Good evening. This week’s cover story brings you inside one of the most sensational business stories of the year so far — and it has nothing to do with Covid-19. Luckin Coffee’s spectacular collapse has dominated headlines in both the U.S. and China, as allegations of fraud have made $11 billion of wealth vanish since January. The Wire gives you all the juicy details, but we also look at how Luckin’s fall fits in to one of the more troubling aspects of global investing over the past decade.

Want this emailed directly to your inbox? Sign up to receive our free newsletter. Subscribe to The Wire here. For a limited time, we’re offering one free article to users.

The Big China Short

When Luckin Coffee had its Nasdaq IPO, it was touted as China’s home-grown, tech-savvy answer to Starbucks. Its stores were expanding like crazy, it had sophisticated investors like BlackRock and Morgan Stanley cheering it on, and at its height just three months ago, its stock reached $51 a share, resulting in a $12 billion valuation. As The Wire reporter Eli Binder shows, however, there was just one problem: Luckin Coffee wasn’t actually selling much. An anonymous report detailing middling foot traffic in stores and sales receipts was widely shared among short-sellers who finally got the world to wake up and smell the fraud.

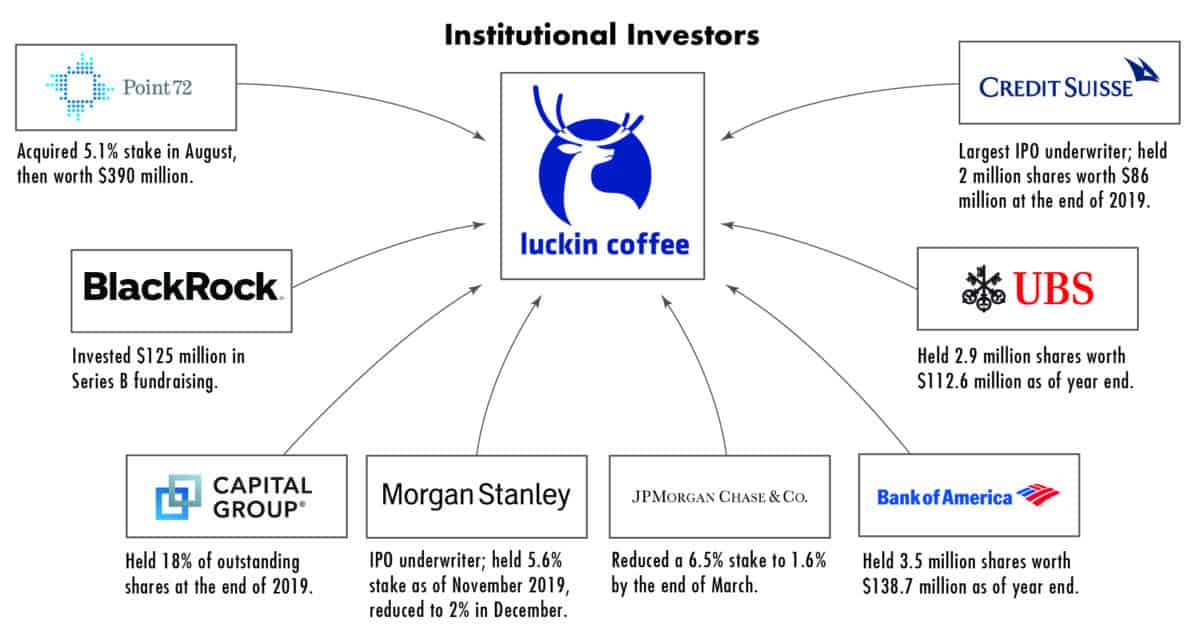

The Big Picture: The Players Behind the Rise and Fall of Luckin

Five people owned more than 80 percent of Luckin Coffee at the time of its IPO. Some of the world’s biggest and most sophisticated asset managers, including BlackRock, Credit Suisse and Morgan Stanley, bought into Luckin’s model. And three prominent short-sellers helped publicize the allegations of fraud that ultimately led to Luckin’s collapse: Carson Block, Anne Stevenson-Yang, and Jim Chanos. The Wire‘s graphics this week introduce the people behind Luckin Coffee, the institutions that fell for its inflated numbers, and the short-sellers who suspected it was all too good to be true.

Credit: U.S. Secret Service

China vs. U.S. Growth Models Shape Covid-19 Responses

The type of public-health measures pursued by the two countries — and their outcomes — have diverged sharply. China’s draconian lockdowns produced a dramatic decline in new cases, whereas America’s delayed and fragmented response allowed infections — and the death toll — to mount. This divergence is often attributed to political differences: Chinese central planning allows for more resolute action. But in their op-ed for The Wire, Andrew Sheng and Xiao Geng argue that this explanation misses the extent to which the U.S. and Chinese growth models have shaped their responses — and the financial and economic effects.

Credit: Aleksandra Sova, Shutterstock

Week in Review: Digging Out of the Economic Hole

Each week, The Wire’s Dave Smith rounds up the most interesting China news and insights you may have missed. This week, he looks at how long the economic recovery will likely be, revealing gaps in China’s unemployment insurance, the country’s launch of a new digital currency, the reason censors suspended a ByteDance app, a meatless gamble by Starbucks, and how China is winning a very important battle for lithium ion batteries — which are crucial for everything from electric cars to cordless drills.

A Q&A With Shan Weijian

Shan Weijian is an economist and investor based in Hong Kong. In this interview with The Wire’s David Barboza, he explains how the current pandemic will actually slow U.S. efforts to decouple the two economies and what it means now that China’s retail market has surpassed that of the U.S. “China is no longer just a factory for the world,” he says. “GM sells more cars in China than in the U.S. Where do you think GM can move to that makes economic sense?”

Shan Weijian

Illustration by Lauren Crow

Subscribe today for unlimited access, starting at only $19 a month.