “Transparent Factory,” in Dresden, Germany, was designed as a “beacon” to demonstrate all that the company has to offer.

Made almost entirely of glass, the small, but sleek factory plays with the double meaning of “transparency,” and invites VW customers to visit and see the production process for themselves.

But on a recent grey November day, the electric hum of the automated assembly line of VW’s fully electric ID.3 model instead masked the factory’s many troubles.

Just a few weeks earlier, 150 workers had gathered outside the factory to protest VW’s reported plan to carry out mass layoffs, impose sweeping 10 percent pay cuts, and shut at least three VW factories in Germany. VW management has pointed to the untenable manufacturing costs and poor productivity in its German factories, and says the company aims to make some $5 billion in cutbacks in its home market as early as next year.

With the showcase Dresden site rumored to be a shutdown target, the local work council called the restructuring announcement “embarrassing and brazen,” and local politicians warned that the factory’s closing would leave a “gaping wound in the heart of the city.”

Indeed, if the shutdowns move ahead, it will represent the first time in the storied-German automaker’s almost 90-year history that it closed factories at home. Management and the union resume negotiations this week as roughly 100,000 workers carry out a new wave of strikes at nine factory sites across Germany. The Volkswagen Group, which includes brands like Porsche and Audi, is Germany’s largest employer with nearly 300,000 workers on its payroll at home.

“Volkswagen clearly must address its high-cost situation,” says Stephen Reitman, a London-based analyst at Bernstein Research, “but human nature will push the unions and politicians to resist too many layoffs and plant closures”

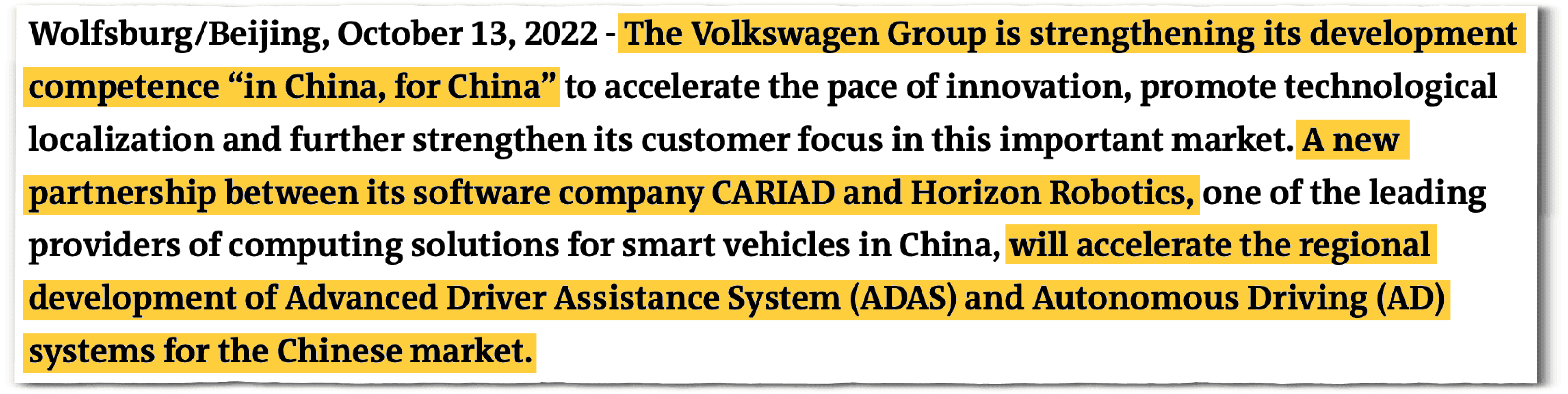

Adding to this predicament is the fact that VW is acting altogether differently in China, which Volkswagen Group chief executive Oliver Blume has called the automaker’s “ second home market.”

Although VW says it has no choice but to tighten its belt in Germany, the company announced a $2.7 billion investment earlier this year to expand its EV production and innovation hub in the Chinese city of Hefei in Anhui province. The site will boast a technology center, ending a decades long practice at VW of developing cars in Europe and bringing them to China.

This news came on top of last year’s announcement of VW’s joint development of two new models with domestic EV maker Xpeng and a $700 million investment for a 5 percent stake in the Chinese company.

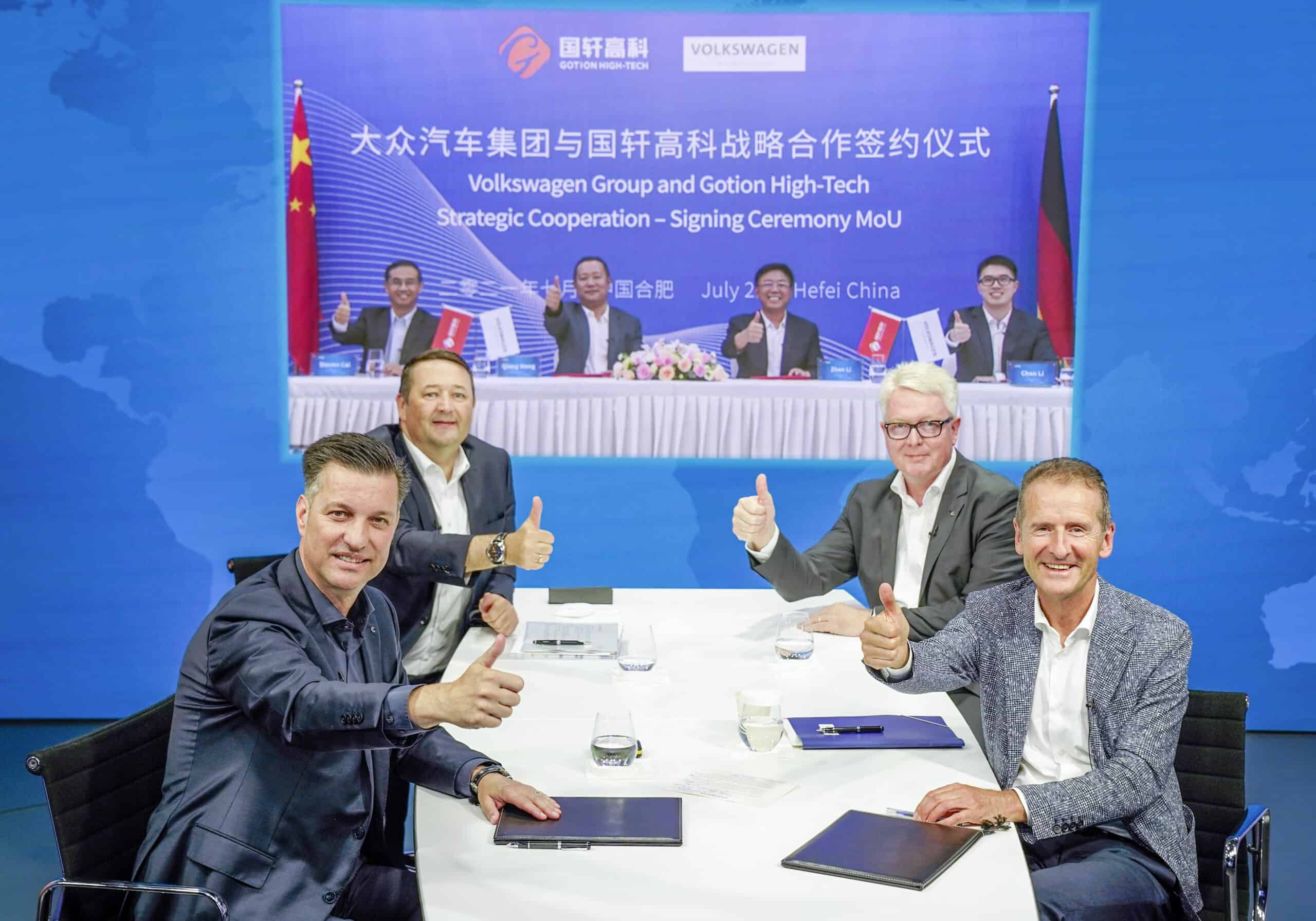

A year earlier, VW bought a $2 billion, 60 percent majority stake in Beijing-based Horizon Robotics to develop an autonomous driving system, and spent another $2 billion to raise its equity shares in its local joint venture with Chinese manufacturer JAC Motors in Anhui, as well as to buy a quarter stake in Chinese battery producer Gotion High-Tech.

“The Chinese market is the powerhouse of the automotive industry globally and setting the pace for many future technologies,” a VW spokesperson told The Wire China. “Digitalization and connectivity of the car, AI-enabled smart cockpit functions, and autonomous driving are developing at a speed that we cannot imagine in Europe.”

The corporate interest is to outsource to China because it has the most sophisticated, innovative, and efficient supply chain compared to anywhere else. But policymakers in Europe have other aims.

Yanmei Xie, a geopolitics analyst at Gavekal Research

China is the world’s largest automobile market and exporter, producing some 30 million vehicles last year. It is also the center of the world’s EV industry, making 8.6 million EVs last year — close to seven times more than Germany, the world’s second largest EV producer. Consequently, some analysts argue that automakers like VW can’t afford to lose touch with trends and innovations in the Chinese market. From this perspective, China is a “fitness center” of sorts, where companies need to be active if they want to produce competitive and innovative global products.

But VW’s strategic decision to “go on the offensive” in China, as Blume has said, while restructuring in Germany, is risky business.

For starters, many foreign companies are currently questioning whether China’s slowing economic growth is worth the risk of operating in an increasingly hostile business environment. A long line of foreign automakers are also already retreating as China’s rapid transition to EVs, with the rise of domestic players leaving them in the competitive dust: Over the last two years, the share of foreign brands in the Chinese car market has fallen from 53 percent to 33 percent this July.

GM’s vehicle sales in China, for instance, have fallen by a staggering 56 percent since 2020, and it recently announced a $5 billion write-down on its China operations. Its Detroit compatriot, Ford, has seen its sales plummet by 70 percent in the Chinese market. That result prompted its CEO, Jim Farley, to dial down the company’s ambitions; he currently sees China as a “listening post” to keep up automotive trends rather than a market for expansion.

Last year, Japan’s Mitsubishi Motors abandoned local manufacturing in China. A year earlier, French carmaker Stellantis shuttered the last factory of Jeep, its subsidiary, in China — one of the very first Sino-foreign joint automobile ventures.

And VW itself is hurting. Last year, after some four decades as market leader, VW lost its number one status in China. Its market share has declined to 10 percent as domestic upstart BYD surpassed it at 12 percent. (Sales numbers so far tallied up this year see BYD extending its lead.) This year VW also reported its first quarterly loss in equity income in China in over a decade and a half.

But VW isn’t cutting and running. Instead, it seems determined to do whatever it takes to hold onto its double-digit share of the Chinese market.

“Volkswagen’s doubling-down on investment and commitment to the Chinese ecosystem is quite unique compared to any other foreign automaker,” notes Lei Xing, co-host of the China EVs and More podcast and former chief editor at China Auto Review.

Rhodium Group research found that VW invested over $13 billion in China from 2018 to October this year. That is four times more than Japan’s Toyota and eleven times more than America’s GM.

The company’s so-called ‘in China, for China’ strategy focuses on deepening local partnerships, improving cost efficiencies, and staying at the bleeding-edge of new innovations. Although VW’s Blume makes no promises of a “utopian” future in China, there are tentative, early signs that the strategy may work to keep VW in the race. While overall sales in China are down, VW’s EV sales rose 27 percent in the first three quarters of this year compared to last.

VW argues that the basis for the group’s success lies in the high quality, safety and reliability of its products. “Particularly in a dynamic market like the Chinese one, where new products are thrown into the market at a high rate,” a spokesperson says, “these values are crucial to gaining the long-term trust of customers.”

But the company’s ambitions in China may clash with — and even undermine — the trust VW has built with the broader German and EU economies.

“The corporate interest is to outsource to China because it has the most sophisticated, innovative, and efficient supply chain compared to anywhere else,” says Yanmei Xie, a geopolitics analyst at Gavekal Research. “But policymakers in Europe have other aims. They not only want to meet decarbonization goals, but also produce growth, innovation, jobs, revenues, and value-added.”

With China’s soaring capacity — it is expected to export 6 million vehicles this year — disrupting a global industry that has traditionally seen production rooted to regional markets, the EU decided trade action was the only option left.

This October, the EU put into force a range of tariffs on Chinese-made EVs. Wayne Griffiths, CEO of the VW Cupra, warned that the entire brand could be “wiped out” by EU tariffs on the Cupra Tavascan, a mid-sized electric SUV built at VW’s joint venture in Anhui.

VW opposed the tariffs, which were put into place for five years, and reportedly did not cooperate with the European Commission’s investigation leading up to them. As Xie from Gavekal says, the tariffs “dropped a big wrench in VW’s plans.”

Indeed, most experts agree that the company and other European carmakers may still harbor ambitions to leverage China’s capable and efficient supply chains for production and export — “in China, for the world.”

“If you’re a cost-conscious company that wants to scale, and you’re seeing Chinese competition on the rise, then you probably want to leverage Chinese suppliers and Chinese tech for outside markets,” says Gregor Sebastian, senior analyst at Rhodium Group.

Reading the signals of a geopolitically divided global economy is far from a perfect science, but now any plan to use China as a platform for manufacturing, technology and know-how to enhance global competitiveness looks limited. Instead, VW is being forced to wage battle on separate fronts.

As BYD and Chinese EV makers continue to stretch their legs overseas, VW — Europe’s largest corporation — must compete for ground not only in its ‘second home market,’ but in its home market too.

“There is a bigger risk than core European corporate champions going under in China,” says Jens Eskelund, President of the EU Chamber of Commerce in China, “and that is going under in the rest of the world.”

Be Chinese

When the Transparent Factory opened, there was little doubt it was distinctively German.

Designed by Dresden-native architect Gunter Henn, the factory’s foundation was laid by then-Chancellor Gerhard Schröder, longtime VW chairman Ferdinand Piëch, and Kurt Biedenkopf, who at the time, was prime minister of the German state of Saxony.

VW maintains deep familial and government roots today. The Porsche-Piëch family is its largest shareholder and holds a majority voting stake, while Lower Saxony maintains an 11 percent share and one-fifth voting stake on top of its vital role in VW’s supervisory board.

“It will be possible to both see and feel the finest hand craftsmanship and state-of-the-art technology here,” Piëch boasted when the factory began production of the VW Phaeton, a luxury sedan, in late 2001.

The Phaeton was conceived by Piëch to compete with Mercedes-Benz and BMW. Customers could watch it being “assembled almost completely by hand in light-flooded halls” while roaming floors that were “covered with light mountain maple wood from Canada and dark German moor oak.”

With the Phaeton, German engineers did what they did best: powerful petrol and diesel engines. Most of its components were provided by a diverse German network that included Bosch and ZF Friedrichshafen, and although sales of the near $100,000 prestige car never took off, peaking at over 11,000 units in 2011, over 80,000 units had been made altogether when production halted in 2016.

By 2017, VW’s EV transition began to take shape, and the Dresden factory’s production shifted to a new electrical architecture: Modularer Elektrobaukasten, or MEB for short, a hardware configuration bringing all the electronic components, wiring, and circuits into a single platform to be shared across VW’s EV models.

German factories still supply components for VW’s EV models, but unlike combustion engines, the most critical components depend heavily on technology from Asia. VW’s EV models, for instance, have traditionally relied on battery packs produced by South Korea’s LG Chem, but are increasingly using those from China’s battery giant, CATL and Gotion High-Tech. (Although South Korean and Japanese battery makers remain competitive, China controls between 70 and 85 percent of the key components in battery making.)

Compounding this dependency is the fact that the large robotic arms on the assembly line in Dresden are made by the Bavaria-based robotics company Kuka, whose $5 billion takeover in 2016 by Midea, a Chinese electrical appliance manufacturer, sent shockwaves through the German establishment.

VW was a first mover to China in the early 1980s and helped build up the modern automobile industry there. As a result, by the late 1990s, the German automaker enjoyed 50 percent of the Chinese market; just two VW models, the Santana and Jetta, accounted for four-fifths of the entire passenger car market.

That changed at the turn of the century, when Toyota, GM and other foreign automakers raced into a Chinese market that was growing at 25 percent a year.

Left: The VW Santana, the first model produced by SAIC Volkswagen, April 11, 1983. Right: The first Jetta produced by FAW-VW, 1991. Credit: Volkswagen Group China

VW was caught sheepishly off-guard and lost some 30 percent of its market share in a short time. But after introducing new models and building out new low-cost production in China, VW managed to hold onto nearly 20 percent of the Chinese market — and just in the nick of time. In 2009, China became the world’s largest car market, and the profits came flooding in.

For years, it has been the prominent view in Germany that profits earned in China have ultimately kept the lights on in Stuttgart and Wolfsburg.

Gregor Sebastian, senior analyst at Rhodium Group

“There was a window of ten years where Volkswagen was dominating the Chinese market,” says Arndt Ellinghorst, a longtime analyst of Volkswagen and the global automobile industry at QuantCo, a data analytics company. “With little competition from Chinese brands, volumes and profits kicked in. Volkswagen was in harvest mode.”

For example, Evercore ISI, an equity research firm where Ellinghorst once worked, estimates that in 2016, VW’s China profits represented 49 percent of its global total — double that of GM and 20 percent higher than its German counterparts Mercedes and BMW. Likewise, in 2021, a Bernstein Research note found that China made up close to half of VW’s total earnings and cash flows.

VW typically sold more vehicles in the EU on an annual basis, but experts underline that the company enjoyed significantly higher profit margins in China, particularly because it earned sky-high premiums on imports of luxury brands like Porsche and Audi and generated billions more through licensing, royalties and auto parts sales in China.

On the other side of the ledger, overall costs in China pushed margins up further, explains Beatrix Keim, Director of the Center Automotive Research (CAR), a private-sector research institute in Germany.

“Salaries, energy, and supplier and distribution costs in China are still below those in Germany,” she says.

Costs were also higher for VW in Europe and the United States for a very particular reason.

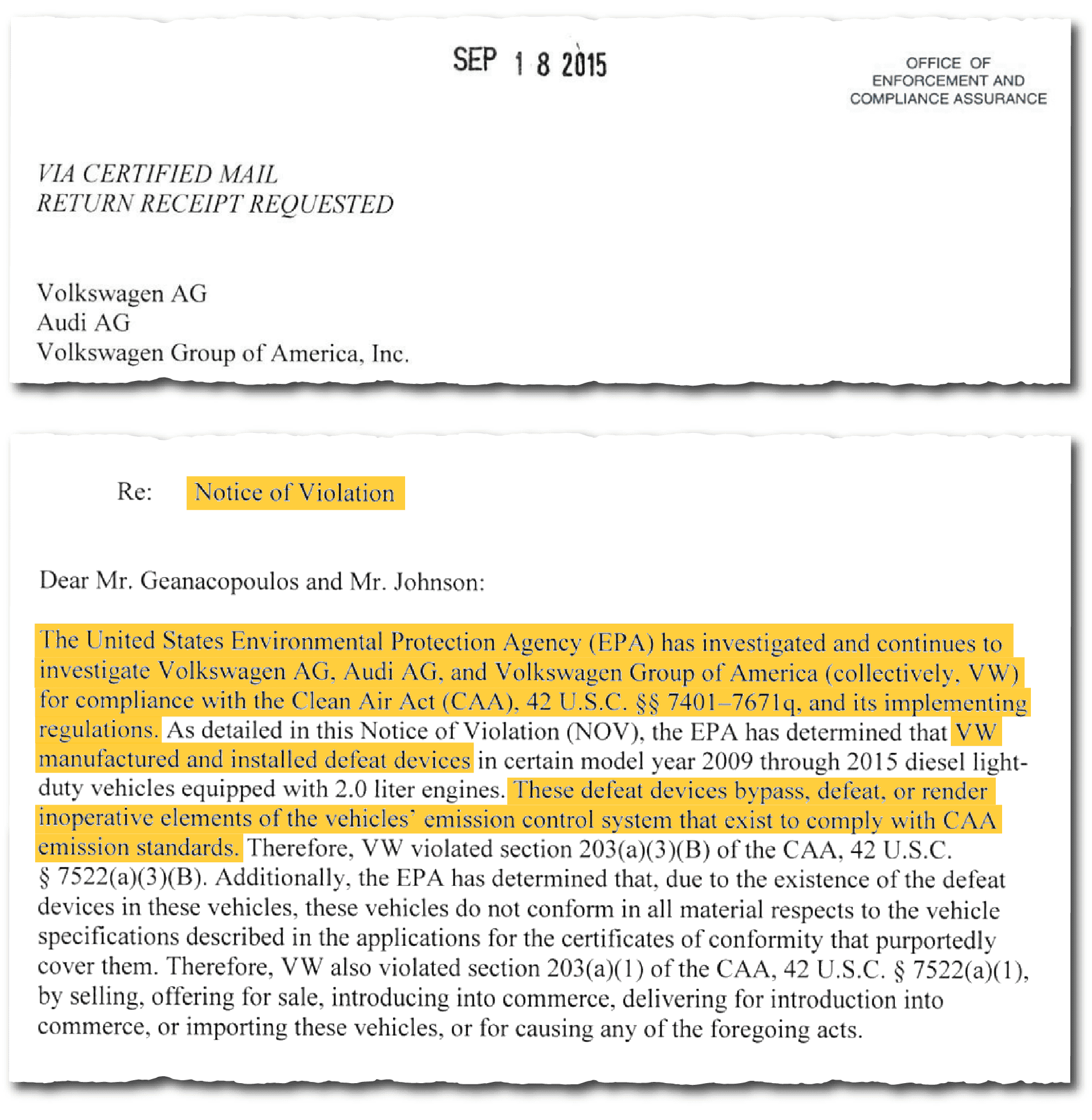

In 2015, an investigation of the United States Environmental Protection Agency found that software installed in a long line of VW models was intentionally programmed to activate emissions controls in laboratory testing only, and not in regular, everyday use, when they at times emitted 40 times the permitted nitrogen oxide levels.

The resulting fines, settlements and buyback costs of the ‘Dieselgate’ scandal cost VW $38 billion — and counting.

“It was a drag on everything,” says Ellinghorst, “but Volkswagen quickly bounced back.”

In large part thanks to China. While executives at VW’s sprawling headquarters in Wolfsburg grappled with the publicity nightmare at home, they rejoiced in double-digit sales gains in China. In 2017, VW even claimed the title as the largest automaker in the world.

“For years, it has been the prominent view in Germany that profits earned in China have ultimately kept the lights on in Stuttgart and Wolfsburg,” says Sebastian, at Rhodium.

Indeed, Thomas Puls, a senior economist at the German Economic Institute (IW), argues that VW’s success in the Chinese market made it possible for the company to invest in production capacity that held “no economic justification.” He sees the Transparent Factory in Dresden, for instance, as “a political project that could be dragged along for a long time thanks to the profits flowing from China.”

Beyond subsidizing arguably frivolous projects, QuantCo’s Ellinghorst adds that China revenues distracted the company’s brass from addressing serious challenges — namely, VW’s unique governing structure. Because the union and the German state of Lower Saxony together hold a voting majority on the company’s supervisory board, Ellinghorst says VW was — and remains today — limited in its ability to make far-reaching strategic decisions at critical times.

Reitman, of Bernstein Research, agrees. “I’ve been covering the company since 1985, and it seems like everything’s changed, but nothing’s changed,” he says, recalling that in the early 1990s the German automaker announced large cost cuts in response to rising competition from Japanese manufacturers.

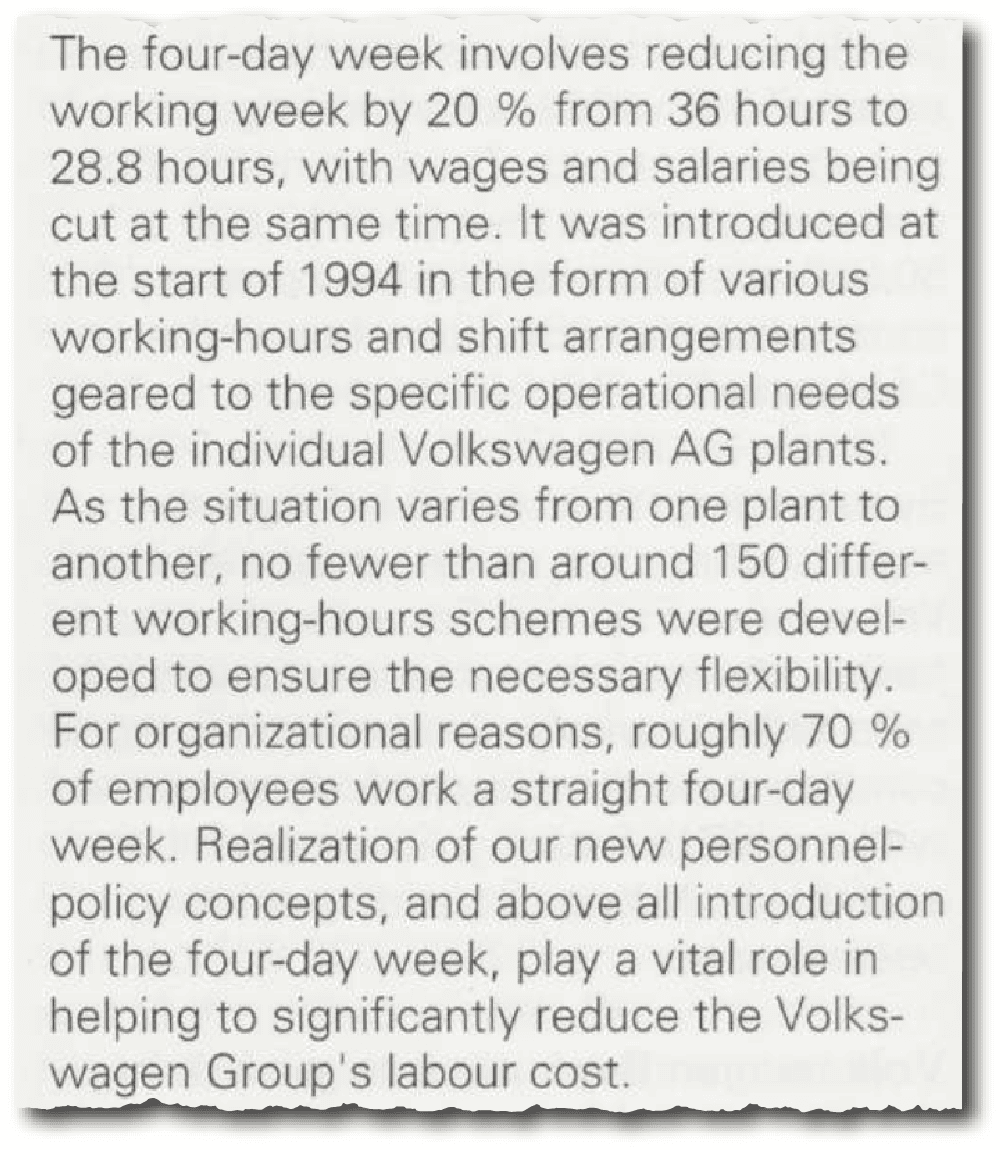

Back then, VW did not follow through on its plan to lay off a third of its German workforce. Instead, in 1994, it made a no-layoff pledge until 2029, coming to terms with its influential union to lower weekly working hours and implement other cost savings and productivity measures, such as building a larger number of models from a common chassis.

The push and pull between VW and its union continued. “Over 30 years later, Volkswagen is still bloated and overstaffed,” says Reitman.

What’s changed, however, is that the company, since around 2010, has also become hyper-dependent on a single market.

“If you’re a company like Volkswagen that, from a governance perspective, is dominated by politicians and unions, then growing out of your problems is always the fallback strategy,” Ellinghorst says. “China was like a sweet drug fueling that addiction, but in the long run, it was a massive risk, because Volkswagen’s global footprint was off-balance.”

The rapid rise of BYD and other Chinese EV competition now threaten to knock VW to the ground. In a recent earnings call, the company reported that the fall in China sales in the first three quarters of the year contributed to an overall 31 percent decline in global profits.

Getting Digital

How might VW reverse course? Analysts point to its failure to keep up with EV software as a key challenge to overcome.

Former CEO Herbert Diess knew software was key: In 2020, he launched Cariad, a new software subsidiary, and invested over $12 billion in it as part of the company’s larger efforts to transform itself into an EV company. “Software offers a huge opportunity for economies of scale,” Diess said.

But according to Reitman, Cariad turned into a multi-billion dollar “bureaucratic monster” with clunky software and delayed updates.

In the spring of 2021, the launch of the ID.4 fell flat in China — selling a little over 1,200 units in two months compared to over 6,600 Tesla Model Ys during its initial debut. VW’s joint venture in China reportedly even proposed to its employees that they buy the struggling models to boost sales numbers.

“Volkswagen was behind in terms of software and offering the functionalities that Chinese customers expected,” says Reitman.

Cariad’s failings — which contributed to VW’s poor EV showing in China — and clashes with labor representatives over his suggestions of large job cuts contributed to Diess being shown the door as CEO in July 2022.

Chinese customers care less about the powertrain, but they do care about how the car connects to everything on their phone. A German engineer builds the car around the engine; a Chinese engineer builds around the mobile device.

Arndt Ellinghorst, a longtime analyst of Volkswagen and the global automobile industry at QuantCo

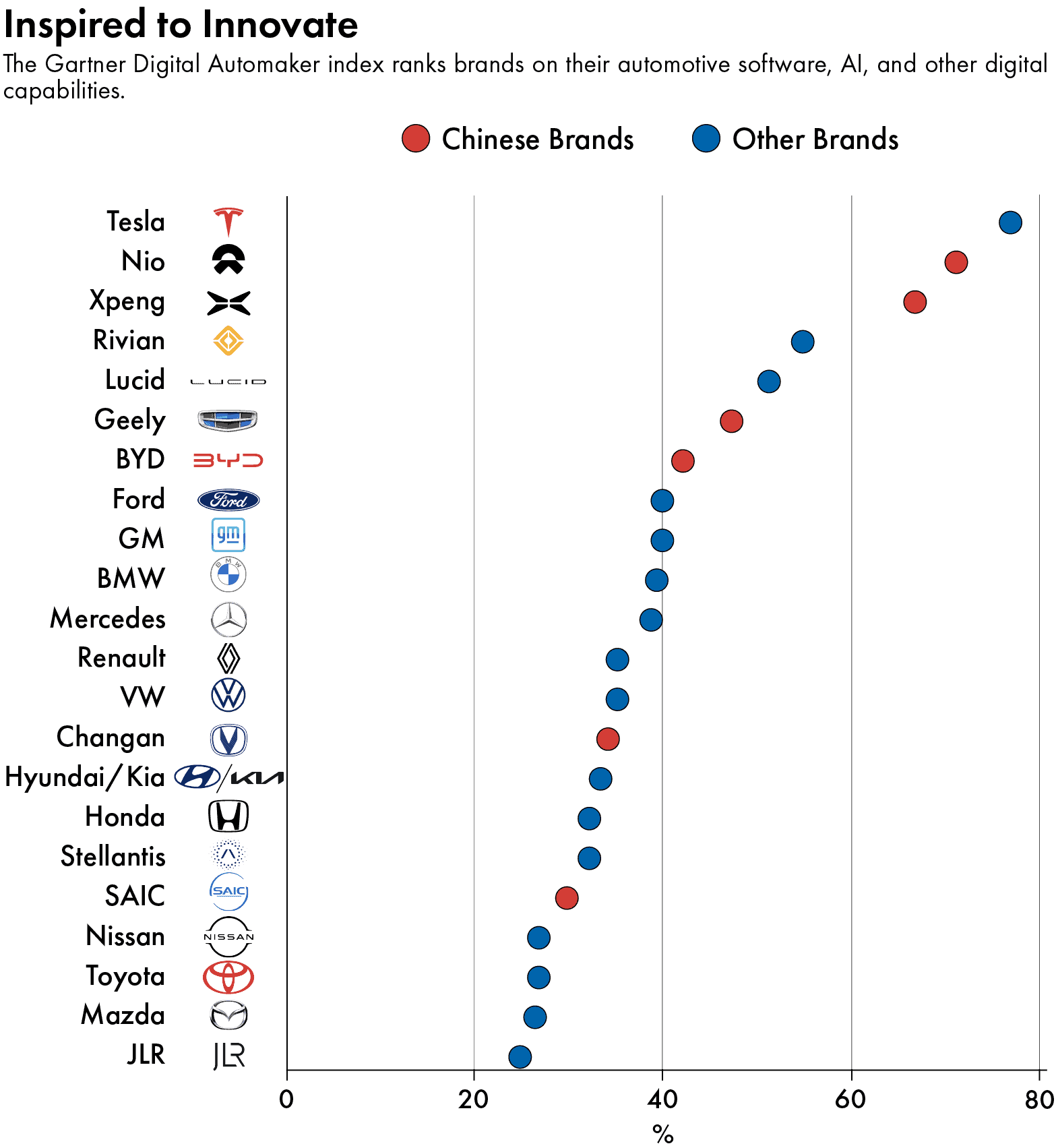

VW is still deemed a software lightweight: The consultancy Gartner ranked VW 13th in its digital performance index this year, well behind Tesla, Nio, Xpeng, and others. Only three legacy carmakers — Ford, GM and BMW — cracked the top ten.

“The legacy automakers just don’t know how to do software,” says Xing from China EVs and More. “In contrast, the founders and CEOs of emerging Chinese players come from the IT side and bring a smartphone mentality to making EVs.”

CAR’s Keim, who spent years in marketing for Volkswagen and BMW in China, has straightforward advice on how to compete with local EV brands: “Be Chinese. Cater to the Chinese driver’s needs and digitalize the car with reliable and quick software updates.”

VW seems to be trying that strategy now with its new partnership with Xpeng to reduce complexities and develop a stand-alone electrical architecture and software collaboration for its EVs in China.

Analysts say the shift for VW is to put less emphasis on ‘what the car can do’ and more on ‘what you can do in the car,’ which involves starting with fresh code that can run cleaner and faster than what VW was used to.

“Chinese customers care less about the powertrain,” says Ellinghorst, “but they do care about how the car connects to everything on their phone. A German engineer builds the car around the engine; a Chinese engineer builds around the mobile device.”

But VW isn’t only relying on the perspective of Chinese engineers.

Most notably, VW’s near $6 billion investment in California-based EV manufacturer Rivian Automotive stands out as its most ambitious move outside of China.

Rivian is best known in the U.S. as a maker of electric trucks and SUVs. For VW, however, the American upstart matters for its technology. Unlike the legacy carmaker, Rivian is near the top of Gartner’s rankings of digital automakers — even above most Chinese players. (Tesla is number one.) Similar to the Xpeng joint venture in China, VW and Rivian plan to develop an electrical architecture and software platform for new EV models by 2026.

Bolstering its U.S. stakes further, VW also acquired a 20 percent stake this year in U.S.-battery maker QuantumScape, which develops solid-state batteries that could potentially lower dependencies on Chinese supply chains.

Just as in China, there are no promises that the German automaker’s multi-billion-dollar deals in the United States will materialize into new strategic advantages globally. Its $2.6 billion investment, for instance, in American self-driving technology from Argo AI did not pan out.

But analysts say this strategy of ‘bifurcating’ global investments and technological ecosystems is a shrewd calculation.

“There is a big bet in China,” says Xing, “and there is a big bet outside of the Chinese market.”

Mütterland Last

Keeping all those investment bets straight is turning into a job for only the most advanced bookies.

With growing overlap between China and western EV industries, Ilaria Mazzocco, a deputy director and senior fellow at the Center for Strategic and International Studies, says it is difficult to discern which players count as Chinese and which do not.

“It is a matryoshka [Russian nesting dolls] of different levels of investment,” she says.

For example, VW-backed Gotion High-tech is also making investment inroads into Europe through Slovakian battery maker Inobat. With ambitious production plans in the EU and its near neighborhood, Inobat intends to leverage its tech partnership with Gotion to supply VW and others.

There’s also the Swedish brand Volvo Cars, which has been majority-owned by Zhejiang Geely Holding since 2010. Although Volvo maintains production in its hometown of Gothenburg, the acquisition has allowed the Chinese carmaker to undergo a Scandinavian makeover of its own brand in China, while still pushing forward with production of its iconic Volvo brand in the United States and other international markets.

And just last week, Stellantis announced a new, 50-50, $4.3 billion joint venture with Chinese battery maker CATL to build a large-scale battery plant in Spain.

Such ‘nesting’ opens competitive opportunities both ways, some analysts say: China’s EV advantages are certainly at play in foreign markets, but Chinese EV makers must also adjust to local preferences.

“The potential downfall for Chinese cars is that they are too digital for European customers,” says Keim.

“The wishes of the young and tech-savvy Chinese customers differ a lot from European customers who are around 20 years older on average when they are buying an e-car,” says a VW spokesperson.

VW can certainly benefit from knowing and playing both sides, but being the bridge between them may prove more challenging. For starters, the so-called “China speed” in manufacturing and new model development is partly possible because of the low pay and long hours facing Chinese automotive workers.

“There is a human aspect to the competition in that a European automaker in China cannot treat its employees like a Chinese automaker can,” Keim says.

U.S.-based human rights groups have accused automakers, including VW, of exploiting forced labor in China’s Xinjiang region. Denying the allegations, VW recently announced the sale of its Xinjiang plant to its Chinese partner for commercial reasons.

Earlier this year, thousands of VW Group luxury vehicles, including Porches, Audis and Bentleys, were also impounded by U.S. customs officials for violating regulations prohibiting the import of products made by forced labor in China’s western region.

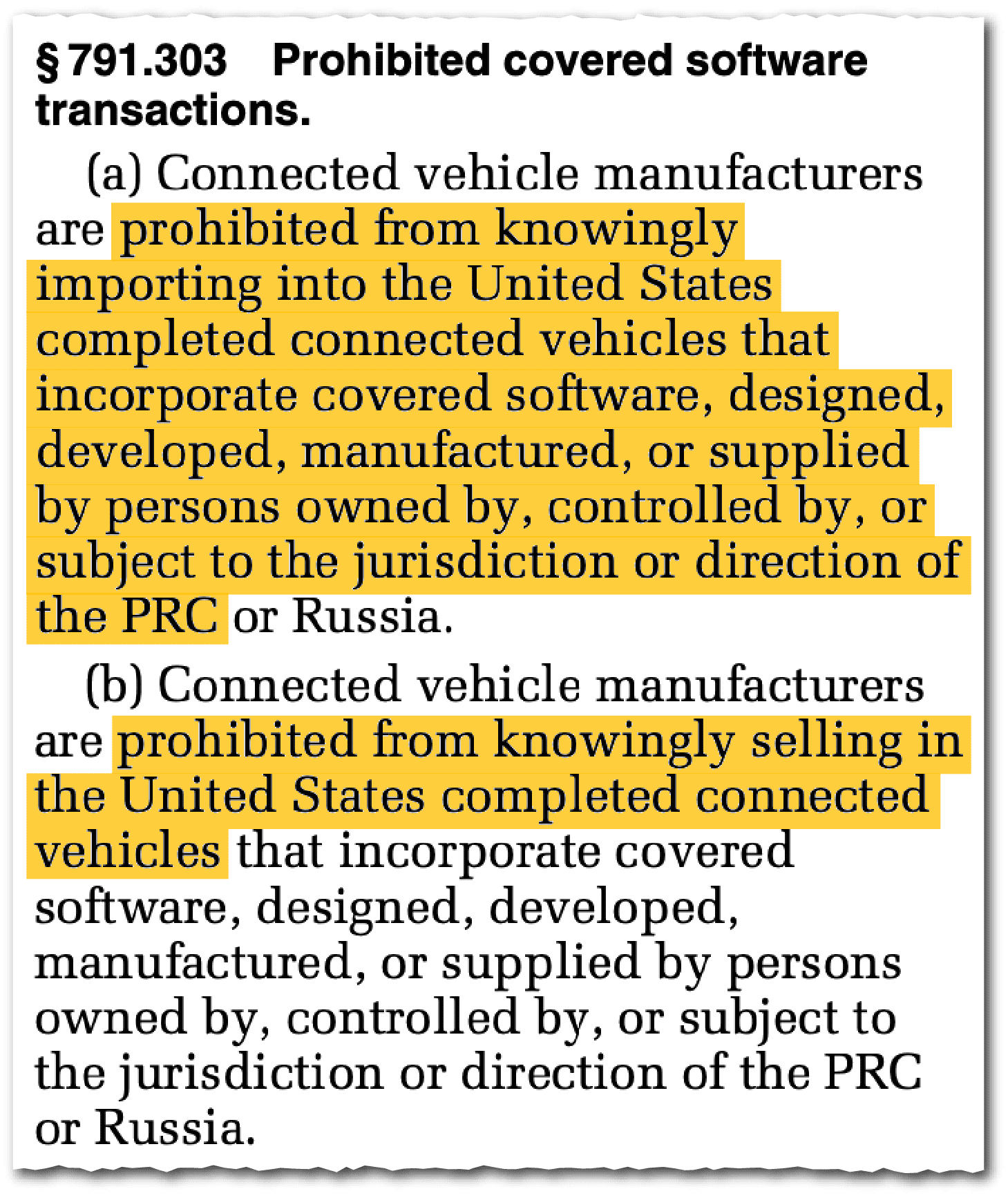

Geopolitics will also frustrate opportunities for VW to scale technology in China for its global operations, particularly when it comes to EV software and data for autonomous driving. Washington’s growing trade barriers and potential data restrictions on Chinese EVs has already done much to decouple the EV era. The return of an “America First” agenda and new tariffs from incoming President Donald Trump will only add to VW’s mounting cost troubles.

A spokesperson for the German Association of the Automobile Industry says that most vehicles exported from the EU to the U.S. contain software and/or hardware from China that would make them subject to a possible U.S. government ban. The Commerce Department’s proposed rule targets “connected” vehicles “with a sufficient nexus to the People’s Republic of China (PRC) or Russia.”

A VW spokesperson says such geopolitical hurdles are precisely “why we are developing local strategies in the major markets worldwide” — such as the Rivian investment.

But for VW, local politics matter too.

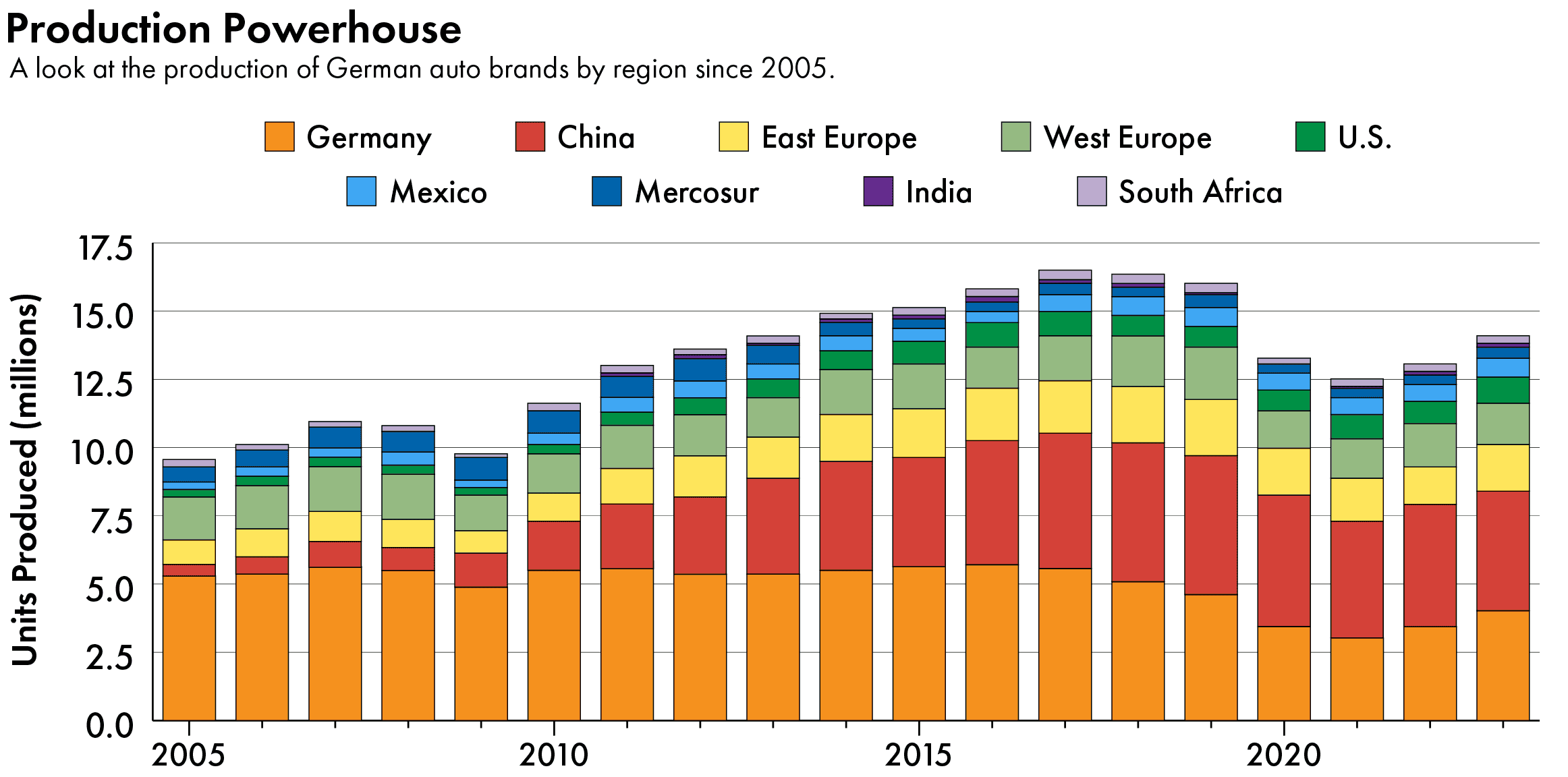

Germany’s automobile industry still makes up 5 percent of the country’s entire economy and directly employs close to 800,000 Germans. But Puls argues that the “golden age” for the industry is over. Both production and export numbers are in decline. New research from the German economist finds that, in 2023, the total production of passenger cars in Germany was roughly at the level of 1985, while exports were at the level of 1998.

Not only is VW planning to cut down its German workforce, but main auto-parts suppliers, such as Bosch and ZF, have announced thousands of job cuts of their own — even as they advance plans to open new component facilities for electric vehicles in China.

It is something of a socialization that the German business community believes that tariffs are protectionist, and protectionism is bad for our export model. Maybe it is in our genes.

Jürgen Matthes, a senior economist at IW

The moves, of course, make some immediate sense: German brands now manufacture more vehicles in China than they do at home. (Last year, they produced less than 30 percent of their total vehicles in Germany.) But, says Xing, “in the last few years, we’ve seen the emergence of interesting Chinese component players that may very well disrupt traditional tier one players.”

“In auto electronics and braking systems there are still a lot of foreign suppliers that dominate the market,” adds Sebastian, from Rhodium. “If Volkswagen was to suddenly adopt a Chinese braking system, that would be a huge development.”

Thus far, the German government has been supportive of VW’s and other German brands’ China choices. The country has a proud tradition of adhering to market ideology, and “there is a very doctrinaire free trade and open competition mentality among many German politicians and policymakers,” says Xie.

Chancellor Olaf Scholz even overruled his own coalition government partners in voting against the EU’s EV tariffs.

“It is something of a socialization that the German business community believes that tariffs are protectionist, and protectionism is bad for our export model,” adds Jürgen Matthes, a senior economist at IW. “Maybe it is in our genes.”

But the layoff announcements from automakers and auto-parts suppliers in Germany coupled with their new investments in China can disturb even the most devoted worshiper’s beliefs. With a national election rapidly approaching in February, Chancellor Scholz called on VW to not close any German factories, but at the same time, he has extended a helping hand to industry by advancing tax exemptions, and promoting a new European-wide subsidy, to boost EV sales.

German companies want protections too. A survey conducted by Matthes found that 80 percent of German businesses said the Commission’s countervailing duties against Chinese-made EVs were at least partly justified on the basis of China’s market distortions.

Still, the tariffs may not be enough to halt sales growth from the lead Chinese EV maker BYD and Chinese-owned brands like Volvo in European markets. Even with an overall decline in the EU’s EV market so far this year, BYD sales doubled in October compared to a year earlier. (By contrast, Chinese-made EVs may be virtually shut out of the U.S. market by a wall of tariffs and restrictions.) BYD and other Chinese brands are also selling a growing number of hybrid models in the EU to avoid the new EV tariffs, and they are making deep inroads in third markets such as Brazil and Mexico at the expense of legacy players.

So far, low price points and software have fueled Chinese brands’ popularity, but many in Germany argue that after playing digital catch up, long-honed German competitive advantages in the “driving experience” may just pay off.

As the spokesperson from the German Association of the Automobile Industry explains, this entails “the coordination of all individual systems in the vehicle” that “create a harmonious overall experience, the ‘vehicle as if from a single mold.’”

For Volkswagen, rather than relying on a single uniform beacon extending out of its troubled heartland to create this product, it has invested tens of billions of dollars in new technologies and production capacities in disparate geopolitical locales. Whether the German automaker will stay standing strong in the decades to come will depend on how well it can finagle all the moving parts it has set into motion into a single, harmonious mold.

Back at the Transparent Factory in Dresden, meanwhile, while rumors swirl that ID.3 production may soon be stopped, there are also rumblings of a new e-Golf model sporting Rivian architecture and software — a model that could conceivably roll off VW assembly lines in Germany one day.

Luke Patey is a senior researcher at the Danish Institute for International Studies. He is author of How China Loses: The Pushback Against China’s Global Ambitions. His work has been published in The New York Times, Financial Times, The Guardian, The Hindu, Foreign Affairs and Foreign Policy. @LukePatey