Beijing whipped out its flashiest gadgets for the 2022 Winter Olympics: Robots flipped burgers and served meals at the canteens, a green cooling system used carbon dioxide to keep ice rinks cold, and smart beds monitored the heart rates and breathing of athletes as they slept.

But in its effort to cement its role as an innovation powerhouse, China’s most ambitious technological debut was also its most controversial: The digital yuan was rolled out as the legal tender of choice for the Olympic games. Instead of cash or Visa (the corporate sponsor that had dominated the sports event for three decades), visitors were encouraged to exchange foreign currencies for digital yuan at automated teller machines and to pay digitally through the e-CNY app on their phones or through a card that can be used offline.

The experience would allow visitors to “take a dip into the convenience of mobile payments in China,” said Mu Changchun, director-general of the Digital Currency Institute at the People’s Bank of China (PBOC). China had led the revolution to go cashless with fintech giants Alipay and WeChat Pay, and it was now the first major economy to introduce a digital form of fiat currency. A successful Olympics trial would give the digital yuan international clout, Chinese state media reported.

But in the West, observers watched with trepidation and suspicion. Much like China’s social credit score, the digital yuan rollout seemed like another example of “digital authoritarianism.” Jeremy Fleming, head of the UK’s intelligence agency at the time, warned that it could be used as a surveillance tool to monitor transactions. American officials grew concerned that it would enable China to challenge the dollar as the world’s leading reserve currency. Ahead of the Olympics, then-Senator Pat Toomey (R-PA) wrote to both the secretaries of State and Treasury demanding a briefing on “e-CNY’s potential to subvert U.S. sanctions, facilitate illicit money flows, enhance China’s surveillance capabilities, and provide Beijing with ‘first mover’ advantages, such as setting standards in cross-border digital payments.”

Yet, despite all the attention, the launch of the digital yuan largely fell flat. The COVID-19 pandemic meant Olympic visitors were confined to “bubbles” with little opportunity to travel, shop and dine out, and very few foreigners chose to use the digital yuan over their credit cards. Beijing saw just $315,000 in digital yuan processed every day over the course of the games — a small fraction of the usual revenues at the Olympics. At the 2008 Olympics in Beijing, for instance, the city generated roughly $264 million per day.

“People thought this was going to be a really big coming out party for the digital yuan,” says Martin Chorzempa, a senior fellow at the Peterson Institute for International Economics. “But it was very, very muted.”

The larger crypto craze, meanwhile, also began to fizzle around this time. Just a few months after the Olympics, FTX, the digital currency exchange behemoth that had a valuation of $32 billion, filed for bankruptcy in the United States. Although central bank digital currencies (CBDC) like the digital yuan are not the same as cryptocurrencies, the general enthusiasm for — and attention to — digital currencies in all their forms died down.

“e-CNY and retail CBDC in general were overhyped,” notes Chorzempa, author of The Cashless Revolution: China’s Reinvention of Money. “It’s very sensible that we’re coming back to Earth on both accounts.”

But while China acknowledged its Olympic failure, it has also quietly doubled down on the digital yuan, including a big push to drive adoption. Last year, several cities began paying civil servants and collecting taxes in digital yuan. Jiangsu province saw the most recorded transactions in the country after it gave away 30 million yuan ($4.18 million) in digital “red envelopes.” And this past May, the digital yuan expanded for the first time outside of mainland China when it became available for use in Hong Kong. Though there is no timeline for a nationwide launch yet, China has rolled out pilot schemes in 26 cities and 17 provinces since 2019.

The efforts have paid off. In a press briefing last week, the PBOC announced that total transactions reached $7 trillion yuan ($982 billion) in June — a four-fold jump since last June.

Digital yuan usage is still only a fraction of China’s $40-trillion payment market, of course. The total number of e-CNY wallets opened — 120 million as of last July — also trails behind that of Alipay, which had over a billion users by 2020 and recorded $118 trillion worth of transactions in one year alone.

But as Beijing continues to crackdown on its fintech giants, it is creating room for the digital yuan to rise. In fact, officials see the transition to digital currency as both necessary and inevitable. According to Yi Gang, former governor of the PBOC, the current moment of transition is not unlike that of the Ming Dynasty, when the government started taking tax payments in silver instead of labor and grains. China’s currency has evolved with time, he said during a speech at Fudan University in April, and “the digital yuan is no exception.”

MONEY TALKS

The People’s Bank of China set up a task force to study the feasibility of a national digital currency as early as 2014. It had formed a prototype by 2016. But the efforts took on a new urgency around 2019, as the rise of cryptocurrencies backed by the U.S. dollar threatened to make fiat currencies less desirable.

Facebook’s proposed Libra coin, for instance, promised a “global currency and financial infrastructure that empowers billions of people.” With its extensive reach, users could send money as easily as a text message. As one group of academics put it, Libra was “a wake-up call” for anyone who still sees “the issuance of currency as a unique function of the state and central banks.”

“Libra generated a lot of interest for central banks around the world — not just the PBOC,” says Josh Lipsky, senior director of the Atlantic Council’s GeoEconomics Center and former advisor at the International Monetary Fund. “They were asking, ‘If there will be these dollar or Western reserve currency-backed stablecoins, do we need our central banks to offer our own form of digital asset?’”

Mark Zuckerberg testifies before congress regarding Facebook’s cryptocurrency Libra, October 23, 2019. Credit: C-SPAN

For China, the answer was a resounding yes. In July 2019, less than a month after Facebook announced Libra, Huang Yiping, a Peking University professor who sat on the monetary policy committee of PBOC, warned that Libra could “overtake China on a bend.” Wang Xin, director of the Chinese central bank’s research bureau, said that if a digital currency closely associated with the U.S. dollar takes off, “there would be in essence one boss — that is the U.S. dollar and the United States.” Its arrival, he added, “would bring a series of economic, financial and even international political consequences.”

Libra never did take off due to regulatory pushback in the United States, but that didn’t stop Beijing from taking action. In 2021, it announced a blanket ban on all cryptocurrency transactions and mining. At the same time, it accelerated the development of the digital yuan. A 2021 white paper laid out the framework, including a two-tier model that ensures the digital yuan doesn’t cut out private financial institutions. Instead, the central bank issues the e-CNY to commercial banks, which in turn distribute it to consumers.

[CBDC] is a beautiful solution to a problem that doesn’t exist. It is compelling for the government because it provides visibility and control. e-CNY solves a problem for the government, not necessarily for the people.

Zennon Kapron, founder of the fintech consultancy Kapronasia

China is among 36 countries that are in pilot phases, according to a study last year from the Atlantic Council’s CBDC tracker, but it has quickly emerged as the pace setter. “They were able to build a pilot that could scale to hundreds of millions [in transactions] while other countries were still in the exploratory phase,” notes Lipsky.

The idea of a digital currency appeals especially to emerging economies, many of which, like China, are keen to create a more efficient payment system, promote financial inclusion and reduce their dependence on the dollar. Only Jamaica, the Bahamas and Nigeria have officially launched their CBDCs, but 130 countries — representing 98 percent of the global GDP — are exploring the use of digital currencies.

For China, launching the e-CNY when it did “became a matter of establishing leadership for prestige and technology reasons, and potentially for commercialization internationally,” says Darrell Duffie, a finance professor at Stanford University.

“They’re going at it very, very effectively in terms of building out the whole ecosystem of e-CNY,” Duffie adds. “The only thing that’s missing is that the people are not really using it.”

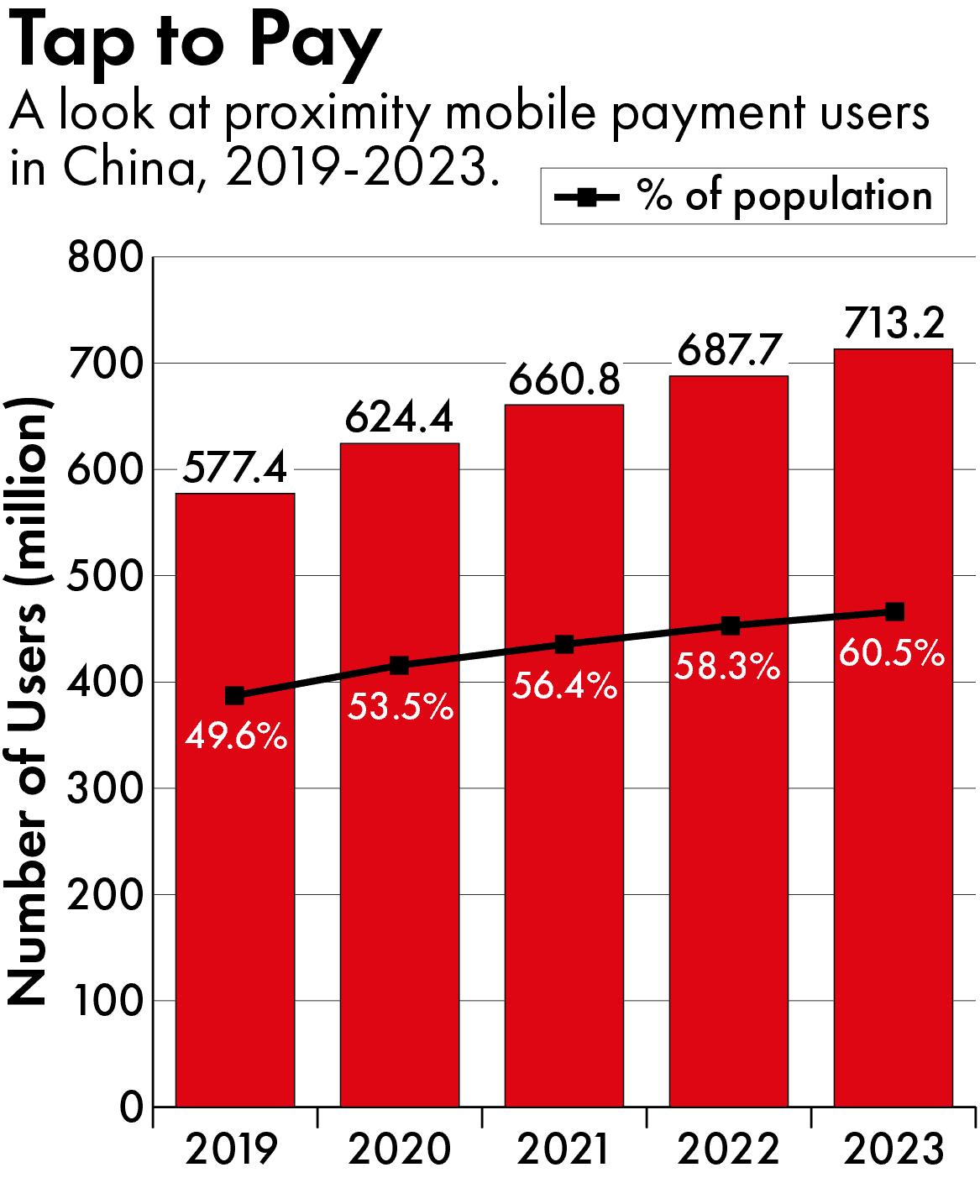

Indeed, while the Chinese government kept an eye on foreign technology like Libra, it didn’t quite take stock of what was happening in its own backyard. Alipay and WeChat Pay, which emerged in the early 2010s, moved at a much faster pace than e-CNY and have essentially taken over the digital yuan’s space. By the end of the decade, the duo dominated the mobile payment market in China with over 90 percent share. They have also grown into “super-apps,” where users can do everything from taking out loans and paying utility bills, to buying plane tickets and ordering take out.

“[CBDC] is a beautiful solution to a problem that doesn’t exist,” says Zennon Kapron, founder of the fintech consultancy Kapronasia. “It is compelling for the government because it provides visibility and control. e-CNY solves a problem for the government, not necessarily for the people.”

Though Chinese bank officials insist the digital yuan is meant to complement, not compete with, commercial payment services, officials tried to rein in the duopoly in late 2020.

Credit: Tencent

First, regulators halted the blockbuster initial public offering of Ant Group (the owner of Alipay), and then overhauled the company and its management. In 2021, authorities slapped a record $2.8 billion antitrust fine on the group. Meanwhile, Tencent, the owner of WeChat Pay, received a $410 million penalty for violations in consumer finance protection, among other regulatory breaches. WeChat is now under pressure to lower its share of the mobile payment market and “is very cautious about the potential risks of growing too big,” Nikkei Asia reported earlier this year, citing sources familiar with the matter.

The crackdown kept the fintech giants in check, but it did little to shore up the digital yuan. Even after the clampdown, the use of WeChat Pay and Alipay has become so entrenched among the population that very few see the need for an e-CNY wallet. It doesn’t help that the e-CNY wallet has far more limited functions, including not offering interest, and that the government has not yet provided the necessary hardware for merchants to accept e-CNY.

Left: The services offered in the e-CNY wallet. Right: The services offered in Alipay’s application.

Screenshots provided by author.

China’s dilemma is echoed in other countries such as India and Brazil where CBDCs have also struggled to compete with popular existing digital payment systems.

“It’s not very useful to have a retail central bank digital currency in a country that already has extremely high penetration of digital payment tools that work really well,” says Chorzempa, of Peterson Institute. “The marginal benefit of making a central bank digital currency is very low, but the cost of building out a duplicative set of retail payment infrastructure is very high.”

In an effort to attract users, the Chinese government is exploring integrating the e-CNY wallet with existing payment tools, so that the funds that circulate on WeChat Pay or Alipay may also be digital yuan. Right now, for instance, users can connect their e-CNY wallet to Alipay and transfer money between them.

Officials are also trying to expand the scope of e-CNY beyond consumer retail transactions. The Bank of China, for instance, has tested the use of “smart contracts” for afterschool programs in Chengdu of Sichuan province: Parents can pay a deposit in e-CNY to educational institutions, and the latter only receives the money after the lessons are taken.

These business-to-business and government programming applications could be a “game changer,” according to Warwick Powell, a senior fellow at Taihe Institute, a Beijing-based think tank, because they “ensure that the provision of certain funds can only be used for certain activities.”

Yet that same function triggers concern for others. For instance, although some local governments and banks have offered loans in e-CNY, companies are reluctant to take them, says Yang You, a finance professor at University of Hong Kong. “The nature of e-CNY is that a policymaker can generate a loan and see where it flows to,” says You. But companies, he notes, would much prefer non-traceable loans, despite repeated assurances from the People’s Bank of China that it will not hold information against them.

The issue of trust — and privacy — is central to criticisms of the digital yuan. If the central bank can easily see and track all payments, the thinking goes, it can be used as a surveillance tool for social or political control. A digital currency would never work in the U.S., Federal Reserve chairman Jerome Powell said in a press briefing in 2021, since it “allows the government to see every payment that’s used in real time.”

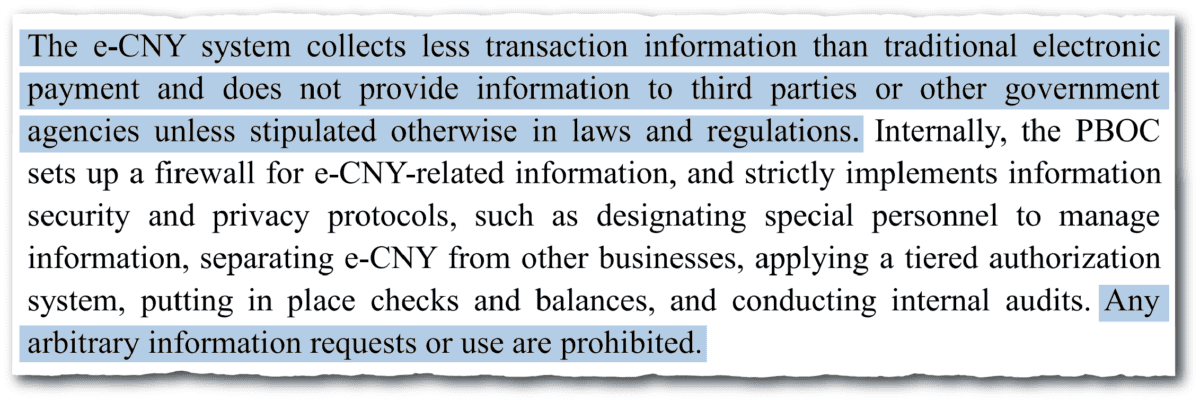

Chinese central bank officials have argued that is not their intention. Instead, the PBOC says the digital yuan follows a principle of “anonymity for small value and traceable for high value” as a way of striking a balance between privacy protection and combating criminal activities, such as tax evasion and money laundering. The e-CNY wallet, for instance, requires users to undergo a more complex verification process in order to unlock higher transaction limits. But while many central banks are bending over backwards to assure users they would not hand over data to authorities, “the situation in China is different,” notes Duffie.

THE LONG GAME

In 2019, several scholars and former government officials gathered before a packed audience at the Harvard Kennedy School to debate how to respond to a fictional national security crisis. In the simulation, North Korea had tested an intercontinental ballistic missile that landed in the Philippine Sea. North Korea was able to defy sanctions and purchase the raw nuclear materials for the weapons without alerting the U.S. thanks to none other than the digital yuan.

“We may be moving into a world where the U.S. is not financially dominant,” said Meghan O’Sullivan, a Harvard professor and former deputy national security adviser who was playing the role of Vice President.

Five years and two new wars later, experts say America’s underlying concerns about digital currencies are just as relevant. If anything, the search for an alternative to the U.S.-backed Swift, the global messaging network for the banking system, has gained momentum since the U.S.-led sanctions on Russia.

“China has used the sanctions as a reason to advance the cause of de-dollarization,” says Elizabeth Economy, a senior fellow at the Hoover Institution at Stanford University and recent advisor to the Department of Commerce. “It has made the case that the United States is weaponizing the dollar, hence other countries should begin to trade in their own currencies. It’s actually a deft diplomatic move on the part of China.”

According to the Bank of International Settlements (BIS), a survey of 86 central banks last year showed a sharp uptick in experiments with “wholesale CBDC” — transactions between banks and other financial institutions, rather than consumers and businesses. In October, for instance, the e-CNY set a new milestone: At the Shanghai Petroleum and Natural Gas Exchange, the state-owned PetroChina used digital yuan to purchase a million barrels of oil from an undisclosed seller.

“There’s still a conversation about the e-yuan [for domestic retail transactions], but there’s more discussion about a regional payment system,” says Victor Shih, an associate professor of political economy at the University of California. “An alternative to Swift potentially has more legs.”

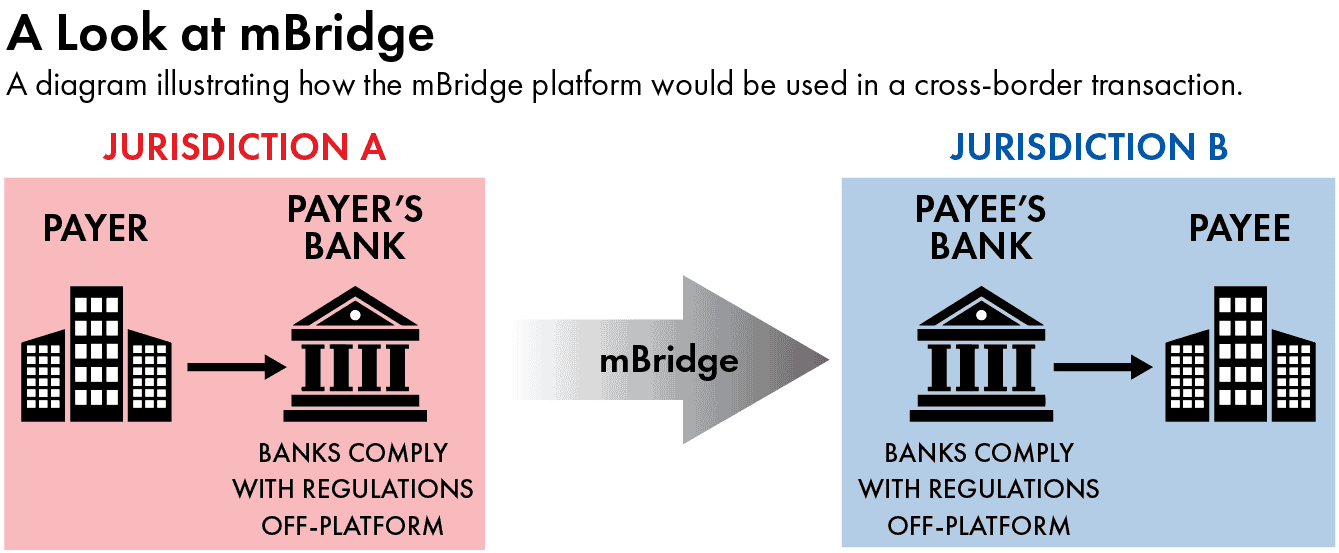

The oil purchase seems to be a one-off so far, but a new project called mBridge hopes to make such transactions routine. It is a collaborative effort between the “innovation hub” of BIS and the central banks of five jurisdictions: China, Hong Kong, Thailand, United Arab Emirates, and most recently, Saudi Arabia.

A video on Project mBridge from the Bank for International Settlements. Credit: BIS

Underpinned by distributed ledger technology (which records transactions in multiple places at the same time), mBridge aims to be a multi-CBDC platform that can support instant cross-border payments. The idea is to make international settlement faster and cheaper than Swift. But it also means things are not dependent on the U.S. dollar.

“Swift had a number of disadvantages, and they basically related to cost and time,” says Powell, of the Taihe Institute. “Now we have seen the emergence of other concerns, namely that the messaging system is subject to the capricious censorship of single actors. And therefore, relying upon the Swift communications infrastructure to send messages between banks opens yourself up to sanctions that are unilaterally imposed by third parties.”

The BIS Innovation Hub is also working with other central banks — including that of France, Switzerland, Australia and Malaysia — on separate experiments. But mBridge, which started in 2021, is considered the most advanced. During a six-week pilot in 2022, 20 banks from four jurisdictions used the platform to settle $22 million worth in transactions on behalf of corporate customers.

Kapron, the fintech consultant, notes that mBridge still has a ways to go. “Ten thousand banks are on the Swift platform and using it every day,” he says. “That is what mBridge needs to be able to accrue.”

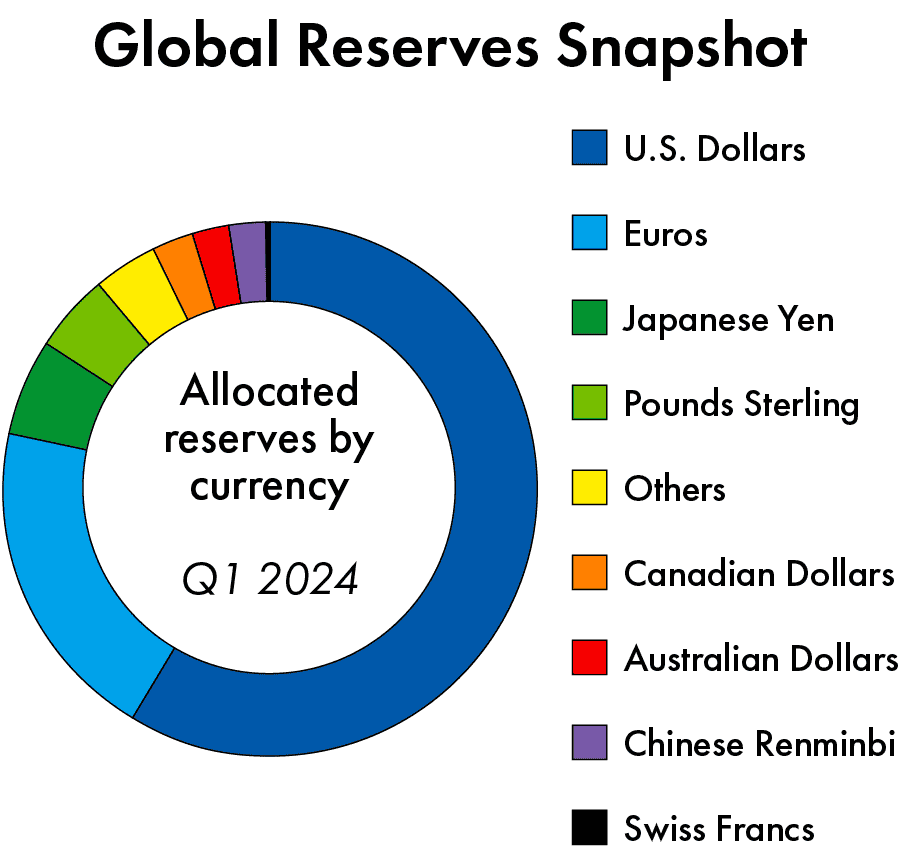

It can be tricky to rightsize the risk to the U.S. of a digital yuan as well as China’s efforts to internationalize it. On the one hand, the renminbi’s share of global payments has gradually increased from around 2 percent in 2020 to a record high of 4.74 percent in July. It even overtook Japan’s yen last year as the fourth most active currency, according to data from Swift.

But the dollar’s share is still 47.81 percent. As Lourdes S. Casanova, director of the Emerging Markets Institute at Cornell University, notes the dollar’s dominance has contributed to American reluctance to even experiment1The House of Representatives passed a bill in May barring the Federal Reserve from creating a digital dollar without approval from Congress. with a CBDC: “Why bother if you have a currency that dominates the financial sector?” Many experts say that even if a system like mBridge gets off the ground, it won’t do much to help the yuan unseat the dollar.

“The notion that digitization of the yuan will increase its role in international finance is a chimera,” says Eswar Prasad, a professor at Cornell University and former head of the International Monetary Fund’s China division. “The dollar’s strengths lie not just in the depth and liquidity of U.S. financial markets but also the institutional framework that underpins the currency’s status as a safe haven.”

Fundamental problems in China’s economy — such as stringent capital controls and forced stabilization of the exchange rate — also make trading the yuan unappealing.

“If you want [a stable exchange rate], you cannot have a large pool of renminbi being traded by speculators overseas,” says Shih. “Just by definition, you can’t internationalize the currency.”

But Economy, at the Hoover Institution, warns that the U.S. hasn’t seen the last of the digital yuan. “One thing about China is, it doesn’t give up,” she says, citing the decades-long effort China undertook to become the global leader in electric vehicles. “If it takes Chinese leaders another ten or fifteen years with some modifications to gain both national acceptance and to have a global system in which the e-CNY is a big player, they’re going to do it.”

Rachel Cheung is a staff writer for The Wire China based in Hong Kong. She previously worked at VICE World News and South China Morning Post, where she won a SOPA Award for Excellence in Arts and Culture Reporting. Her work has appeared in The Washington Post, Los Angeles Times, Columbia Journalism Review and The Atlantic, among other outlets.