This year, more than ever before, the question of how the U.S. should deal with China is on the ballot. China’s handling of the Covid-19 outbreak represents the culmination of long-building tensions between the two countries over national security, global leadership and, perhaps most pressingly for American voters, the economy.

The past year has brought an escalating U.S.-China trade war, the Trump administration’s move to decouple from Chinese technology companies like TikTok and Wechat, and an ever-expanding Entity List filled with Chinese firms. Not only have these conflicts soured Sino-American diplomacy, they have also impacted American consumers, manufacturers, and investors. How the next American president, whoever he may be, handles this critical turning point will set the tone for U.S.-China relations in the twenty-first century.

In this week’s issue, The Wire has identified the three most pressing areas in the U.S.-China economic relationship: trade, technology, and investment. These three policy spheres are both rife with disagreement and rapidly evolving, which can make it difficult to find one’s footing. To help, we have briefly summarized the current state of affairs and then asked leading policy makers, cyber security experts, senators, economists, and investors what the U.S. policy in each of these areas should be going forward. What follows are their recommendations for how the next president should strengthen the American economy, retool the country’s trade policy, and spur technological innovation — all while minimizing conflict with China.

TECHNOLOGY

The Trump administration has used just about every tool in its shed to try and kneecap China’s technological rise. In 2018, it launched a campaign to rid the U.S. network of components from Huawei and ZTE, the Chinese telecom equipment giants, citing national security concerns. Meanwhile, pointing to work with the People’s Liberation Army or involvement in the mass internment of Uighurs in Xinjiang, the administration also started adding a range of Chinese technology companies, including those in advanced fields like artificial intelligence and those with U.S. investors, to the U.S. Entity List, which makes it harder for those companies to do business with Americans. The Committee on Foreign Investment in the United States, an interagency group led by the Treasury Department, has also blocked Chinese investment in financial services, dating apps, and hotel management software, because it says Chinese businesses should not have access to the personal data of Americans — a line of argument repeated recently as the Trump administration made moves to ban social media apps TikTok and WeChat from U.S. devices.

The Trump administration has also restricted visas to Chinese nationals who want to study STEM subjects in the United States. And the Federal Bureau of Investigation has ramped up arrests of Chinese students and researchers it suspects of being spies.

The Trump administration’s tools have been blunt, at times wreaking havoc in markets, creating uncertainty for businesses, and spelling doom for those who fall in the crosshairs. But, still, there is a growing consensus that both the advancements in Chinese technology and its ubiquity present threats to the United States. The next president will have to decide which tools are worth using.

How should the next president respond to China’s state-backed push to lead the world in high-tech fields?

Anja Manuel

Anja Manuel is co-founder and partner in Rice, Hadley, Gates & Manuel LLC and Director of the Aspen Strategy Group and Aspen Security Forum. She is a former State Department official.

If you look across history, the countries with the best technology always went on to have empires. The United States has been the dominant technology power for the past five or six decades. But now, we need positive strategies to build ourselves up.

“It’s not that China has caught up in many advanced technologies yet, but it’s like that sign in your rear view mirror: ‘Objects may be closer than they appear.’ That’s where China is today. There are five areas that I think we need to be watching carefully: fintech, AI, semiconductors, quantum, and different aspects of biotechnology, especially the ones that can bleed into biological weapons.

In payment systems and fintech, with what Alipay is doing, I would argue China is well ahead of the U.S. and Europe. And if the West doesn’t wake up on this issue, we’re going to have another 5G situation on our hands. In artificial intelligence, many of the best academics are in the U.S., Canada, and the UK. But the tinkering, and the application of, AI is increasing very rapidly and very impressively in China. In semiconductors, the Chinese are still behind. But, they’ve put $100 billion or more into catching up. And quantum isn’t quite there yet. But in five years, we’ll be wanting to make sure that we’re in the lead.

The Trump administration’s actions have been almost all defensive: trying to build a big moat around our technology. They’ve tried to stop China from buying American companies, and they instituted really stringent export controls. The Department of Commerce is coming out with more and more regulations saying, basically, you cannot sell any semiconductors that are either designed or created in the U.S. to Huawei and others. It’s been all restrict, restrict, restrict. Some tightening, of course, was necessary. But why are we concentrating only on tearing China down?

Credit: Briáxis F. Mendes (孟必思), Creative Commons

There are a number of ways that we can build ourselves up. On semiconductors, we need to make sure that the U.S. continues to lead in chip design and that the most advanced fabs, which are the factories that create semiconductors, are located in the United States or allied countries. TSMC is probably the most advanced, and they are in Taiwan. Due to some good work by the Trump administration, one TSMC fab is now moving to Arizona, but it’s not the most advanced one. This is an area where we need a positive, affirmative strategy.

We need a new policy on science and technology education. If you talk to our university presidents, they’ll tell you that we can’t fill our STEM PhD programs with American students alone. So we’ve got to do more at the K-12 level to get our STEM pipeline up and running. We could have a relatively inexpensive program like what President Eisenhower did after Sputnik that offers financial incentives for Americans who study the disciplines that we really care about.

Another important area is our basic science. Research and development [R&D] budgets funded by the federal government have gone down pretty precipitously under the Trump administration. The private sector is picking up the slack, but not necessarily for the technology that makes us most competitive, or that will help our military. At the height of the Cold War, our R&D spending was 2 percent of our GDP — a huge amount! Right, now we’re down to 0.7 percent of GDP. If we can raise it up to 1 percent — that’s about the historical average — then we will really see the advances we need to stay relevant.

Finally, so far we’ve been doing all of this alone. Export controls are worth very little if it’s America only. I and others have suggested creating a Technology 10: a loose grouping of countries that have the same view about technology that we do. So, for example, in a working group on semiconductors, you’d probably have the U.S., the Netherlands, Japan, South Korea, and maybe Taiwan. You could have a different one on AI ethical standard, which might include the UK, Australia, and India. We need a group of countries that share our values and that work together on making sure that the U.S. and our friends remain in the technological lead.”

James Lewis

James Lewis is senior vice president and director of the Technology Policy Program at the Center for Strategic and International Studies (CSIS). He is an expert on cybersecurity and the geopolitics of technology. Prior to joining CSIS, he worked at the Department of State and Department of Commerce in various diplomatic assignments.

The next president needs to continue to push on China. But it’s not a Cold War. We’re not going to get containment or an embargo on China. The next president has to do something a little more nuanced.

“There’s strong consensus on the Hill, and in the American public, that we need to push back on China. China’s behavior isn’t going to change. Xi can’t afford to change. So that means if the next president changes from the current course, there will be repercussions on the Hill and in the country. We will need to still push back on China.

But that doesn’t mean our policy couldn’t be better managed. The biggest change the next president needs to make is to develop an alliance strategy for getting China to change its behavior. We need to work with our allies and partners. The goal here is to get reciprocity from China on how companies are treated and backing off on espionage. That will be a lot easier if we have the Germans, the Japanese, the Canadians, Brussels, and others on board.

Credit: Cherie Cullen, U.S. Department of Defense

Then we have to identify and distinguish where we are facing shortfalls versus where we are facing competitive obstacles. In terms of shortfalls, there are some obvious answers. We’re falling short in R&D investment. We’re falling short in science and engineering and math education. Those cry out for federal programs and for restoring funding for American programs. It also calls for immigration reform. Twenty years ago, the head of IBM told me that every PhD we give in physics, math or engineering should come with a green card stapled to it. That’s still true. But we haven’t been able to deliver. Give people the opportunity to live in the United States. Maybe we’ll have to do a little more on the counter-espionage side to make sure they aren’t calling home. But most tech companies say they’d rather manage and accept the risk themselves. Let the foreign workforce in.

In terms of where we’re facing competitive obstacles, chipmaking is the prime example. And it’s not just that China is making a big push to foster chipmaking, but that about a dozen other countries are also trying to incentivize it. So, when a chip company goes to locate, countries are going to them and saying: ‘if you locate here, we will give you a tax break, and we will give you free land.’

We can’t be afraid to spend money. This is China’s biggest advantage right now, but ever since the Cold War, we’ve been reluctant to spend. Now that we’re in another fight, we’re going to have to. People may not like it, but in any conflict, both sides get a vote, and the other guys have voted to spend money. If we don’t match them, we’ll lose.

But while there’s a very good case to be made for matching foreign incentives and emphasizing R&D, we can’t just have an old-style industrial policy. The next president should be a little cautious about being overly deterministic and having Washington lay out the strategy for what the tech industry needs to do. We didn’t have a strategy for the internet, after all, and that worked out pretty well.”

Senator Mark Warner

Mark Warner is a Democratic Senator from Virginia. He is the Vice Chairman of the Senate Intelligence Committee. He also served as the Governor of Virginia from 2002–2006. Prior to his time in government, he was a technology investor, and co-founded the company that became Nextel, a wireless service operator.

The two prevailing technology governance regimes are an authoritarian model developed by China and Russia, and a laissez faire model, driven by two-decades of U.S. policy that eschewed rules for the internet. That’s just not viable anymore. We need to work with our allies to develop governance regimes that reflect and advance democratic values and priorities.

“Over the last several years, the Senate Intelligence Committee has, on a bipartisan basis, focused on supply chain security and the threat posed by state-directed companies like Huawei. In reality, this extends beyond Huawei: any software that’s from a vendor located in a country that has laws that make its technology sector ultimately beholden to the state apparatus is potentially suspect. And that’s not necessarily because it currently has some hidden backdoor in it. It’s because companies in these countries can serve as extensions of government power and can be compelled to comply with data requests from the state. Which means that in the future they can leverage that access for surveillance or sabotage or to sow disinformation or chaos.

This isn’t just about keeping Huawei out of our networks though. If Huawei’s market share continues to grow, it will jeopardize the stability of the Western alternatives that remain. A key part of dealing with these strategic challenges is re-prioritizing foundational technologies like communications infrastructure and semiconductors to maintain not just our country’s economic leadership, but to ensure that countries with inconsistent values and objectives – whether that’s around due process, intellectual property protection, state surveillance, or censorship – aren’t able to leverage control over these foundational technologies in worrisome ways.

Unfortunately, many of the key ingredients to our success — federal support for R&D, investment in basic research, and support for advanced manufacturing — have declined over the last 20 years. It wasn’t so long ago that ‘industrial policy’ was a dirty word. To be clear, I am still a firm believer in the power of open markets and I’m opposed to governments picking national champions or micromanaging technology development. We can and should still be working to ensure that the conditions and policies favor new entrants, open innovation, and technology neutrality.

But, that said, we have to be pragmatic and honest about the role of the U.S. government when it comes to establishing and maintaining those conditions: they don’t just happen automatically. Look back to 1979, when the U.S. government invested $4.2 billion to create the GPS system, which is such a large part of today’s digital economy. In 2020 dollars, that equates to $15 billion! Our recent antipathy towards ‘industrial policy’ and unwillingness to honestly reckon with the government’s role in facilitating innovation in the past has made us unwilling to commit to similarly ambitious investments today.

The Trump administration has taken the worst possible approach: spurning overtures from our allies for a democratic vision of internet and technology governance, while embracing a non-transparent approach that validates digital protectionism abroad to the detriment of U.S. technology companies. This isn’t viable anymore. The U.S. should be offering a values-based alternative to China’s cyber sovereignty — one that promotes a multilateral approach and embraces pragmatic governance regimes. In areas like AI, in particular, we need to work with our allies to develop rules that reflect and advance democratic priorities. Concerns about China are bipartisan, and the next president should keep the pressure on Beijing while also ensuring we make the right investments domestically to outcompete those who want to indigenize technology.”

INVESTMENTS

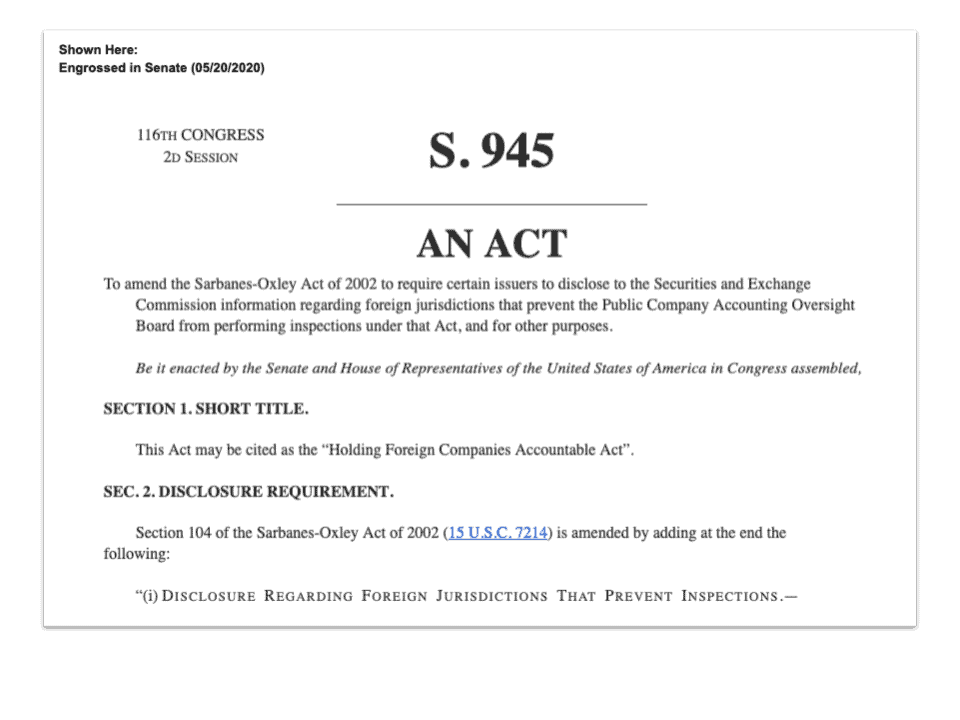

The Trump administration has recently turned its attention towards paring back U.S. involvement in Chinese capital markets. In May, the administration blocked a federal pension plan from investing in Chinese companies traded on mainland exchanges and has urged universities to clean their endowments of China. Despite these moves, billions of dollars from U.S. investors have flowed into Chinese equities in the past few years.

On the flip side, when a Chinese startup listed on Nasdaq collapsed after admitting fraud in April, there was fresh scrutiny of Chinese companies traded in the United States. Chinese companies often offer fewer disclosures, and in May, a bipartisan group of senators introduced a bill that would force Chinese companies to delist from U.S. exchanges if China doesn’t allow U.S. regulators more access to their books. Some Chinese companies appear to be preparing to leave the U.S. if things get uglier. Chinese investment in any area involving technology, the military, or data could face immense hurdles to get approved by U.S. regulators.

The Trump administration’s moves have been seen by many as a necessary first step towards reducing vulnerability to China. But when it comes to investments and capital markets, the U.S. may not have as much leverage as it would like, and if the next administration pursues decoupling from China without being careful, the American people could very well be the biggest losers.

How should the next president approach capital flows between the U.S. and China?

Huang Yasheng

Huang Yasheng teaches at MIT’s Sloan School of Management. He runs the school’s China Lab and India Lab and is the author of Capitalism with Chinese Characteristics, a study of the economic reform era. Huang has a PhD from Harvard and previously taught at the Harvard Business School.

The thing I worry about is this tendency to think up all the things you can do to hurt China. I don’t think that’s a very productive way to do things, even if I fully acknowledge that China has done many things wrong.

“I don’t think inflicting harm on China should be an end in and of itself. The next president needs to first say what our policy objective is and then think about the right policy instrument to achieve it. What we’re seeing now is just going after China — one thing after the other, with delistings and CFIUS reviews. If you think, for example, that intellectual property rights [IPR] is problematic, why is restricting Chinese investments in the United States consistent with that particular objective? They’re not violating IPR when they invest in the United States; they’re paying a market price.

I hope the next administration will be more clear headed. They should recognize the areas where the two countries have conflicts, and the areas where the two countries can cooperate. China has the second largest GDP in the world. It still has incredible production capacity and controls vital things that the rest of the world needs. And, you know, there’s 1.4 billion people there and their welfare is also important. If you just blacklist China altogether, that’s not really a starting point.

Credit: Alibaba

Rather than just threatening to delist Chinese companies, for example, the next president should impose a timetable, which would allow them to get their act together and improve disclosure. Because you are trying to protect U.S. shareholders, and it is absolutely true that Chinese companies are not transparent — there are all sorts of Ponzi schemes and ownership structures that are not clear. But even though there are some Chinese companies that have decided to delist from the U.S. capital markets, the New York Stock Exchange and Nasdaq still have a lot of allure. If you’re a technology company and you’re not listed on Nasdaq, you just don’t have the same cache. It’s not the same to be on a Chinese exchange. So with this leverage, the U.S. could impose a timetable. I can even imagine coming up with fairly China-specific provisions, taking into account the unique and peculiar features of the Chinese system. Chinese companies would have to satisfy these additional provisions, and if they don’t, then you can delist them.

It should be a similar approach with Chinese investments in the United States. There isn’t a strong rationale to restrict Chinese investments, because they have to do everything in compliance with U.S. law and regulations. And they pay full market price. But if technology export is your concern, then the U.S. should write additional clauses about the use of the technology and the control of the technology. The next administration can be proactive and innovative about imposing additional hurdles, rather than just banning Chinese investments in the United States.

China warrants additional brainstorming. It requires some big ideas and doing things a bit different from the usual way. Instead of telling TikTok to sell their business, for instance, the U.S. should see it as an opportunity to tell the Chinese to let Google or Facebook in. There needs to be a new normal now.”

Weijian Shan

Weijian Shan is the chairman and chief executive of PAG, the Hong Kong based private equity firm. Previously, he served as senior partner at TPG Capital, an American investment firm, and JP Morgan’s China chief representative. He has taught at University of Pennsylvania’s Wharton School and founded the China Economic Review.

Unpredictability is costly, disruptive and hard to deal with — leading to reduced economic activities and huge wastes.

“When it comes to Chinese companies listing on U.S. exchanges, the proposed tightening of regulatory requirements, especially with regard to disclosures and compliance with accounting standards, is good for investors as well as listed companies. Transparency and compliance requirements don’t drive good companies away, but the threat to delist Chinese companies for political reasons does.

From an investor’s point of view, the world has an oversupply of capital but a dearth of good investment opportunities. Restricting capital flow just punishes the investor. Unless sanctions are imposed, depriving Americans of the right to invest in certain places infringes upon their property rights, which is probably unconstitutional. And it won’t make a dent in the ability of Chinese companies to raise capital, as American investments in China (about $100 billion a year) represent less than 2 percent of China’s total investment (about $6 trillion a year).

And in terms of sanctions, the next president needs to understand that simply increasing the number of companies on the U.S. Entity List can have an effect on the sanctioned companies — but having an effect doesn’t mean it is effective to achieve policy objectives. In the long run, overusing such sanctions simply incentivizes China to build its own technologies. And China has reached the stage of economic development where it will be able to reinvent the wheel — any wheel — in time. The next administration should focus on building America’s technological leadership, as opposed to taking down China, which is counterproductive.”

Lawrence Summers

Lawrence Summers is the former Director of the National Economic Council for the Obama administration and former Secretary of the U.S. Treasury for the Clinton administration. He has also served as Vice President of development economics and chief economist of the World Bank. Currently, he is the Charles W. Eliot University Professor and President Emeritus at Harvard University

Actions create their own facts on the ground, and even actions that were unwise 30 months ago may not be wise to reverse today.

“When it comes to investments and capital flows, U.S. policies need to be done in much more nuanced ways rather than with hard and fast blanket principles. In general, for example, it’s better for American capital to be in Chinese companies than it is to be outside those companies. In a world where capital is widely available from many sources, our capacity to damage Chinese companies by being unwilling to give them capital is rather limited. We are doing more damage to ourselves than we are to Chinese interests when we deny Americans the opportunity to invest in Chinese companies. And if Americans judge that it’s in their economic interest to be minority shareholders in Chinese companies, I don’t think our government has a basis for correcting that judgement.

But when it comes to Chinese companies listing in the U.S., my hope would be that, over time, we would apply standards like the standards we apply to companies from other countries. That means some combination of insisting on the transparency that goes with the rules of our stock market and showing the degree of respect for national jurisdictions that we display vis-a-vis other countries. I don’t think there’s strong case for treating China in an especially generous way because they’ve got large companies that are attractive to our exchanges, nor do I think there’s a case for treating China in an especially punitive way.

The next administration should be very cautious about co-mingling the economic and the political. For example, economic sanctions, particularly when they are unilateral in their orientation, are a shoot-yourself-in-the-foot policy. The next president needs to be careful about who we’re helping and who we’re hurting when we use economic sanctions.

We also need to think carefully about where our red lines are when it comes to China. The next administration needs to more explicitly set America’s top priorities and pursue them in the firmest possible way. Our errors in the last several years have certainly not been of insufficient truculence. But I think the next president is going to need to take an increasingly firm approach to China, and take a firm approach that is focused rather than indiscriminately angry and dissatisfied.”

Willy Shih

Willy C. Shih, a professor of management practice at Harvard Business School, likes to talk about solutions. He is an expert in manufacturing, supply chains and intellectual property rights. He serves on the board of Flex, one of the world’s biggest contract manufacturers. He previously worked at Silicon Graphics and Eastman Kodak.

The important thing is to have a set of rules, to apply them consistently and enforce them consistently, because businesses like predictability. Businesses don’t like you changing the rules — especially arbitrarily or seemingly arbitrarily.

“Consistency is the foundation of fairness. And, as Americans, we should all believe in fairness. But right now, I don’t think anyone knows what the expectations are anymore. The U.S. Commerce Department is rolling out new additions to the Entity List practically every month. This can be damaging to American suppliers, and we don’t want American suppliers to be subject to political whims. That’s very destructive. My concern is that the path we’re taking is alienating China from using the U.S. as a supplier. If you were the Chinese government, would you trust the U.S. for anything? Or would you be looking for substitutes? That’s a bad position for U.S. companies to be in.

I would prefer to see the next administration working with U.S. allies, which gives us enormous strength. If multiple countries take a unified position, we’d be a lot more likely to effect change and there would be some consistency in behavior. The problem is, there’s been a lot of damage done not only in the U.S.-China relationship, but also the U.S. relationships with many others. The next president needs to rebuild alliances. It’s going to take time — probably more than the next term or even the next two terms — but we need to rebuild America’s commercial leadership and create a cooperative vision that recognizes that China has a different system.

The other thing I would tell the next president is that while I understand why you do not want sensitive technologies to fall into the hands of strategic competitors, you can’t think America can do everything at home. There’s a big uproar about semiconductors right now, for example, and there’s a big uproar about a lot of so-called strategic commodities like rare earth minerals. But if you think the U.S. can do, say, semiconductors all by ourselves, we’re a long way from that. It will surprise a lot of people to learn how dependent we are on other parts of the world for these industries, including China, Germany, Italy, Switzerland, Mexico, Canada, Latin America, and various nations in Africa. A lot of people don’t appreciate how complex the interdependencies in the world are; and it would be naive for the next president to think we in the U.S. can do it all ourselves. Those days are gone.”

TRADE

The trade war between the U.S. and China started in 2018, when the Trump administration implemented tariffs on various Chinese goods, citing the country’s trade practices, limited market access, intellectual property theft, and the American goal of bringing manufacturing back home. These initial tariffs resulted in an escalating tit-for-tat, hundreds of billions of tariffs from both sides, and wide-ranging economic impacts on everyone from American soybean farmers to Chinese shoe factory workers.

Subsequently, Chinese and American negotiators have worked on a series of partial deals to minimize these rippling economic reverberations. The most recent agreement, which was signed in January, included intellectual property theft provisions and a promise from the Chinese to increase purchases of U.S. goods by $200 billion to reduce trade imbalances.

But as we approach November’s election, the future of the U.S.-China trade relationship is still very uncertain. Some American lawmakers, including members of the Trump administration, are calling for a complete economic decoupling from China, an extrication of American supply chains from China, and a doubling down on sanctions, which have already been extensively leveled on Chinese companies for their involvement with human rights abuses in Xinjiang and the Chinese military. Others are calling for a resumption of more standard trade policies, claiming that Trump’s aggressive approach has done nothing to address underlying issues and has only backfired on the American people. The architects of the next administration’s trade policy will be tasked with deciding which path to follow, and that decision will have enormous consequences for the American, Chinese, and global economies.

How should the next president think about U.S.-China trade disputes?

Mary Lovely

Mary Lovely is a senior fellow at the Peterson Institute and a professor of economics at Syracuse University. She was co-editor of the China Economic Review from 2011 to 2015.

Trade policy should be used for creating rules — not for political signaling or for redistribution in the domestic economy.

“U.S. trade policy should be focused on unmet challenges such as digital trade, common rules on data protection and data localization. It should be focused on market opening, particularly in regions like non-China, Asia, where we stand to lose markets because of the newly forming free trade area. We should be using trade policy, trade negotiations, and our diplomatic effort, our market power, and our own soft power toward creating strong institutions and new rules of the road.

To make any progress on these issues, we need to recognize that trade is viewed as having major distributional impacts, and a large part of the U.S. population is now convinced that its overall impact is negative. You hear often about the so-called ‘China shock,’ for example. I don’t think that’s a complete description of what has happened over the last 20 years; a lot of investors benefited from holding tech stocks that did incredibly well because of China’s impact on the cost of devices. But trade policy needs to be undertaken in the context of inequality in the United States. I don’t think that the next President, whoever it is, is going to get any support for designing new rules of the road for trade unless he also discusses distribution. Now, clearly, Trump has emphasized trade’s losers. I just think his policies have created false promises. Reshoring and bringing manufacturing jobs back is not going to happen by levying tariffs, even the 25 percent tariffs he placed on imports from China.

Official White House Photo by Shealah Craighead

Trade policy is being asked to do too much; other domestic policies have to do some of the heavy lifting. Unfortunately, the U.S. has been burying its head in the sand. Just take the auto sector, we know the auto sector is changing. The U.S. is clearly a leader in electric vehicle technology, along with a couple other countries, and yet our trade policy has just doubled down on combustion engines. We need to be at the forefront of developing new machinery. Germany, for example, did incredibly well and ran a trade surplus with China for years by supplying advanced machinery. Government policy can help by preparing the workforce for jobs in high-end manufacturing, not by pretending that we can reshore jobs in labor-intensive sectors.

A policy focus on manufacturing alone is not going to be enough to improve the outlook for American workers. Automation means fewer, more skilled jobs in manufacturing. So we have to think about other ways to create good jobs. And the next president has to see that trade policy is only one set of tools. China has been used as a kind of boogeyman to avoid focusing on what the U.S. needs in terms of domestic reforms. The Biden campaign, for instance, is calling for policies like taxing offshoring, notably call centers. Their concerns are understandable as we have a lot of people underemployed. But there is little attempt to understand why call centers aren’t located here. Or how policies, like ensuring fast broadband throughout this country, can be used to bring tradeable service sector jobs to the United States. You can’t solve these very big problems without thinking beyond trade and tax policies. You have to think about their intersection with other domestic policies.”

Jeff Bader

Ambassador Jeff Bader is a senior fellow at the Brookings Institute. He was President Obama’s principal Asia advisor from 2009 to 2011, and over his three-decade career as a foreign service officer, Bader served in a number of posts covering China. He is a director of the National Committee on U.S.-China Relations.

We’re not in the place we were some years ago. The next administration has to recognize that the China we’re dealing with is a strategic competitor. There is going to be a high degree of friction in the relationship.

“On economics and trade, we need a much more assertive approach to press China to abandon the privileges that it retains from its WTO accession. Although they were not called ‘developing country exceptions,’ at the time, that is what they were. China ought to be compelled by a multilateral coalition of advanced countries to accept that it needs to open its market in precisely the ways that advanced economies have done — that they don’t get any breaks. The only way you do that successfully is with the EU, Japan, Australia, Canada and others, collectively, making the argument and imposing consequences if China doesn’t agree.

Credit: William J. Clinton Presidential Library

But a new administration would also need to demonstrate that they can take yes for an answer. If the Chinese do something that is positive, we should acknowledge that so that we are no longer engaged in this race to the bottom where we try to be just as restrictive as China is — we can’t win that game. There has to be a positive reciprocity cycle rather than negative one. It’s not easy to do that, but the next president needs to understand that this isn’t just a case of ‘let’s shake hands and smile at each other.’ These are issues where we really have to dig in.

After the last few years, Chinese leaders and Chinese society have concluded that the U.S. is irredeemably hostile; that the U.S. opposes their taking their rightful place in the world and that the attacks on the Communist Party are simply a Trojan horse for a larger effort to halt China’s deserved rise. Those are hard perceptions to overcome, and there is a huge risk in them. The next president should commit to accepting that China is a strategic competitor, not an enemy, find areas where we can cooperate, and not look for quick fixes or politically popular gestures.”

Wendy Cutler

Wendy Cutler is vice president of the Asia Society Policy Institute. She served for nearly three decades in the Office of the U.S. Trade Representative, rising to become the Acting Deputy U.S. Trade Representative when the Trans-Pacific Partnership (TPP) agreement was signed.

We’re at the juncture where, in order to be effective, we need to work more closely with allies and partners. We share similar concerns and by working together, we can urge China either not to implement certain problematic policies or urge them to work with us to develop new international trading rules.

“Everyone points to the EU and Japan as our natural allies on these issues, but I think the net can be cast much wider, to include Australia, Korea, Canada, Mexico, certain Southeast Asian countries, and even certain Latin American countries. But, it’s important that we be respectful and realistic in working with them. Because even though some of our concerns and interests overlap, there are also areas where they don’t. For example, we might want to be tougher, or there will be matters where we don’t see things the same way they do — particularly among Asian countries where China for most is their largest trading partner. We need to have realistic expectations about working with allies and partners, but in any overall approach towards China, it’s time for us to put a lot more weight on a collective response.

The next president also needs to develop trusted supply chains, recognizing that there are certain essential and strategic sectors where reshoring may be in our national interest. When it comes to which sectors are prime for reshoring, folks point to medical supplies and medicines, semiconductors, and rare earths. But I’m sure there are other sectors that would fall into this category that we’re not yet thinking of. We need to do a thorough review to identify not just today’s sectors of concern, but also to take a forward-looking approach. We can’t re-shore everything, of course, but we should provide incentives for companies in certain sectors to bring some production back to the United States. And to complement that, we should establish trusted supply chains with like-minded countries, so we’re not relying so much on China or any one source. We need to diversify, and the next president should recognize that trade agreements can play an important role in that process — they can provide the basis for integrated supply chains among allies and partners.

There is no question that we need effective export controls on key products that have national security implications. But, the next administration should work to make sure the list does not get too broad by including products that frankly don’t present genuine national security threats. This is also an area where we need to work with our allies and partners, because if we are too enthusiastic about imposing export controls on a wide range of products, we may see companies from other countries stepping in and displacing U.S. sales. One thing I’ve learned through my years as a trade negotiator is that once you lose market share, it’s extremely difficult to regain it.

Our current trade policy toward China is unfinished work. The current focus on China’s unfair trade practices is welcome and rightly underscores the seriousness of the problem. But while we’ve made some inroads on issues like IPR [intellectual property rights] and technology transfer, we’ve caused disproportionate pain on U.S. interests, whether it be consumers, companies, workers or farmers. The next occupant of the White House, whoever he is, needs to revive the focus on addressing the practices associated with China’s state-led economy, like industrial subsidies and state-owned enterprises, while working with allies and partners in the context of an overall China strategy. China is in it for the long game. We need to be as well.”

William Reinsch

William Reinsch is the Scholl Chair in International Business at the Center for Strategic & International Studies and a senior adviser at Kelley, Drye & Warren. He was the undersecretary of commerce for export administration during the Clinton administration and president of the National Foreign Trade Council for 15 years.

I look at it as running a race. There are only two ways to win: you run faster, or you trip the other guy. A policy that focuses only on tripping is not going to succeed. You want to do that, if you can, but what you really want to do is run faster. And that means out-innovate, out-work, and hustle.

“The things that we’ve complained about — subsidies, intellectual property theft, support for state-owned enterprises, discrimination against Western companies — they’re all serious problems. I wouldn’t make light of them. But for the Chinese, what we’re demanding is not perceived as economic change, but as political change, and they’re not going to agree to that. The next administration should continue to press them on it, because they’re violating international trade rules, but we need to be realistic about the fact that they won’t change. And that means understanding that the real competition with them is not going to be in China, because they’re not going to treat us fairly. And it probably won’t be here, because we don’t need to treat them fairly in response. It’ll be the rest of the world, in third markets. We’re going to go head-to-head with them in India, Latin America, and Africa.

Outside of national security related issues, reshoring our manufacturing will make us less competitive in these contests. Reshoring means telling companies not to do what they’ve found is most efficient, the lowest cost and best quality. So while it might create jobs here in the United States, in the long run, it makes us less competitive globally. But keep in mind that decoupling and reshoring are not the same thing. Companies are going to leave China for lots of reasons, but they won’t come back here. They’re going to go somewhere else that meets their needs. The big winners will probably be Vietnam and Mexico, followed by other Southeast Asian countries and maybe other Central American countries.

Credit: Tracy Robillard, USDA Natural Resources Conservation Service, Creative Commons

Our trade policy recently has been a case of the right diagnosis and the wrong prescription. There’s bipartisan agreement on the structural problems: China’s subsidies, favoritism toward SOEs, and forced technology transfer. But the tariffs prescription has produced enormous collateral damage in the United States, beginning with farmers, who lost a lot of market share, and also manufacturers, some of whom have taken on a double hit because the parts they were importing from China have become more expensive and the products that they’re exporting have become more expensive because of Chinese retaliation.

Instead of going it alone and unilaterally trying to trip China, the next president really needs to focus on the running faster part. How do we get America’s innovation strategies functioning better? How can we put more money into R&D and more investment into developing new cutting edge technologies? Our ability to get them to change their behavior is limited. But we can control our economy.”

The Path Ahead

It won’t be easy for the next U.S. president to successfully implement all of these recommendations. But the stakes couldn’t be higher, both for the economic success of the next administration and the well-being of the American people. The experts we spoke with didn’t all agree on how the U.S. should resolve issues of trade, technology, and investment with China, but there was widespread consensus on a few issues.

First, the U.S. should engage with allies in order to counterbalance China, instead of attempting to unilaterally effect change. Second, the U.S. should aggressively and strategically invest in the domestic economy, particularly in high-tech and cutting-edge fields. And third, the U.S. needs a thoroughly considered, overall strategy to face economic tensions with China, rather than a tit-for-tat approach that breeds escalation.

Though the onus will be on the next administration to lower the temperature in the heated U.S.-China relationship, it always takes two to tango. As Susan Shirk, a research professor at the University of California, San Diego and chair of the 21st Century China Center says, “A lot really depends on Xi Jinping and whether his government can take advantage of the opening that would be created by the next administration to stabilize relations, and whether there will be a willingness to make the necessary compromises on Chinese side.”

Blaming China for our economic woes, rather than crafting nuanced policy to solve those woes, is a tendency on both sides of the American political aisle. Hopefully, regardless of whether Trump or Biden occupies the Oval Office next year, our China policy can start lay the groundwork for a more productive economic relationship.

David Barboza is the co-founder and a staff writer at The Wire. Previously, he was a longtime business reporter and foreign correspondent at The New York Times. @DavidBarboza2

Katrina Northrop is a journalist based in New York. Her work has been published in The New York Times, The Atlantic, The Providence Journal, and SupChina. @NorthropKatrina

Eli Binder is a New York-based staff writer for The Wire. He previously worked at The Wall Street Journal, in Hong Kong and Singapore, as an Overseas Press Club Foundation fellow. @ebinder21