Dongfeng, an impoverished village in Jiangsu Province, was once characterized as a mere “dumping ground,” because its economy was heavily reliant on plastic waste recycling. This bleak situation led to an exodus of young adults seeking employment opportunities in cities, with one villager even lamenting that “if an elderly person died, the village would not be able to muster four able-bodied men to carry the coffin.”

Han Sun, born in 1982, was among the young people who left Dongfeng to pursue a better life. After dropping out of college, Sun attempted various occupations — gatekeeper, mover, and even background actor in Hengdian (known as “China’s Hollywood”) — but he struggled to find the right fit.

During a casual visit to IKEA’s Shanghai store in 2007, however, Sun was inspired by the idea of producing and selling furniture similar to IKEA’s offerings. Leveraging a prior experience in e-commerce where he sold prepaid phone cards, he decided to return to Dongfeng Village and embark on a new online venture. Given the absence of skilled carpenters in the village, he recruited several coffin makers to manufacture furniture, which he subsequently sold on Taobao.com, an online platform that was founded by Alibaba in 2003.

The online business immediately took off, with furniture sales exceeding 100,000 RMB ($13,700) within the first month alone. And the momentum continued to grow.

Since Chinese rural villages are ungated communities where everyone knows each other, gossip travels fast. After observing a truck routinely picking up packages from his backyard, Sun’s fellow villagers soon discovered his money-making formula and promptly copied it. With more households joining the e-commerce frenzy, Dongfeng Village blossomed into a bustling hub for online furniture sales.

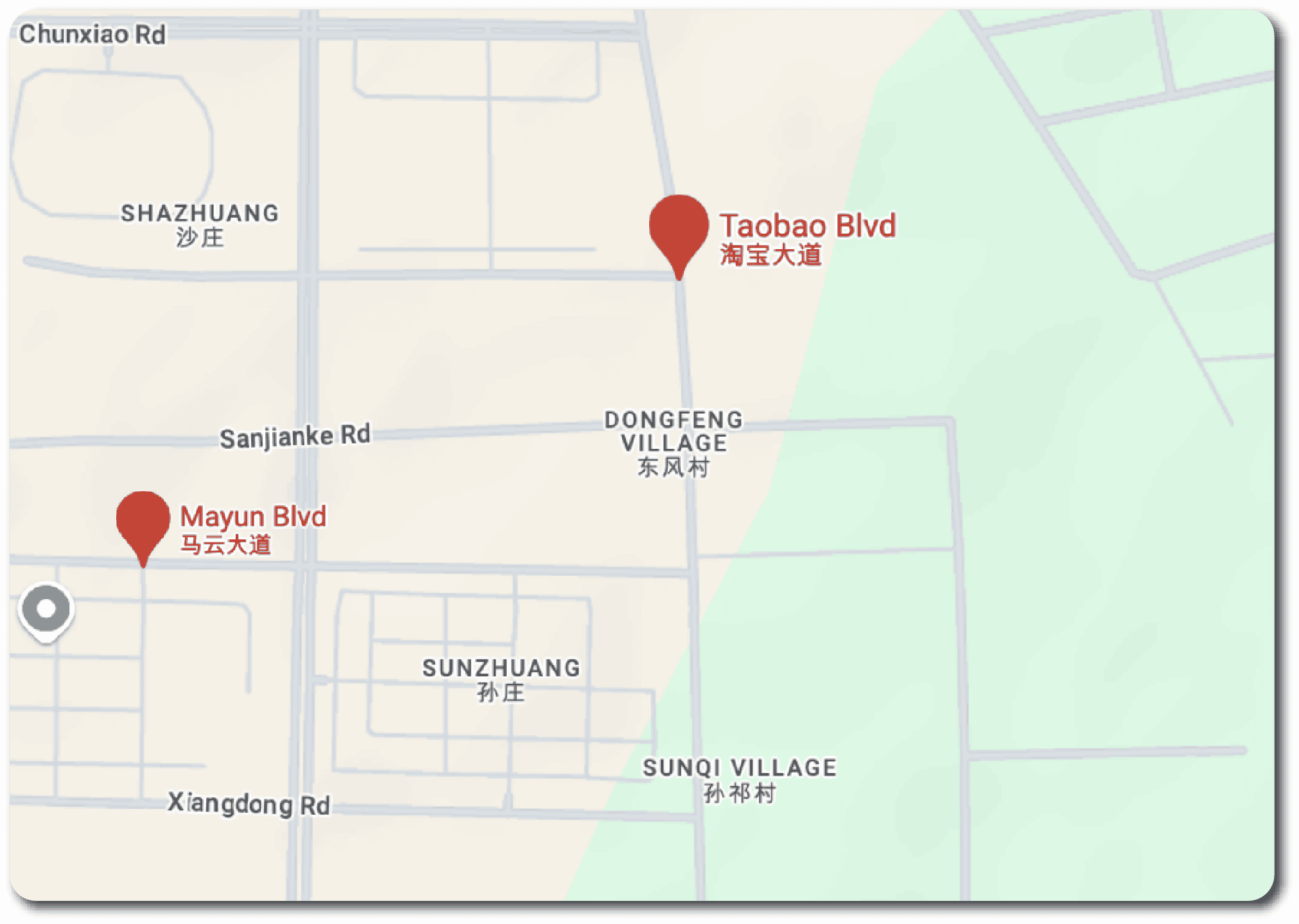

By 2014, the small village hosted over 2,000 online stores, surpassing its own household count of 1,180. Its online furniture sales alone raked in an impressive annual revenue of more than 1.3 billion RMB ($210 million). When I first visited that year, I strolled along several roads that were aptly named to commemorate the village’s remarkable rise in e-commerce, including “Taobao Avenue” and “Ma Yun Avenue,” which paid tribute to the Chinese name of Jack Ma (Ma Yun), the founder of Alibaba.

Online traders I interviewed told me that e-commerce not only brought wealth to the village; it also triggered a social transformation by reversing the village’s earlier labor drain. Young people are now much more likely to stay in the village or to return after they graduate from college. Elderly members of the community often help with their children’s online businesses, leading to a richer labor force and feelings of self-worth.

In a country where the state wields immense power, government’s non-intervention can provide autonomy to the market, which is necessary for a sector to thrive.

“There was even a drop in how frequently villagers wrangle over trivial matters,” a village cadre told me. “As everyone is busy with e-commerce now, even neighbors don’t necessarily have time to visit each other.”

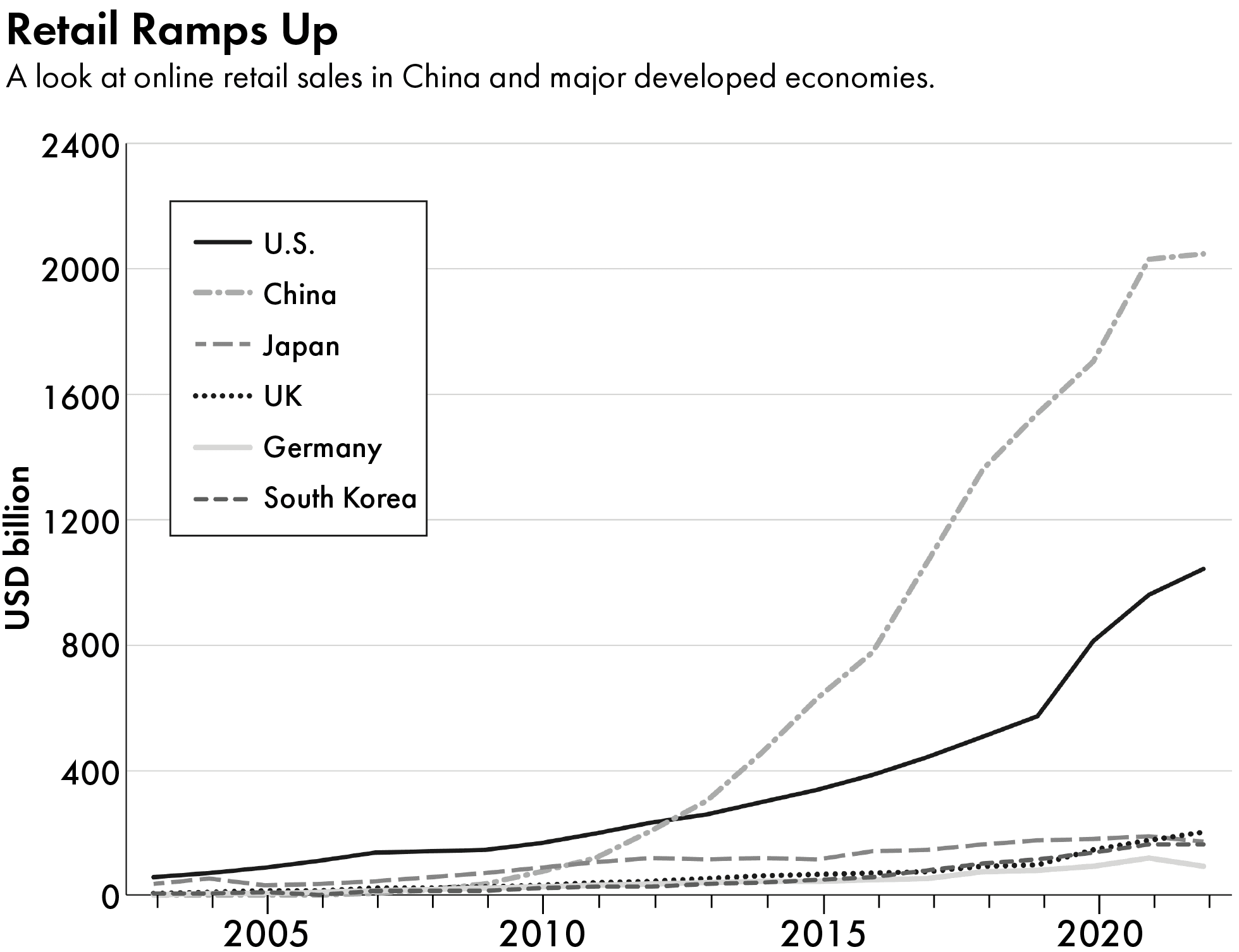

Dongfeng was not alone, of course. China’s e-commerce market has grown exponentially in the past 20 years. In 2003, China’s online retail sales amounted to roughly half a billion U.S. dollars. By 2020, that number was $2 trillion, about double online retail sales in America.

Data: Nominal online retail sales collected by the author from various official sources and converted into USD using yearly average currency exchange rates provided by OECD. Note: In the case of Japan, only business-to-consumer (B2C) e-commerce data is included, as consumer-to-consumer (C2C) e-commerce data is unavailable for many years.

To understand how China achieved such a high level of e-commerce development, I went to Dongfeng Village with a series of research questions in mind. My initial focus revolved around how local governments may have helped to foster the e-commerce industry. The Chinese government, after all, is known for its extensive use of industrial policies, including subsidies and tax breaks to support various industries.

Yet, after my fieldwork in Dongfeng Village and in other locations throughout China, I realized that local governments played a much less significant role in e-commerce than I had anticipated. Although local governments engaged in various collaborations with e-commerce platforms, they appeared to have limited interactions with online merchants operating on these platforms. Many e-commerce merchants I met chose not to register officially with the local government and expressed disinterest in receiving any government support. One merchant even strongly asserted, “No regulation is the best support (不管就是最大的扶持).”

Indeed, even when government subsidies were offered to online merchants, few applied. According to two industry experts, in 2013, a district in Suzhou City allocated 20 million RMB to support e-commerce, but only 15 percent of it was utilized. Similarly, in Shanxi Province, 10 million RMB remained unused and had to be returned to the government. The tepid response from online merchants stemmed from their deliberate avoidance of interactions with the government, fearing tax obligations and potential expropriation. Additionally, many merchants did not need subsidies because of sufficient cash flow from e-commerce.

To be sure, local governments were not irrelevant to China’s e-commerce boom. They provided the necessary infrastructure for e-commerce to thrive, from internet connectivity to roads. Their endorsement of e-commerce also lent credibility to the industry in the eyes of citizens. However, given e-commerce’s prominent status and the government’s history of active intervention in the economy, the level of government involvement seemed intriguingly limited.

In fact, the organic emergence of “e-commerce villages” like Dongfeng seemed to even frustrate local governments who lacked detailed information about the online stores operating in their areas and the sales data of online merchants. In one instance, a local official asked an Alibaba employee, who was traveling with several researchers (including myself), if the platform could share user-level information with the local government. The employee declined.

As we became more acquainted, the local official openly shared her perspective:

“E-commerce makes Alibaba and peasants rich, but the local government gets nothing,” she said. “The [local] government loses. While the e-commerce industry makes our locality nationally well known, our government does not benefit financially. The merchants do not pay taxes, and the logistics companies located in our village only pay taxes in Shanghai, where their headquarters are located . . . I envy those online merchants. Before, being a local cadre at least brought some sense of status. Now, seeing all the peasants making a big fortune and my own monthly salary lower than 3,000 RMB, I even thought about resigning.”

As my research and fieldwork progressed, I switched my research focus from “how local governments supported online merchants to succeed” to “how online merchants achieved their success without substantial government support.” This shift in perspective allowed all the disparate pieces to come together into a coherent narrative, and it highlighted an underappreciated factor underlying China’s extraordinary economic development.

The prevailing explanations for China’s economic growth often rest on the “developmental state” thesis, which emphasizes the government’s pivotal role in the economy. Policies such as tax breaks, state-led infrastructure projects, and subsidies are frequently cited as drivers of growth. This narrative focuses on the government’s visible actions to support the economy — what it has been actively doing.

However, statements like “no regulation is the best support” reveal another important dimension: the art of non-doing. In a country where the state wields immense power, government’s non-intervention can provide autonomy to the market, which is necessary for a sector to thrive. In the case of e-commerce, it seems that the government’s non-doing — rather than its active doing — has been even more pivotal to the sector’s success.

How did David defeat Goliath? A remark by Jack Ma provides the answer: “eBay may be a shark in the ocean, but I am a crocodile in the Yangtze River. If we fight in the ocean, we lose — but if we fight in the river, we win.”

But if the government is not the primary source of support for individual e-commerce sellers, then who is? The answer lies in the e-commerce platforms. These digital platforms are not merely intermediaries connecting buyers and sellers; they act as private providers of market institutions that foster trust. To understand why trust is crucial and how platform-based institutions drive growth, we must revisit the historical battle between the global giant eBay and the indigenous challenger, Alibaba’s Taobao.

Shark vs. Crocodile

In 2003, all the stars seemed to align for eBay to build an e-commerce empire in China. Through the acquisition of EachNet, the nation’s leading online auction platform, eBay swiftly claimed a commanding 85 percent market share. For Meg Whitman, eBay’s CEO at the time, China was a “must-win” to achieve global dominance. In the ensuing years, eBay forged exclusive partnerships with major web portals to thwart competitors’ advertisements and committed substantial investments to signal “an unmistakable commitment and an unstoppable determination to be number one in China.”

Nevertheless, eBay’s remarkable momentum was disrupted by an unexpected contender: Alibaba. Alibaba was founded in 1999 by former English teacher Jack Ma. The company initially only had online business-to-business (B2B) wholesale platforms, facilitating Chinese small- and medium-sized enterprises to sell worldwide. As eBay entered China, however, Alibaba swiftly sensed that eBay would encroach on Alibaba’s user base, since Chinese buyers would struggle to distinguish small business sellers on Alibaba from individual vendors on eBay. Therefore, in 2003, Alibaba unveiled Taobao.com, a rival consumer-to-consumer (C2C) platform, as a defensive move against eBay.

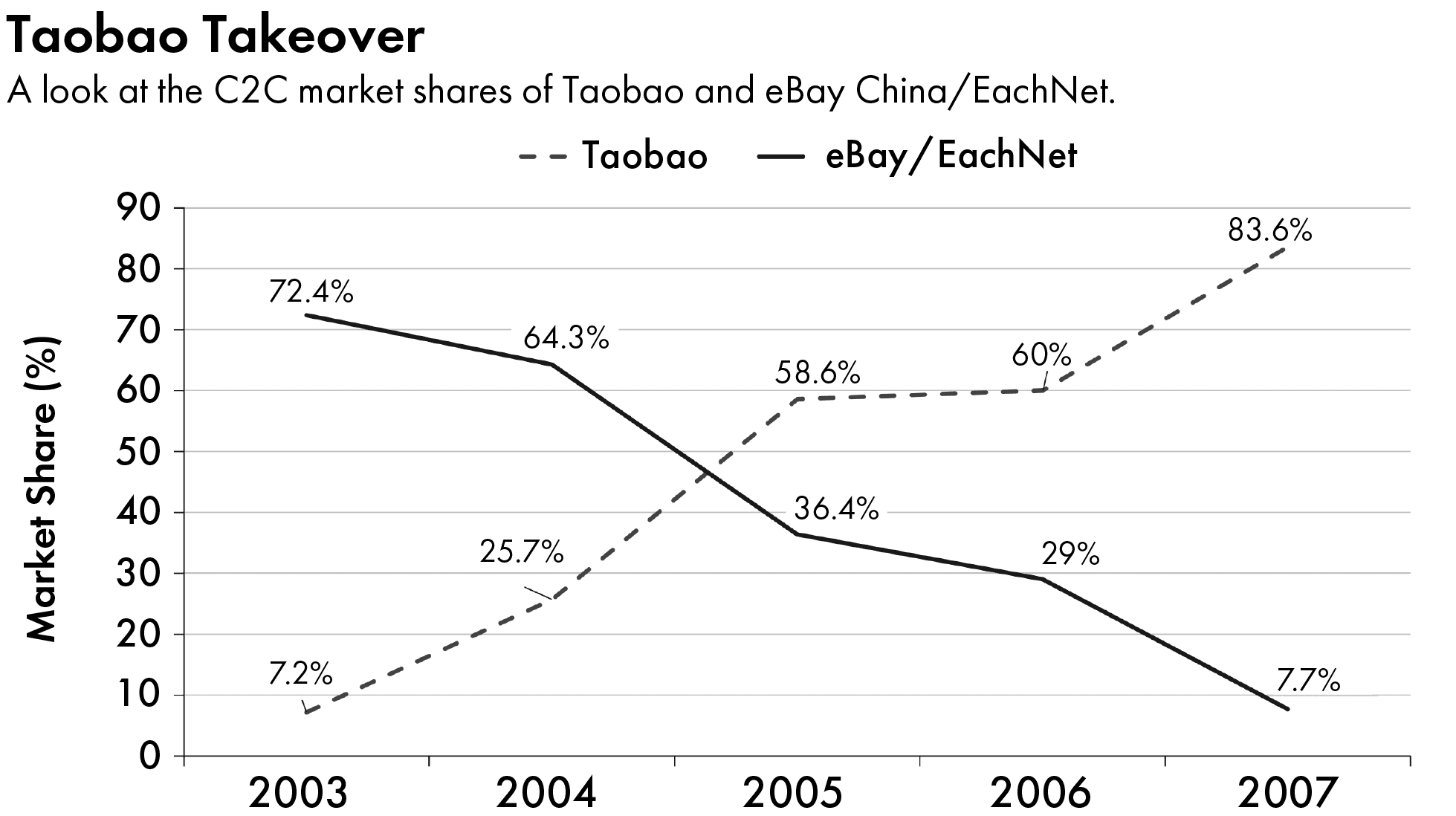

All signs indicated a clear victory for eBay over Taobao. By 2003, eBay was globally recognized, with annual net revenues exceeding a billion dollars. Its first-mover advantage and strong network effects made it appear unbeatable. In contrast, Alibaba was relatively unknown and had only achieved positive cash flow the previous year.

But the battle yielded a surprising outcome. In merely four years, eBay/EachNet’s market share plummeted from 72.4 percent in late 2003 to a mere 7.7 percent in 2007, while Taobao’s surged from 7.2 percent to over 80 percent. This dismal performance prompted eBay to withdraw from China.

How did David defeat Goliath? A remark by Jack Ma provides the answer: “eBay may be a shark in the ocean, but I am a crocodile in the Yangtze River. If we fight in the ocean, we lose — but if we fight in the river, we win.”

A key distinction between the “ocean” and the “river” is their institutional environments. Unlike developed markets, early 2000s China faced institutional voids — an absence or inadequacy of institutions like a strong legal system, efficient arbitration mechanisms, and credit card systems. These institutions are crucial for preventing issues in e-commerce. For example, a strong legal system would reduce counterfeit products, and credit cards protect consumers against online scams. In the U.S., for instance, there was reasonable assurance and trust that if you placed a bid, you would pay and the seller would ship the item. Such assurance was sorely lacking in China at the time.

Coverage of “taobao villages” across rural China, November 22, 2013. Credit: CGTN

As a result, Chinese consumers exhibited notably lower trust in e-commerce compared to Americans. To encourage adoption, China-based platforms needed stronger online institutions to build trust. eBay overlooked this difference and merely transplanted their U.S. model to China, failing to assure Chinese consumers of transaction safety. In contrast, as a local company, Taobao leveraged its deep understanding of the Chinese market and built institutions that fostered user trust.

The Game Changer: Alipay

A critical institution behind Taobao’s triumph is the invention of Alipay. This seemingly small step in improving the online payment systems resulted in a great leap for Alibaba’s e-commerce business.

In the early stages after Taobao’s launch, employees noticed a peculiar trend: Although users were enthusiastic about online trading, they rarely completed transactions on the platform. This was due to a simple dilemma: should the seller ship the products first, or should the buyer pay first? Neither party wanted to kickstart the process, fearing that the other might not fulfill their contractual obligations afterward.

Consequently, most early transactions on Taobao were only partially online. Users would identify trading partners online but meet in person to exchange products and cash, limiting e-commerce to local trades where in-person exchanges were feasible. Fundamentally, this problem stemmed from the aforementioned institutional voids: Without strong institutions to ensure the fulfillment of contractual obligations, trust levels were low, causing trade to stagnate.

After numerous attempts to solve the trust problem, Taobao introduced Alipay. As acknowledged by the chief strategy officer of Ant Financial (Alibaba’s financial subsidiary), “If there were no Alipay, there would be no today’s Alibaba.”

Particularly when dealing with new industries (such as e-commerce, fintech, ride sharing and other parts of the digital economy), the Chinese government often follows a principle of “development first, regulation later” (先发展, 再监管).

On the surface, Alipay might seem like just another online payment system, similar to PayPal. However, what distinguishes Alipay is its integration of a mandatory escrow system (担保支付) into the online payment process.

Alipay is vital in building user trust. Unlike PayPal or credit cards, where the buyer’s payment is directly transferred to the seller upon order placement, Alipay’s escrow service ensures that the payment is released to the seller only after the buyer receives the product and is satisfied with it. If either party is unsatisfied with the transaction, Alipay freezes the payment, prompting dispute resolution. By withholding payment until both parties are satisfied, the escrow system ensures both sides fulfill their contractual obligations.

While Alipay involved little new technology, it was a major institutional innovation that triggered substantial growth in online transactions. In particular, it unleashed the potential of long-distance trade, as individuals no longer needed to meet in person to establish trust. Alipay’s first transaction took place in October 2003 and enabled the international sale of a secondhand camera between Xi’an, China, and Yokohama, Japan.

By early 2004, 70 percent of Taobao products included Alipay as one of the payment options. Taobao later made Alipay compulsory for all transactions.

By contrast, eBay China failed to prioritize trust as a central element of its institutional design until it was too late. The Chinese company that eBay acquired, EachNet, recognized the importance of trust and even introduced a beta version of an escrow service prior to Alipay. Unfortunately, this crucial advancement was halted to make room for the introduction of PayPal in China. A year after Alipay was created, eBay China finally launched its own payment escrow system, called “An Fu Tong” (安付通). This endeavor proved unsuccessful, as users often confused An Fu Tong with PayPal, exacerbating eBay’s challenges.

The Political Backdrop

Apart from Alipay, one crucial factor behind Taobao’s success is often overlooked: the Chinese government’s tolerance to Alibaba’s institutional innovations in legally ambiguous domains. At the time of Alipay’s inception, China’s financial industry was predominantly controlled by state-owned banks. Non-bank third-party payment systems, including Alipay, lacked the legal authorization to issue direct online payments. The legal risks associated with launching Alipay were so substantial that Jack Ma had to reassure his staff by saying, “If someone needs to go to jail for Alipay, let it be me.”

The government was informed about Alipay from the outset, since Alibaba decided to provide monthly updates to alleviate suspicions. However, for nearly eight years, the government maintained a regulatory-free environment in this specific domain rather than cracking down on it. Eventually, in 2010, the central bank legitimized third-party payment systems, and, a year later, the government issued the first electronic payment licenses to 27 domestic enterprises, including Alipay and Tencent’s Tenpay.

Not only did the government acquiesce, but in the mid-2010s, it actively encouraged the disruptive innovations introduced by Alipay and other private payment platforms, disregarding pleas from state-owned businesses to ban these platforms. A notable example is the launch of a money market fund called “Yu’E Bao” (余额宝, meaning “leftover treasure”) by Alipay in 2013. This offering allowed consumers to earn much higher interest rates by keeping their funds within Alipay, resulting in a rapid diversion of deposits away from state-owned banks. Despite strong complaints from state-owned banks, China’s central bank chief sided with the private sector, claiming that Yu’E Bao and similar products would definitely not be banned. On another occasion, then-Premier Li Keqiang even praised these fintech innovations as a means to reform the Chinese economy, incentivizing the mighty state-owned banks to change.

Over the years, as Alipay became widely adopted and an integral part of the country’s digital infrastructure, the Chinese government partnered with it to strengthen legal enforcement. In 2018, it took only 40 minutes for two courts in Beijing and Hangzhou to coordinate and investigate a suspect’s Alipay record. In 2022, the Public Security Bureau of Chaoyang District in Beijing also collaborated with Alipay to jointly develop an Anti-Fraud Early Warning System, targeting scammers.

The ‘Anti-Fraud Early Warning System’ developed by the Public Security Bureau of Chaoyang District and Alipay, as seen in Alipay’s mobile app. Source: Chaoyang Municipal Public Security Bureau via WeChat

It may seem paradoxical that an authoritarian government, possessing significant regulatory capabilities, would allow private firms to flout rules and even challenge the business interests of the state-owned sector. In fact, it points to a broader governmental strategy that I call strategic nonregulation. This nonregulation does not come from an inability to rule; rather, it is a deliberate choice by the government to refrain from stringent regulation, thereby creating space for market development and innovation.

Particularly when dealing with new industries (such as e-commerce, fintech, ride sharing and other parts of the digital economy), the Chinese government often follows a principle of “development first, regulation later” (先发展, 再监管). It adopts a “wait and see” stance and regulates only when the time is ripe. In the case of e-commerce, the Chinese government waited nearly two decades before implementing stricter regulations in late 2020. This delay allowed ample time for private digital institutions like Alipay to emerge and fill the governance gap left by the state.

Ultimately, the combination of platforms’ private provision of key market institutions and the government’s strategic nonregulation was instrumental in driving China’s e-commerce boom. By outsourcing the tasks of institutional building and enforcement to platforms — a process I term institutional outsourcing — the state facilitated rapid growth without undergoing the arduous process of establishing these institutions itself.

Excerpted from FROM CLICK TO BOOM by Lizhi Liu. Copyright © 2024 by Princeton University Press. Reprinted by permission.

Lizhi Liu is assistant professor at the McDonough School of Business at Georgetown University, where she is also a faculty affiliate of the Department of Government. Her research specializes in the politics of trade, technology and innovation, and the political economy of China.