Credit: Wingtech

Chinese investors are proving less ready to splash their cash overseas.

Numbers through November from the Chinese government showed $95 billion in overseas non-financial deals, which make up only a part of all overseas funding. However, the China Global Investment Tracker (CGIT), run for years by the American Enterprise Institute and the Heritage Foundation, found just $30.5 billion worth of significant investment and construction deals over the entire year.1CGIT only tracks deals worth $95 million or more, so smaller deals will account for some of the discrepancy. The CGIT data, which in the past have tended to be more in line with official Chinese figures, indicate that China’s dealmaking overseas peaked in 2016 and 2017, and has declined in every year since.

The global pandemic is likely to have delayed some transactions last year. But the figures also reflect growing unease about Chinese acquisitions, particularly in the U.S. and other Western countries. Perceptions of Chinese companies as predatory investors have limited some countries’ willingness to accept their funds, particularly amid a global economic slump that has made some assets appear cheap.

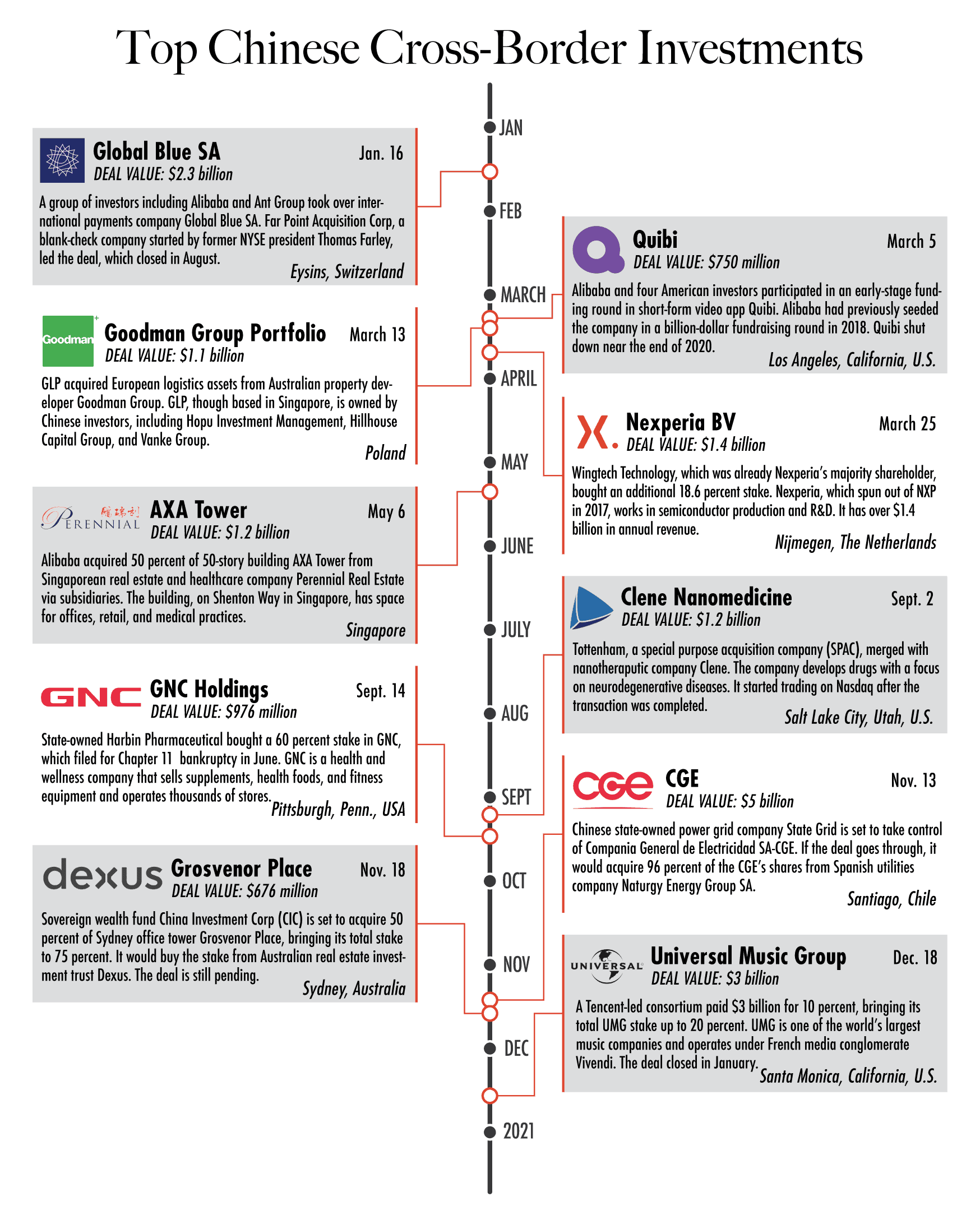

Even some of the deals announced last year might be less viable now as conditions rapidly shift. Chinese electronics manufacturer Wingtech’s 2018 acquisition of Nexperia — bolstered last March when Wingtech bought an additional 18.6 percent stake in the Dutch semiconductor producer for $1.4 billion — is one deal that might face greater hurdles if done today. “[Until recently] people didn’t see China or semiconductors as a big strategic issue,” says James Lewis, the director of the Strategic Technologies Program at the Center for Strategic and International Studies (CSIS). “Now, it would be a lot bumpier ride.”

Chinese companies’ appetite for overseas acquisitions also appears to have dimmed. Heavier restrictions on outbound investment imposed by a warier government have stymied their global ambitions. Even lending and investment under the government’s flagship Belt and Road Initiative has reportedly faded. This week, The Wire examines the top cross-border M&A deals in 2020 to see what they might reveal about China’s FDI dip, and the potential for a recovery this year and beyond.

Tencent Leads

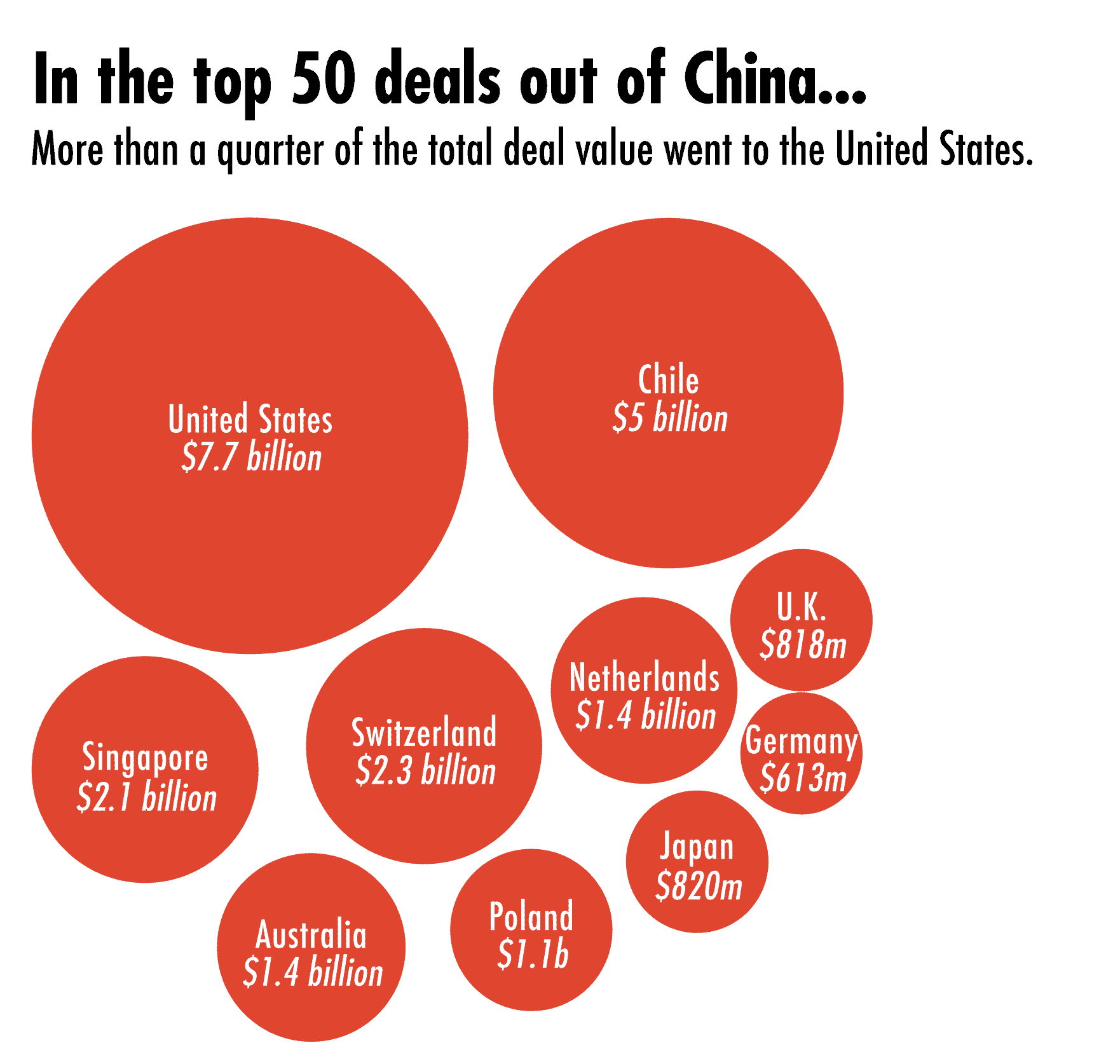

While the top 50 cross-border investment deals announced globally in 2020 amounted to nearly $450 billion in value, the top 50 deals out of China and Hong Kong were worth just $28 billion, according to data provider Dealogic.2Different sources track dealmaking in different ways. Most commonly, the date, and therefore year, for a transaction will be counted by when it was announced, filed, or closed. Only State Grid’s pending $5 billion purchase of Chilean power grid company CGE cracked the global list. The world’s biggest deals were S&P Global’s $43 billion acquisition of U.K. data firm IHS Markit and AstraZeneca’s $39 billion acquisition of U.S. drugmaker Alexion Pharmaceuticals.

While the U.S. has grown more wary of Chinese investment, it was still the leading destination for Chinese outbound deals, according to Dealogic. Some of last year’s largest transactions were Tencent’s $3 billion pending purchase of a 10 percent stake in music industry titan Universal Music Group and Harbin Pharmaceutical becoming the majority owner in bankrupt health and wellness company GNC for just under $1 billion.

Most analysts expect that any recovery in Chinese foreign investment will be uneven. Western opposition to Chinese investment could result in proportionately more funds going to Latin America and Belt and Road countries — largely in the Middle East and Northern Africa — as the global economy recovers, according to AEI Resident Senior Fellow Derek Scissors, who maintains the CGIT. Another factor is Covid-19: Several countries’ economies, such as India’s and Brazil’s, are stalled as their battle with the virus rages on.

China’s state-owned enterprises might also lead the way more in making billion-dollar investments in future, due to the hostility that many of the country’s biggest private companies are facing at home and abroad, experts say. “If you feel like you might be attacked as a firm in China, to say we’re spending lots of money in another country — state-owned enterprises can get away with that,” says Scissors. “I think you’re going to get a cautious private sector for most of this year.”

Biggest Border Crossers

Though major Chinese deals are often examined for political or strategic motives, many involve well-financed and large entities looking to find investments that will provide stable returns, in areas such as resources or top-tier real estate.

State Grid, for example, increasingly commands Chile’s power grid: the company said it would pay $2.2 billion for control of electricity distributor Chilquinta, which provides power to 2 million people, in late 2019, in addition to its pending $5 billion CGE stake. The likes of Alibaba, GLP, and China Investment Corporation (CIC) all meanwhile made pricey investments in international property last year. CIC’s pending $676 million purchase of the majority stake in Australian office tower Grosvenor Place is in line with its other investments, which include holdings in major New York City office buildings.

One oddity of the recent craze for special purpose acquisition companies, or SPACs, is the way it can distort cross-border investment data. Take the recent $1.2 billion deal in which Clene Nanomedicine, a Utah-headquartered drug development company, merged with Hong Kong-based SPAC Tottenham, in order to list on Nasdaq. While technically this was a cross-border deal, “presently, there’s no connection at all to Hong Kong, in terms of the company, save that we have key advisors and investors in the region advising Clene, as we also have investors from Korea and Japan,” Clene CEO Rob Etherington told The Wire.

Nexperia as New Strategy

News broke in 2018 that Wingtech was set to acquire a majority stake in semiconductor producer Nexperia, which says it now controls 14 percent of the global semiconductor chip market. Netherlands-based Nexperia has a significant R&D and sales presence in Asia, despite its headquarters and fabs still being in Europe.

Wingtech was founded in 2006 and manufactures electronics for major Chinese smartphone makers like Xiaomi. Its purchase of a further 18.6 percent of Nexperia means it now owns nearly all of the company, having initially paid $3.79 billion for 79.98 percent of Nexperia.

The acquisition plays into China’s larger push for chip independence. Two other NXP arms have been acquired by Chinese groups in recent years, as well. “This is the fourth or fifth time the Chinese have tried to build their own semiconductor industry — it’s always failed in the past because they don’t have the know-how,” CSIS’s Lewis says. “About five years ago, the Chinese came up with a new strategy and that is, ‘We don’t have the know-how, we’ll buy companies that have the know-how, and that’ll get it to us.’” Lewis said this change in strategy is partly what has driven the United States to start scrutinizing and blocking Chinese takeovers.

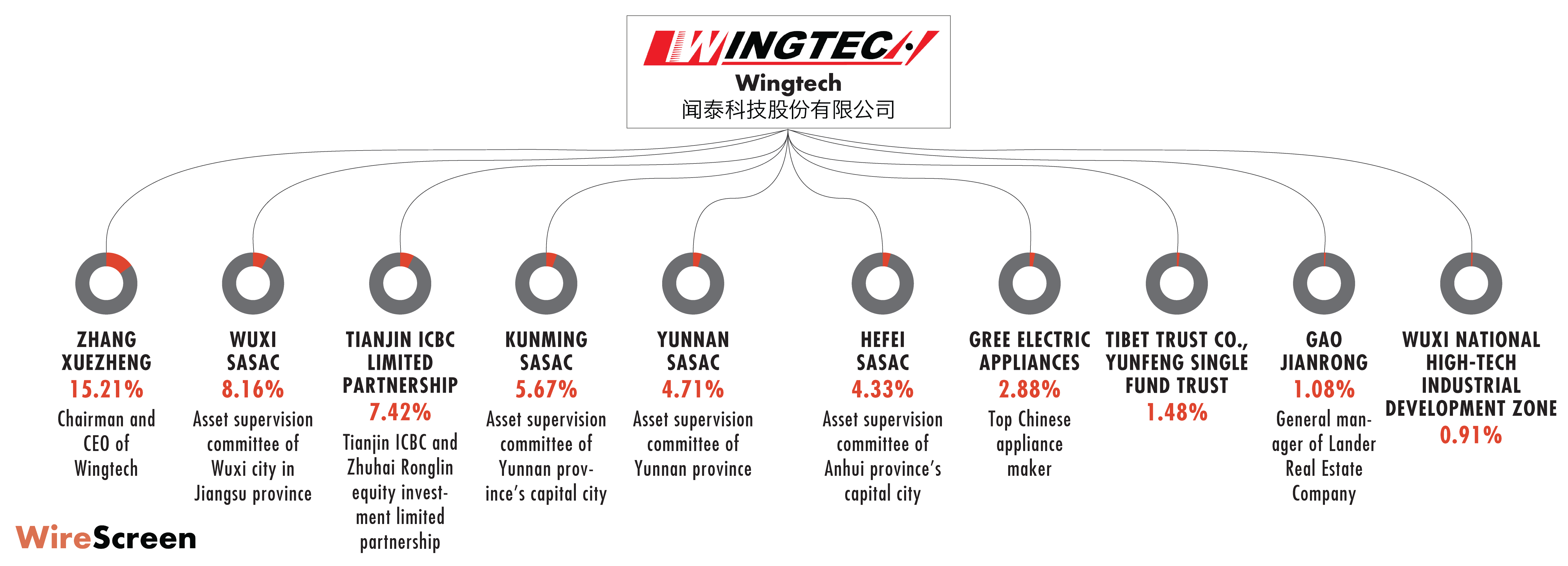

Below are the biggest ultimate stakeholders in Wingtech below.

Hannah Reale is a staff writer with The Wire. Previously, she reported for the GBH News Center for Investigative Reporting, The West Side Rag, and her college newspaper, The Wesleyan Argus. @hannahereale